Theory of Planned Behavior on The Implementation of Environmental Management Accounting

on

Jurnal Ilmiah Akuntansi dan Bisnis

Vol. 18 No. 1, January 2023

AFFILIATION:

1,2,3,4,5Faculty of Economics and Business, Udayana University, Indonesia

*CORRESPONDENCE:

THIS ARTICLE IS AVAILABLE IN:

DOI:

10.24843/JIAB.2023.v18.i01.p08

CITATION:

Kedisan, A. A. V., Ratnadi, N. M. D., Putri, I G. A. M. A. D., Mimba, N. P. R. H. & Sisdyani, E. A. (2023).

Theory of Planned Behavior on The Implementation of Environmental Management Accounting. Jurnal Ilmiah Akuntansi and Bisnis, 18(1), 115-133.

ARTICLE HISTORY Received:

27 December 2022

Revised:

13 January 2023

Accepted:

21 January 2023

Theory of Planned Behavior on The Implementation of Environmental Management Accounting

Anak Agung Vidyaswari Kedisan1*, Ni Made Dwi Ratnadi2, I Gusti Ayu Made Asri Dwija Putri3, Ni Putu Sri Harta Mimba4, Eka Ardhani Sisdyani5

Abstract

G20 2022 put some emphasis on recent environmental issues; one of them is that water pollution that may cause by not only the large company but also micro, small and medium enterprise (MSME) waste, especially textiles, the most found in Denpasar City. This study examines the influence of attitude toward behaviour (ATT), subjective norm (SN) and perceived behavioural control (PBC) on the intention and then the implementation of environmental management accounting (EMA) using legitimacy theory and theory of planned behaviour (TPB). The results showed that ATT and PBC positively influenced the intention to EMA, while SN did not. PBC influence the implementation of EMA positively, while the intention did not. This research enriches legitimacy theory and TPB by revealing the two theories not being able to fully predict the implementation of EMA due to the geographical area, lack of political interest and government regulations that still need improvement.

Keywords: attitude toward behaviour, subjective norm, perceived behavioural control, environmental management accounting

Introduction

Environmental management accounting (EMA) is one way to implement green accounting. Environmental management accounting was introduced in Indonesia for the first time by disseminating the international standard ISO 14001 in 1995. Then it was formally developed through the participation of international institutions in the Southeast Asian region since 2003 (Cahyandito, 2006). The implementation of environmental management accounting is crucial for business actors to carry out. Environmental Management Accounting has helped many business managers allocate environmental costs efficiently and effectively, so the company will get the maximum profit and society's trust by doing environmental maintenance and corporate social responsibility. Implementing environmental management success incorporates hidden environmental costs (Ramli et al., 2019). Given the continuous decline in environmental quality, environmental issues have become a priority for the government. The reality on the ground shows that small enterprises

still cause much environmental pollution. A lot of Environmental pollution has occurred in the province of Bali in recent years, mainly caused by micro, small and medium enterprises (MSMEs). For example, in November 2019, there was pollution at Tukad Badung around Jalan Imam Bonjol, Denpasar. This pollution is known to have originated from a screen printing business operating on Jalan Pulau Misol, Denpasar (Sayoga, 2019). The latest environmental pollution case in April 2022 was river pollution in Mahendradatta road and Gunung Gede road, West Denpasar, by Sablon SMEs operating in Denpasar City (Ginta, 2022). In this case, it was found that the source of pollution came from screen printing waste. Meanwhile, the Head of the Civil Service Police Unit (Kasat Pol PP) for Denpasar City, A.A. Ngurah Bawa Nendra, said that this case originated from the findings of residents who saw the river flow in the area of Jalan Mahendradata and Jalan Gunung Gede, Denpasar, Bali, turning red when Thursday (7/4/2022). Based on the community reports, the Environment and Sanitation Service monitors and takes action on screen printing entrepreneurs who dump waste into rivers (Suparta, 2022).

Based on Indonesian Government Regulation number 18/1999, the waste generated by the textile business is classified as hazardous and toxic waste (B3). In addition, the results of waste monitoring carried out by the Ecological Observation and Wetlands Conservation (Ecoton) forum in Denpasar found that waste from the textile industry had polluted the Jinah River with pollution levels reaching 11 per cent and Mertasari Beach with pollution levels reaching 30 per cent (Ranggawari et al., 2021). BPS data for the Province of Bali stated that of the 4.28 per cent total IBS growth, the textile industry grew 21.91 per cent, followed by other processing industries, which grew 17.59 per cent. Suryawan et al. (2021) stated that the growth of the textile industry can be followed by pollution level increases either directly or indirectly.

