The Motivation Behind CSR Manager Role in Indonesian Mining Companies

on

Jurnal Ilmiah Akuntansi dan Bisnis

Vol. 17 No. 1, January 2022

The Motivation Behind CSR Manager Role in Indonesian Mining Companies

Rabin Ibnu Zainal1*, Fitriya2, Teguh Iman Santoso3

|

Abstract |

AFFILIATION:

|

1,3 Universitas Sumatera Selatan, Indonesia 2 RMIT University, Vietnam |

The goal of this research is to investigate the underlying motivations for the role of the CSR manager. The study used smart PLS analysis to identify three motivations behind the role of CSR managers in mining |

|

*CORRESPONDENCE: |

companies, namely economic, legal and ethical domains. The study |

|

includes 114 managers or representatives from CSR-implementing mining companies in South Sumatera, Indonesia. The manager of mining | |

|

THIS ARTICLE IS AVAILABLE IN: |

companies in this region is mandated to implement CSR based on the |

|

rules of legislation. The study found that following Indonesian CSR legislation is not a significant motivation for CSR managers. Instead, CSR | |

|

DOI: |

managers' decisions are influenced by economic motivation. |

|

10.24843/JIAB.2022.v17.i01.p08 |

Furthermore, analysis results revealed that CSR managers' motivation |

|

CITATION: |

for economic and legal domains influenced their role in CSR. |

|

Zainal, R. I., Fitriya, Santoso, T. I. (2022) The Motivation Behind CSR Manager Role in Indonesian Mining Companies. Jurnal Ilmiah Akuntansi dan Bisnis, 17(1), 117-127. |

Keywords: CSR, mining companies, motivation, role. Introduction |

|

ARTICLE HISTORY Received: |

Corporate Social Responsibility (CSR) is concerned with businesses' connections with the broader society and encompasses an organization's |

|

11 November 2021 |

monetary, legal, ethical, and philanthropic responsibilities (Afrin, Sehreen, Polas, & Sharin, 2020). Many studies in CSR are interested in |

|

Revised: |

finding empirical evidence about the characteristics of managers and |

|

10 January 2022 |

their role in CSR. There are many reasons for this, including the fact that |

|

Accepted: |

CSR managers are human resource development (HRD) professionals |

|

14 January 2022 |

who connect corporations with society. They must be capable of effectively and efficiently directing their subordinates. There are many factors of motivation that affect how a manager views his role in CSR. In line with this, Jang and Ardichvili (2020) suggest that HRD must have a link with CSR to ensure its sustainability. This is why an investigation into the motives of managers with regards to their role in CSR is crucial for HR practitioners within CSR. CSR can take on a variety of distinct meanings in different nations or industry sectors, depending on the legal, social, and economic environment; as a result, it is difficult to define an organization's "Social Responsibility" (Tukur, Shehu, Mammadi, & Sulaiman, 2019). Managers and directors of a business are obligated to avoid causing harm to stakeholders by making decisions based on values, morals, work ethics, and a variety of other sound business concepts (Apriliani, 2021). In addition, the ability of managers to make decisions is one of the aspects that can affect a company's ability to compete in the marketplace (Kloko & Bayunitri, 2020). In Indonesia, the drivers of CSR |

may be related to the existence of CSR laws requiring companies to practice CSR (Zainal, 2019). Because of this obligation, we might conclude that legal motivation is an important factor in the role of the CSR manager. However, we can not overlook the company's economic importance in CSR, such as obtaining a social license from the community, ensuring operational safety, and improving the company's reputation or image (Cesar, 2020).

On the other hand, the direct and indirect effects of globalization, such as the expansion of CSR waves, the spread of multinational corporations (MNCs) to developing countries, may raise ethical issues for managers involved in CSR implementation (Chambers, Chapple, Moon, & Sullivan, 2003). As a result, the CSR manager's role is challenging, as they must meet the expectations of both their organization and the community. As a result, it is critical to investigate the factors that influence the CSR manager's role. Specifically, CSR is identified by its underlying strategic purposes (e.g. legitimacy, responsibility for social externality, and competitive advantage), its drivers (e.g. market, social regulations, and government regulations) and its domain motives (e.g. economic, legal, and ethical) (Visser, 2008). The third attribute, namely, the manager’s domain motive to CSR responsibilities, is one of the focuses of this study.