This is both good news and a challenge for the government because as textile production increases, more and more waste will be produced. If waste is not treated correctly, it will cause a decrease in environmental quality. Therefore, EMA is implemented, especially in the context of waste treatment. The role of the Denpasar city government is vital in creating an order for textile SMEs in Denpasar City regarding waste disposal. Article 38, paragraph 1 of Denpasar City Regional Regulation No. 11 of 2015 states that every person and/or business entity that pollutes and/or destroys the environment must restore environmental functions (Pemerintah Kota, 2015). This means

Table 1. the Number of Textile Business in Bali Province

|

Regency/City |

Number of Business |

|

Jembrana |

176 |

|

Tabanan |

51 |

|

Badung |

199 |

|

Gianyar |

64 |

|

Klungkung |

147 |

|

Bangli |

91 |

|

Karangasem |

79 |

|

Buleleng |

51 |

|

Denpasar |

1.103 |

|

Total |

1.961 |

Source: Bali Satu Data, 2019

that clear government regulations are important in tackling environmental pollution due to textile waste.

Table 1 shows that Denpasar City has the largest number of textile businesses and the area with the highest average population density in Bali, which is above 5,000 people/km2; this figure explains population density of Denpasar city is much higher than other districts. In addition, there were several cases of pollution due to textile waste which made improving the quality of the environment in the city of Denpasar, a priority for the provincial government. The following presents data related to population density in the last five years in Table 1.

Legitimacy theory explains that a company or organization can only survive for the long term if society feels that the organization has carried out its operations following a value system that is commensurate with society’s value system (Ikbal 2012:28). This means that companies operating in an area must act not contrary to the expectations of the local community. The company operates or takes resources from an area; thus the company must maintain their image in public. One of them is being responsible for maintaining the environment. In order to create a sustainable environment and businesses that are accepted in society, business actors need to implement environmental management accounting.

According to the Theory of Planned Behavior, three key factors—attitude toward behaviour, subjective norm, and perceived behavioural control—significantly impact intention before an actual behaviour. It describes the relationship between these three key factors and intention and the intention-behaviour connections.

Attitude toward a behaviour is an individual ability to consider an action based on the level of advantages of the same action in the past. Attitude toward a behaviour is considered the first variable influencing the intention to behave (Seni & Ratnadi, 2017). Attitudes have been shown to influence intentions significantly. This means that if attitudes can be changed, then intentions may be influenced and may further influence behaviour (Al-Rafee & Cronan, 2006). For example, previous research conducted in Australia shows that attitude toward behaviour has positive and significant influences on cotton farmers' intention to adopt EMA (Tashakor et al., 2019) and environmentally friendly business intention (Adibatunabillah et al., 2022). Previous studies found that different countries, cultures, disciplines, management and age groups may change the influence of attitude on behaviour intention (Botetzagias et al., 2015; Dallas et al., 2014; Kuasirikun, 2005). The study noted that having a positive attitude toward a certain behaviour leads individuals to perform that behaviour (Povey et al., 2000; Rosenwald et al., 2002; Zemore & Ajzen, 2014). Based on this explanation, the first hypothesis can be formulated as follows:

Figure 1. Conceptual Framework

Source: Processed Data, 2022

H1: Attitude toward behaviour positively affects the intention to implement environmental management accounting (EMA).

The second factor that influences intention is the subjective norm. Subjective norm is pressure from outside that can encourage someone to take action or not. Subjective norms for MSME actors usually come from surrounding stakeholders, including government regulations, customers, suppliers and environmental monitoring agencies. In this case, stakeholder pressure is a proxy for the subjective norm. This is why the existence of a business is greatly influenced by the support of the stakeholders of the business (Ratnadi, 2014). Previous research conducted by get the result that subjective norms significant positive influence the intention of Australian cotton farmers to adopt environmental management accounting (EMA) (Tashakor et al., 2019) and environmentally friendly business intention (Adibatunabillah et al., 2022). Businesses that neglect their responsibility in protecting the environment will result in severe sanctions from the local government and loss of stakeholder confidence (Paschoalotto, 2021). Subjective norms are the strongest predictor of the intention to implement management accounting compared with performance and effort expectancy (Nguyen & Le, 2020).

H2: Subjective norms positively affect the intention to implement environmental management accounting (EMA).