This article is based on Schwartz and Carroll (2003) CSR model, which proposed three domains of influence on managers' decisions to implement CSR. These are as follows: (1) economic, (2) legal, and (3) ethical. This theory is relevant to the context of studies that question the motives of CSR managers in the existence of CSR legislation. This model was derived from Carroll's (1991) CSR pyramid; however, Schwarts and Carroll (2003) removed the philanthropic domain from their model because business philanthropic activities such as charitable giving can be motivated by either an ethical or an economic motive. Economic motivation implies that managers use CSR as an economic tool to help businesses achieve their profit goals (Friedman, 2007). Legal motivation in the Indonesian context can be related to companies' obligations to CSR laws, such as Law No. 40/2007 on Limited Liability Companies, which require them to conduct CSR during their operations. While ethical responsibility is associated with company activities and practices that are expected or prohibited by society when conducting business (Gjølberg, 2011). Ethics appears to have the least influence on CSR activities in developing countries (Visser, 2008).

CSR has been a significant focus in Western countries, but unfortunately, CSR in Indonesia is far less studied. According to Kemp (2001) CSR in Indonesia was a reasonably new concept prior to the fall of the "new order regime" in the mid-1990s, during which time a few companies only used it. Local districts have successfully requested more autonomy and authority from the central government after experiencing thirty-two years of being under a highly centralized government regime. This also includes any demand for contributions from the company, which previously went to the federal government in Jakarta under President Suharto. Businesses and firms that are involved in natural resources have had to implement CSR requirements, which was an impetus for the government to mandate CSR legislation. Some of the world's first laws on CSR are No. 25/2007 and the LLC Law No. 40/2007, both of which were passed in 2007 (Zainal, 2020). Following the resignation of President Soeharto in 1999, all of Indonesia's CSR laws were instituted. CSR practices in Indonesia are now mandatory because of these laws.

In the context of mandated CSR laws in Indonesia, the purpose of this study is to determine the motivation that drives managers to take on CSR role. In the context of this mandated CSR, the perspective of CSR managers from mining companies should be investigated. For these reasons, the following research questions are addressed in this article The main research question is “What is the influence of economic, legal and ethical motivation to manager to take a role on CSR in mining companies?”

This study will help advance our understanding of CSR and HRD. It is, first and foremost, designed to supplement the framework developed by Hemmingway and Maclagan (2004) who formulated the notion of "locus of responsibility". CSR is a method that helps to fill the gaps that emerge when a company competes in a competitive environment and places requirements on managers from various stakeholders. The above statement suggests that CSR motives need to be analyzed to comprehend CSR roles. Also, the manager in charge of CSR serves as a human resources manager who is tasked with connecting the corporation to the community. It follows that it is essential to evaluate what his motivations are when it comes to CSR implementation. The data would help establish CSR policies and programs that respect all interests, including the interests of the corporation, the community, and the government. Third, since CSR was created with the purpose of practising socially responsible HRD, managers have a duty to implement and execute every facet of social responsibility activities, including education for businesses on social responsibility and to use HRD strategies to foster socially conscious business practices (Jang & Ardichvili, 2020).

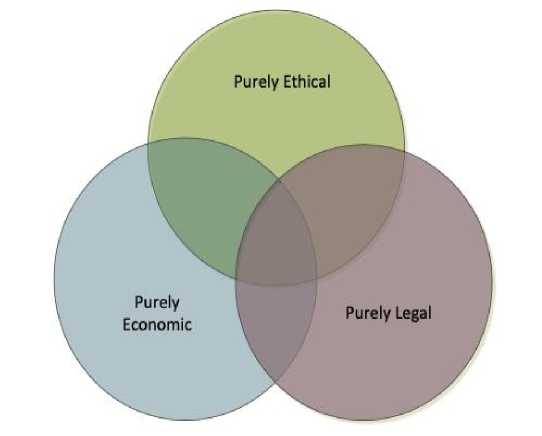

Three CSR domain motives defined as this study attempts to identify the motivations of CSR managers, whether it is based on legal motive as an obligation to implement the legislation, or there are other factors that motivate them. Schwartz and Carroll (2003) model offered three domains on a company manager decision to apply CSR. There are three of them: (1) economic, (2) legal, and (3) ethical (see Figure 1.). Figure 1. demonstrates how the three areas of economic, ethical, and legal duties overlap and interact. However, CSR efforts are rarely motivated purely by one domain.

Figure 1. Three domain motives of CSR

Source : Adopted from Schwartz & Carroll (2003)

The ideal overlap is found in the model's centre, when economic, legal and ethical responsibilities are all met simultaneously. Other pure domains and overlapping domains in the model may reflect real-world business circumstances that must be studied and examined to demonstrate the problems that business decision-makers encounter.

In respect to Figure 1., using these three CSR domain in this research may help to discover the internal motivation of mining company managers to take on CSR roles. This study questioned whether the existence of CSR law became the dominant domain in influencing CSR manager roles in Indonesia. This model provides other motivational domains, such as economics and legal that can also affect CSR manager roles. Study of Ismail, Kassim, Amit, & Rasdi (2014), which takes CSR orientation, consisting of economic, legal, ethical and philanthropic, as a predictor in identifying CSR manager roles in companies in Malaysia mentions that economic responsibility has a higher ranking in the orientation or motivation of CSR managers in Malaysia. Meanwhile, legal responsibility is the lowest orientation or motivation for CSR managers in Malaysia. CSR is concerned with human behaviour, and it is a complex process involving a wide range of organizations with varying business models and stakeholders. As a result, CSR has evolved into a concept encompassing corporate social responsiveness and all social activities in which corporate executives play a significant part.

The economic domain often connects a company's CSR to its performance or profit. This regards CSR solely as a tool for the corporation to achieve its financial goal, which is profit (Berger, Cunningham, & Drumwright, 2007; Dare, 2016). This domain is also known as the narrow CSR perspective, in which businesses will only engage in CSR-related activities if there is a clear link to financial performance, and CSR is a tool to achieve this economic goal (Dare, 2016; Maas & Liket, 2011). This realm of CSR states that CSR initiatives from firms are primarily evaluated in a purely economic manner to pursue a clear link to financial performance. So, hypothesis 1 can be developed from this domain motive.

-

H1: Economic domain motive has a significantly positive influence on CSR manager role in Indonesian mining companies.

The Legal domain discusses why firms want to practice CSR in order to obey or comply with the law. The law is a form of 'codified ethics,' which means that it is a way of fairness developed by legislators after taking into account diverse societal values (Schwartz & Carroll, 2003). Given Indonesia's CSR regulations, it is reasonable to infer that CSR is exclusively motivated by the company's compliance with the legislation (Zainal, 2019). However, whether, if so, and why each firm handles CSR differently when executing the same legislation should be asked. Based on this concept, hypothesis 2 is developed.

-

H2: Legal domain motive has a significantly positive influence on CSR manager role in Indonesian mining companies.

On the other hand, the ethical domain is frequently associated with a broad view of CSR or a normative approach to CSR. In general, the ethical domain refers to firm operations consistent with the community's expectations and other important stakeholders both locally and globally (Karaosmanoglu, Altinigne, & Isiksal, 2016). However, it is seen to be impossible to incorporate all stakeholders' expectations because societal norms vary and rely on context. Hypothesis 3 is built from this perspective.

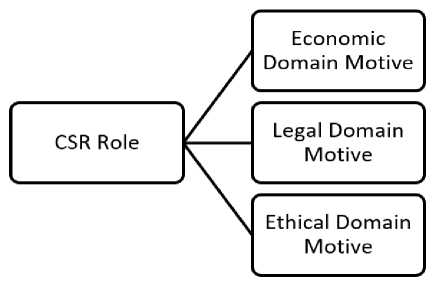

Figure 2. Research Framework

-

H3: Ethical domain motive has a significantly positive influence on CSR manager role in Indonesian mining companies.