The third factor that influences behavioural intention is perceived behavioural control. Perceived behavioural control is an opportunity available to individuals to measure the possible limits of achieving a particular behaviour (Ajzen, 1991). It is the individual's perceived ability to apply a particular behaviour (Botezagias et al., 2015). Another definition of perceived behavioural control is a response that comes from a certain individual (Povey et al., 2000; Rosenwald et al., 2002; Zemore & Ajzen, 2014)l to the level of difficulty of specific behaviour based on previous experience which influences intention (Fitriani et al., 2021). In general, an individual can measure whether or not the individual is capable of doing something. For example, previous research gets the result shows that perceived behavioural control has a significant positive influence on the intention of cotton farmers to adopt environmental management accounting (EMA) in Australia (Tashakor et al., 2019) and environmentally friendly business intention (Adibatunabillah et al., 2022). Based on this explanation, the third hypothesis can be formulated as follows:

H3: Perceived Behavioral Control positively affects the intention to implement environmental management accounting (EMA).

Perceived behavioural control is another factor that influences behaviour based on the theory. Aska (2017) shows that green behaviour is positively influenced by perceived behavioural control. Wang et al., (2019) found that self-efficacy as a proxy of perceived behavioural control also positively affected eco-behaviour. De Leeuw et al., (2015) also found that perceived behavioural control best predicts eco-friendly behaviour. Based on this explanation, the fourth hypothesis can be formulated as follows:

H4: Perceived Behavioral Control positively affects the implementation of environmental management accounting (EMA).

The relationship between intention and behaviour. Sisdyani et al., 2020 found that intention and behaviour are in one relationship. In line with Morren & Grinstein (2016), the individual or population tend to have intentions and turn their behaviour into real. Yadav & Pathak (2017) found that consumer intention positively affects purchasing behaviour of environmentally friendly products in developing countries. Another research by (Shirokova et al., 2016) found that student intention of entrepreneurship strongly affects their behaviour toward starting a real business. Based on this explanation, the fifth hypothesis can be formulated as follows:

H5: The intention to implement Environmental Management Accounting has a positive effect on implementing environmental management accounting (EMA).

Research Method

This study chose the location of micro, small and medium textile enterprises in Denpasar City. This research was conducted on textile production SMEs because the output of hazardous waste still occurs in the city of Denpasar. MSMEs as the research location

Figure 2. Research Design

Source: Processed Data, 2022

because most of the previous studies had examined large-scale businesses, and there was still very little research related to eco-accounting and its implementation in MSMEs. This study was designed to explain the influence of attitude, subjective norms and perceived behavioural control on implementing environmental management accounting in textile SMEs in Denpasar. This study analyzes the related framework Theory of Planned Behavior in the implementation of EMA based on the basis of legitimacy theory. The research examines the influence of Attitude toward Behavior, Subjective Norm and Perceived Behavioral Control on intention and then on the implementation of EMA, which is proxied through business managers' perceptions.

This study used a quantitative research design using a Likert scale from 1 (strongly disagree) to 7 (strongly agree). The questionnaire instrument used has been past the validity and reliability test using the Smart PLS software. Data was collected by convenience sampling method, used in situations with large populations. Convenience sampling is a sampling technique based on the convenience of the researcher, namely those that the researcher meets by chance, is deemed suitable, and is willing to be a source of data in accordance with the researcher's criteria.

This study collects perceptions from the MSMEs business managers, including the owner, founder, co-founder, manager, financial manager and accounting department. Assuming that each business has three management staff, the total sample is 309 questionnaires that have been tested for validity and reliability and will be distributed to owners and managers of textile SMEs in Denpasar City. Data collection was carried out for 40 days. Questionnaires were first distributed online by contacting the business through WhatsApp, Instagram direct messages and business email, but only a few responded. Most prospective respondents only read the messages without giving a response. Therefore, we moved on to collecting data offline by visiting prospective respondents at their place of business, and the response was much more efficient than online.

The analysis method used Structural Equation Modeling-Partial Least Square (SEM-PLS), a causal modelling strategy that tries to maximize the variance of conceptually specified latent variables. The outer model, inner model, and hypothesis testing are all included in the PLS analysis. An outer model analysis was performed to ensure the measurement was valid and reliable. The analysis considers several factors, including Cronbach's alpha, composite reliability, average variance extracted, and convergent and discriminant validity. This model analysis aims to examine the relationships between the latent constructs. The subsequent study includes various calculations, including R, F, and Q squares. The t-statistic and probability values show the results of hypothesis testing. As a result, when the t-statistic (error 5%) is greater than 1.96, the hypothesis is accepted, and the alternative hypothesis, H0 is rejected. If the p-value is less than 0.05, the hypothesis is accepted when using probability to reject or accept it. The following equation was used to analyze the collected data.