-

Figure 2. explains the theoretical framework of this study. Figure explained that the motivation of managers to take CSR roles is influenced by three motivations, namely economic domain motive, legal domain motive and ethical domain motive. This study will look at the domains that are the largest in conjunction with CSR managers in mining companies.

Research Method

Selected CSR managers and representatives from mining companies operating in South Sumatera Province, Indonesia, participated in the study. The number of coal mining companies operating in the area is 114 companies which become the population of this study (Dinas ESDM Provinsi Sumsel, 2020). As a result, it was projected that there were 114 managers or staff related with CSR function in those companies. This is because not all companies have CSR managers and CSR functions are held by other parts such as public relations or operational managers.

In the early stages, we produced a list of the company and the manager's name and the connections received from coworkers who knew the manager's references. Then, all contacts are contacted using Whatsapp and email apps. Hardcopy questionnaires are mailed, and researchers attempt to maintain contact with firm contacts to inquire about questionnaire completion status. Finally, the entire questionnaire can be completed and returned, or it can be taken immediately by the researcher.

The research tool is a questionnaire with four sections covering questions on the economic, ethical, legal, and role in CSR as perceived by CSR managers. Questions about the role of CSR managers were adapted from Ismail, Kassim, Amit and Rasdi (2014) while questions about CSR motivation were adapted from Schwartz and Carroll Model (2003). Each question in the first four sections required a response based on a scale of 1-7, with 1 being "totally untrue" and 7 being "completely truthful." Because it increased the variety of the answers, the 7-point Likert scale was chosen over the 5-point Likert scale (Joshi, Kale, Chandel, & Pal, 2015)The first portion on CSR role has eight tasks designed to measure the manager's role on CSR. "The CSR manager should assume responsibility for developing a formal policy on sustainable actions toward the community," as an example. The second segment, which contains 29 elements, is concerned with CSR

approaches to CSR's economic, legal, and ethical domains. The following are examples of questions from each category: (1) Economic domain: "Each company must retain a strong competitive position”, (2) Legal domain: "It's critical to be a law-abiding business citizen”, (3) Ethical domain: “It is critical to perform in a manner consistent with cultural mores and ethical norms.”

The data collected will be analysed by SEM PLS using smart PLS 3. This analysis will produce an output in the form of a model about the influence of CSR motivation on the CSR role of managers. The analytical steps to be carried out in this study are (Purwanto, Asbari, & Santoso, 2021): (1) Forming the initial model; (2) Check the loading factor of each indicator used in the initial model; (3) Perform iteration steps that aim to abort indicators that are under the rule of thumb; (4) Checking the validity and reliability of the model formed as a result of the iteration process; (5) See the significance of the model that has been made by bootstrapping; (6) The final model of the influence of CSR motivation on the CSR role of managers.

Result and Discussion

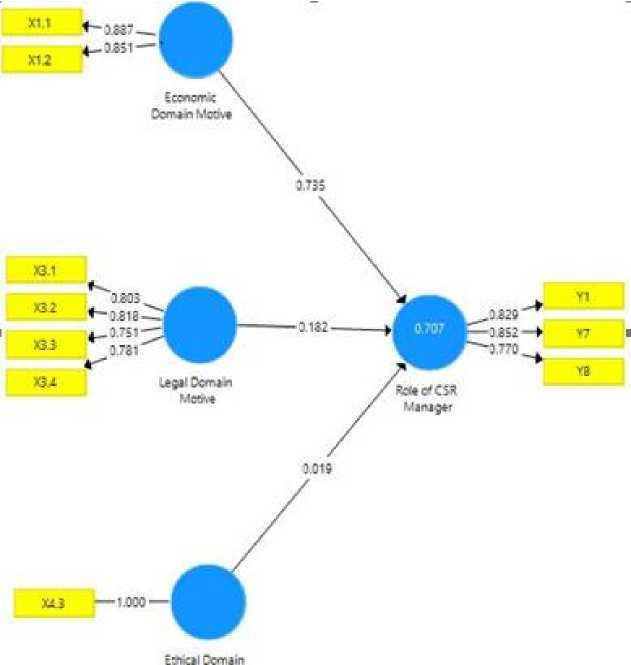

The initial model that is constructed in this study has three independent variables of CSR motive domains: economic, legal, and ethical. The economic domain motive has seven indicators, the legal domain motive has seven indicators, and the ethical domain motive has seven indicators. While the variable dependent is the role of CSR manager, it consists of 8 indicators.