Y= α + β1X1 + β2X2 + β3X3 + β4X4 +e......................................................................................(1)

Y = Implementation of Environmental Management Accounting

α = Constant

β = regression coefficient

Xi = attitude toward behaviour

X2 = Subjective norm

X3 = Perceived behavioural control

X4 = Intention to Implement Environmental Management Accounting

e = errors

Results and Discussion

After observing the situation in the field, it was found that many textile businesses refused to accept the questionnaires, and some businesses were no longer operating. This causes these businesses to be removed from the sample list.

The questionnaires used in the study were 115 questionnaires which were 176 questionnaires distributed, and 61 questionnaires were not returned. Of the 115 questionnaires, only 99 returned that could be analyzed, while 16 were dropped because part of the questionnaire was returned incomplete. Based on Table 2, the response rate obtained is 65 per cent and the usable response rate obtained is 57 per cent. We classified the respondents' characteristics based on position level, age, gender, length of service as the official concerned, level of education, and belief can be seen in Table 3. Descriptive statistics show the characteristics of the research variables, which consist of values of minimum, maximum, mean and standard deviations.

Table 4 shows a mean score of Implementation of EMA (Y), which is 131 shows that the respondent had implemented environmental management accounting (EMA); it can be seen from the average closer to the maximum value, which is 154. The mean of Attitude toward Behavior (X1), which is 66, shows the role of attitude toward behaviour in implementing EMA because the average is closer to the maximum score, which is 77. The mean of the subjective norm (X2), which is 72, shows how subjective norms play a part in implementing EMA because the average is closer to the maximum score, 84. The mean of perceived behavioural control (X3), which is 66, shows the role of PBC in implementing EMA in textiles because the average is closer to the maximum score, which is 77. Lastly, the mean of intention to implement EMA (X4), which is 84, shows the role of intention in implementing EMA because the average is closer to the maximum score, which is 98.

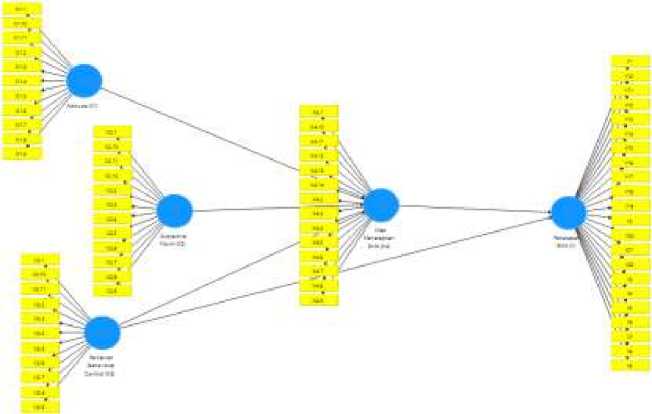

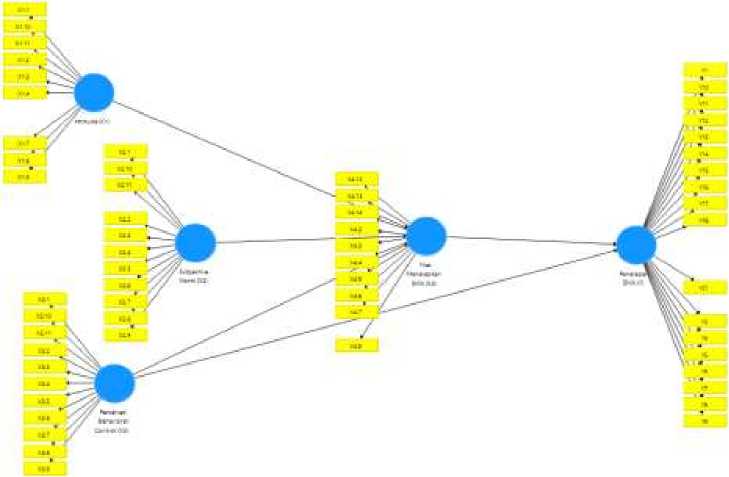

An outer model analysis is the first step of the whole data analysis. We took this test twice because in the outer loading section, we found some indicator that was invalid at the first test, and then the second test was run to ensure all the indicators remaining are still valid to measure certain variables. Figure 3 is a measurement model tested for the first test, which still contained invalid indicators (convergent validity score less than 0,7); those invalid indicators got eliminated, and we continued by running the second algorithm test. On the second algorithm test, we found that all the indicators were already

Table 2. Questionnaire Delivery and Return Details

|

Information |

Amount |

|

Questionnaire distributed |

176 |

|

Unreturned questionnaires |

(61) |

|

Returned questionnaire |

115 |

|

Incomplete questionnaire |

(16) |

|

Questionnaire analyzed |

99 |

|

Rate of Return (response rate) |

65% |

|

The rate of return used (useable response rate) |

57% |

Source: Processed Data, 2022

Table 3. Characteristics of Respondents

|

Amount Percentage | |

|

Owner Co-Founder Manager Accounting Other Total |

45 45% 18 19% 10 10% 18 18% 8 8% 99 100% |

|

Age: |

Amount Percentage |

|

<21 21-30 31-40 41-50 Total |

8 8% 52 53% 34 34% 5 5% 99 100% |

|

Gender: |

Amount Percentage |

|

Man Woman Total |

63 64% 36 36% 99 100% |

|

Length of Service: |

Amount Percentage |

|

1-5 Years 6-10 Years >10 Years Total |

57 58% 29 29% 13 13% 99 100% |

|

Level of education: |

Amount Percentage |

|

Senior High School Diploma Bachelor Master Total |

20 20% 18 18% 53 54% 8 8% 99 100% |

Source: Processed Data, 2022

valid (convergent validity score at least 0,7). Figure 4 is the measurement model from the second/final test, which is the indicator that left is only the valid one.

The correlation between the indicator score and the variable score reveals convergence validity. Each indicator must have a score of at least 0,70 to be valid. At the

Table 4. Description of Variable

|

Standard Mean Median Min Max Deviation | |

|

Implementation of EMA (Y) Attitude toward Behavior (X1) Subjective Norm (X2) Perceived Behavioral Control (X3) Intention to Implement EMA (X4) |

131,273 133 70 154 18,422 66,424 68 37 77 9.107 71,909 72 48 84 8,743 65,485 66 33 77 9,842 84,121 86 52 98 10,599 |

Source: Processed Data, 2022

Source: Processed Data, 2022

first PLS Algorithm test, it was found that some indicators had a value below 0.70, which is invalid. Furthermore, the invalid indicators were removed from the research model, so only valid ones remained. After removing invalid indicators, we run the second convergent validity test to ensure that the remaining indicators score at least 0.7 so those indicators are able to measure certain variables. The result of the beginning and the final outer loading of indicators is in Table 5.

The Fornell-Larcker Criterion score of each indicator variable must be greater than