Figure 3. Final Iteration

Source : Analysis from Smart PLS 3, 2021.

Table 1. Reliability and Validity

|

Reliability and Validity | ||||

|

Cronbach’s Alpha |

Rho_A |

Composite Reliability |

Avaregae Varian | |

|

Economic Domain |

0.678 |

0.686 |

0.861 |

0.756 |

|

Motive | ||||

|

Legal Domain Motive |

0.800 |

0.808 |

0.868 |

0.622 |

|

Role of CSR Manager |

0.751 |

0.756 |

0.858 |

0.669 |

Source : Analysis from Smart PLS 3, 2021.

According to the process of loading factors, only two indicators, X1.1 and X1.2, are eligible rules of thumb in the various economic domain factors comprised of seven indicators. In terms of variable legal domain motive, four indicators qualify for the rule of thumb: X.3.1, X.3.2, X3.3, and X3.4. The other three indicators are being researched.

Based on Figure 3., only one indicator qualifies for a variety of ethical domain motives consisting of seven indicators, namely indicator X4.3. The remainder are ineligible and thus cannot be used. Finally, while the variable role of CSR manager includes eight indicators, only three of them are qualified, namely Y1, Y2, and Y8.

After eliminating the indicators that do not qualify, Figure 3. is produced. It can be seen; of the three independent variables used in this study, only two variables qualified the adequacy of indicators to be analyzed in the study, namely variable economic domain motive and legal domain motive. While the ethical domain motive can not be used because there are not enough indicator adequacy requirements, which only leaves 1 reflective indicator. For dependent variables, the role of CSR manager can still be used because it has qualified the adequacy of indicators with three reflective indicators.

-

Figure 3. is the final model resulting from the iteration process. From the image

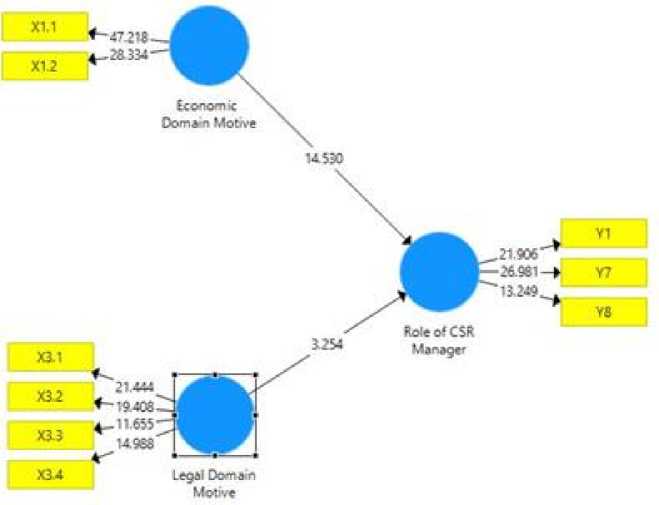

Figure 4. Bootstrapping Picture

Source : Analysis from Smart PLS 3, 2021.

Table 2. Bootstrapping

|

Original Sample |

Sample Mean |

Standard Deviation |

T Statistics |

P Values | |

|

Motive ÷ Role of |

0.736 |

0.738 |

0.051 |

14.530 |

0.000 |

|

CSR Manager Legal Domain Motive ÷ Role of |

0.182 |

0.183 |

0.056 |

3.254 |

0.001 |

CSR Manager

Source: Analysis from Smart PLS 3, 2021

above can be seen only two variables that affect the role of CSR managers, namely, economic domain motive and legal domain motive. From smart PLS, regression models can be generated from the influence of CSR motives on CSR role managers, as follows: Y = a + 0,736 X1 + 0,182 X2 + Ɛ.........................................................................................(1)

Y : Role of CSR Manager

X1 : Economic domain motive

X2 : Legal Domain Motive.

Validity and Reliability: Table 1. shows the construct reliability and validity of the model that has been produced. Validity is seen from the Average Variance Extractive value, which shows the results for all variables in the model above 0.5 which means all variations in the model are valid.

Reliability is seen from three values: Cronbach's Alpha, Rho A, and Composite Reliability. For various economic domain motives obtained two values from cronbach's Alpha and Rho A are below 0.7 which means invalid. However, for composite reliability values are above 0.7 which means valid. We concluded that variable economic domain motive is valid.

Likewise, for variable legal domain motive and role of CSR manager, all assessments of both Cronbach's Alpha, Rho A, and Composite Reliability show reliable values above 0.7. These two variables; legal domain motive and role of CSR manager, are considered reliable.

From Table 2. it can be seen that the three hypotheses proposed are; H1 economic domain motive has a positive and significant effect on the role of CSR manager; H2 legal domain motive has a positive and significant effect on the role of CSR

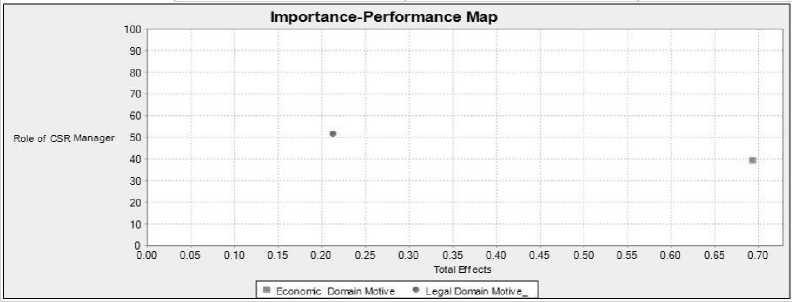

Figure 5. IPMA Graphic

Source : Analysis from Smart PLS 3, 2021.

Table 3. IPMA test

Path Coefficient

Economic Domain Legal Domain Role of CSR

Manager

Motive

Legal Domain 0.182

Motive

Source : Analysis from Smart PLS 3, 2021.

manager. As for H3, the ethical domain motive has a positive and significant effect on the role of CSR manager eliminated or not accepted.

Table 2. shows the significance between the path of economic domain motive to the role of CSR manager t-statistics worth 14.530, which means greater than the t-table of 1.96. As for the variety of legal domain, motive has a t-statistic value of 3.254, which is also greater than the t-table of 1.96.

Table 3. shows which is more important than the two dependent variables; economic domain motive and legal domain motive. From the path coefficient analysis, obtained variable economic domain motive is statistically more important than the legal domain motive in driving the role of CSR manager. This means that the motivation of managers in taking on the role of CSR manager is more due to economic motives, such as profit, not because of the mandate of the Law. Figure 5. shows that managers in this study are more likely to have economic domain motive in their role of CSR manager which is worth 0.736, while the legal domain motive is only worth 0.182 less than the economic domain motive.

Conclusion

The study has found important findings for understanding managers' behavior, especially what motivates them to take on CSR roles within companies. This is coupled with the Indonesian context, which has CSR Law that mandates CSR to be carried out by companies, including mining companies. From the findings and discussions in the previous section, it can be concluded that only two factors motivate managers, namely economic domain motive and legal domain motive. While variable ethical domain motive is not significant in the results of this study. This means economic motive factors, which direct managers to implement CSR with the aim of profit motive more dominantly influencing managers in CSR roles. Meanwhile, the legal motive factor based on managers' compliance to implement CSR law, although significantly influential, has an important performance.

These results indicate that policies carried out by the government to require companies to implement CSR cannot be separated from the economic motives of the business to benefit. This means that even though the CSR Law is aimed at improving the welfare of the community, but in practice it cannot be separated from the motives of economic profits of the company, such as building an image, ensuring the company's operations and even getting a social license from the community.

References

Afrin, S., Sehreen, F., Polas, M. R. H., & Sharin, R. (2020). Corporate Social Responsibility (CSR) practices of financial institution in Bangladesh: the case of United Commercial Bank. Journal of Sustainable Tourism and Entrepreneurship, 2(2), 69– 82.

Apriliani, N. A. (2021). Implementation of Good Corporate Governance (GCG) At the Ministry of Environment and Forestry. Studi Ilmu Manajemen Dan Organisasi, 2(1), 47–60.

Berger, I. E., Cunningham, P. H., & Drumwright, M. E. (2007). Mainstreaming corporate social responsibility: Developing markets for virtue. California Management Review, 49(4), 132–157.

Carroll, A. B. (1991). The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Business Horizons, 34(4), 39–48.

Cesar, S. (2020). Corporate social responsibility fit helps to earn the social license to operate in the mining industry. Resources Policy, 101814.

Chambers, E., Chapple, W., Moon, J., & Sullivan, M. (2003). CSR in Asia: A seven country study of CSR website reporting.

Dare, J. (2016). Will the truth set us free? An exploration of CSR motive and commitment. Business and Society Review, 121(1), 85–122.

Dinas ESDM Provinsi Sumsel. (2020). Daftar IUP Provinsi Sumatera Selatan (List of IUP in South Sumatera).

Friedman, M. (2007). The social responsibility of business is to increase its profits. In Corporate ethics and corporate governance (pp. 173–178). Springer.

Gjølberg, M. (2011). Explaining regulatory preferences: CSR, soft law, or hard law? Insights from a survey of Nordic pioneers in CSR. Business and Politics, 13(2), 1–31.

Hemingway, C. A., & Maclagan, P. W. (2004). Managers’ personal values as drivers of corporate social responsibility. Journal of Business Ethics, 50(1), 33–44.

Ismail, M., Kassim, M. I., Amit, M. R. M., & Rasdi, R. M. (2014). Orientation, attitude, and competency as predictors of manager’s role of CSR-implementing companies in Malaysia. European Journal of Training and Development.

Jang, S., & Ardichvili, A. (2020). Examining the link between corporate social responsibility and human resources: Implications for HRD research and practice. Human Resource Development Review, 19(2), 183–211.

Joshi, A., Kale, S., Chandel, S., & Pal, D. K. (2015). Likert scale: Explored and explained. British Journal of Applied Science & Technology, 7(4), 396.

Karaosmanoglu, E., Altinigne, N., & Isiksal, D. G. (2016). CSR motivation and customer extra-role behavior: Moderation of ethical corporate identity. Journal of Business Research, 69(10), 4161–4167.

Kemp, M. (2001). Corporate social responsibility in Indonesia: quixotic dream or confident expectation?

Kloko, D. M. E., & Bayunitri, B. I. (2020). Comparison analysis of financial performance telecommunication service which has and has not applied PSAK 73. International Journal of Financial, Accounting, and Management, 2(2), 145–157.

Maas, K., & Liket, K. (2011). Talk the walk: Measuring the impact of strategic philanthropy. Journal of Business Ethics, 100(3), 445–464.

Purwanto, A., Asbari, M., & Santoso, T. I. (2021). Analisis Data Penelitian Marketing: Perbandingan Hasil antara Amos, SmartPLS, WarpPLS, dan SPSS Untuk Jumlah

Sampel Besar. Journal of Industrial Engineering & Management Research, 2(4), 216–227.

Schwartz, M. S., & Carroll, A. B. (2003). Corporate social responsibility: A three-domain approach. Business Ethics Quarterly, 13(4), 503–530.

Tukur, S., Shehu, J., Mammadi, A., & Sulaiman, U. A. (2019). An assessment of corporate social responsibility of property developers in Bauchi Metropolis, Nigeria.

International Journal of Financial, Accounting, and Management, 1(2), 119–129.

Visser, W. (2008). Corporate social responsibility in developing countries. In The Oxford handbook of corporate social responsibility.

Zainal, R. I. (2019). Analysis of CSR Legislation in Indonesia: Mandate to Business. Business and Economic Research, 9(3), 165–181.

Zainal, R. I. (2020). Stakeholders Perception on Mandated CSR Laws in Indonesia. In 3rd Global Conference On Business, Management, and Entrepreneurship (GCBME 2018), Atlantis Press (pp. 210–216).

Jurnal Ilmiah Akuntansi dan Bisnis, 2022 | 127

Discussion and feedback