Figure 4. Final Measurement Model

Table 5 Results of Convergence Validity Analysis

|

Indicato r |

Outer Loading |

Variable |

Indicato r |

Outer Loading | |||

|

Beginning |

Final |

Beginning |

Final | ||||

|

X1.1 |

0.886 |

0.903 |

X2.1 |

0.850 |

0.856 | ||

|

X1.2 |

0.824 |

0.832 |

X2.2 |

0.782 |

0.801 | ||

|

X1.3 |

0.848 |

0.868 |

X2.3 |

0.727 |

0.725 | ||

|

X1.4 |

0.865 |

0.868 |

X2.4 |

0.724 |

0.715 | ||

|

Attitude |

X1.5 |

0.283 |

- |

X2.5 |

0.813 |

0.815 | |

|

Toward |

X1.6 |

0.596 |

- |

Subjective |

X2.6 |

0.715 |

0.716 |

|

Behavio |

X1.7 |

0.884 |

0.891 |

Norm(X2) |

X2.7 |

0.715 |

0.709 |

|

r (X1) |

X1.8 |

0.914 |

0.937 |

X2.8 |

0.783 |

0.783 | |

|

X1.9 |

0.901 |

0.901 |

X2.9 |

0.825 |

0.831 | ||

|

X1.10 |

0.762 |

0.739 |

X2.10 |

0.713 |

0.705 | ||

|

X1.11 |

0.883 |

0.876 |

X2.11 |

0.720 |

0.702 | ||

|

X2 .12 |

0.447 |

- | |||||

|

X3.1 |

0.860 |

0.860 |

X4.1 |

0.512 |

- | ||

|

X3.2 |

0.857 |

0.856 |

X4.2 |

0.854 |

0.857 | ||

|

X3.3 |

0.909 |

0.908 |

X4.3 |

0.855 |

0.839 | ||

|

X3.4 |

0.779 |

0.778 |

X4.4 |

0.928 |

0.923 | ||

|

Perceive |

X3.5 |

0.883 |

0.884 |

X4.5 |

0.760 |

0.773 | |

|

d |

X3.6 |

0.848 |

0.848 |

Intention |

X4.6 |

0.858 |

0.892 |

|

Behavio |

X3.7 |

0.834 |

0.835 |

to |

X4.7 |

0.826 |

0.845 |

|

ral |

X3.8 |

0.877 |

0.878 |

Implemen |

X4.8 |

0.621 |

- |

|

Control |

X3.9 |

0.819 |

0.820 |

t EMA (X4) |

X4.9 |

0.719 |

0.705 |

|

(X3) |

X3.10 |

0.760 |

0.759 |

X4.10 |

0.341 |

- | |

|

X3.11 |

0.879 |

0.878 |

X4.11 |

0.655 |

- | ||

|

X4.12 |

0.845 |

0.862 | |||||

|

X4.13 |

0.876 |

0.915 | |||||

|

X4.14 |

0.850 |

0.865 | |||||

|

Yι |

0.816 |

0.819 |

Y12 |

0.919 |

0.929 | ||

|

Y2 |

0.506 |

- |

Y13 |

0.917 |

0.929 | ||

|

Y3 |

0.814 |

0.800 |

Yl4 |

0.907 |

0.919 | ||

|

Implem |

Y4 |

0.859 |

0.871 |

Y15 |

0.914 |

0.918 | |

|

Y5 |

0.861 |

0.855 |

Y16 |

0.812 |

0.822 | ||

|

entation | |||||||

|

of FK∕IΛ |

Y6 |

0.892 |

0.898 |

Y17 |

0.808 |

0.823 | |

|

(Y) |

Y7 |

0.906 |

0.897 |

Y18 |

0.866 |

0.875 | |

|

Y8 |

0.832 |

0.823 |

Y19 |

0.483 |

- | ||

|

Y≡ |

0.896 |

0.888 |

Y20 |

0.642 |

- | ||

|

Y10 |

0.887 |

0.898 |

Y21 |

0.847 |

0.827 | ||

|

Yu |

0.930 |

0.947 |

Y22 |

0.517 |

- | ||

Source: Processed Data, 2022

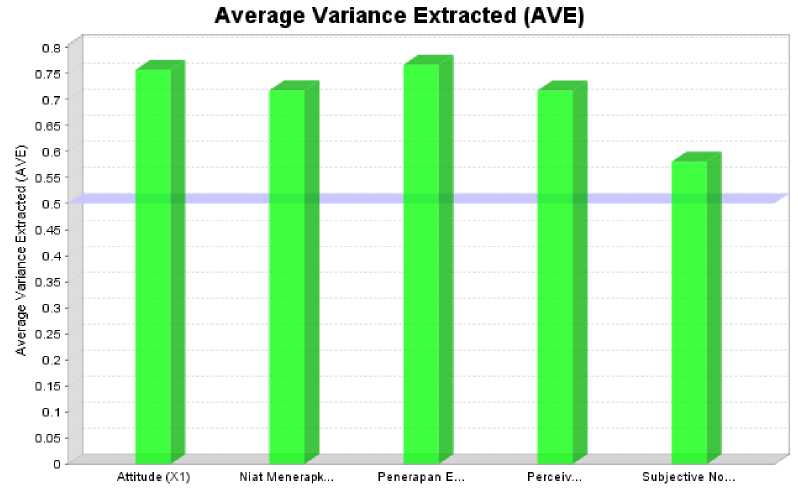

the cross loading and the indicator cross scores between variables must also be worth more than 0.5, which is already passed. The average variance extracted (AVE) value can be used to evaluate discriminant validity. This study's model is strong, as shown in Figure 3 by the model's AVE value, which is higher than 0,50. The outcomes of the discriminant

Table 6. Results of Fornell-larcker Criterion analysis

|

Attitude (X1) |

Subjective Norm(X2) |

Perceived Behavioral Control(X3) |

Intention to Implement EMA (X4) |

Implementation of EMA (Y) | |

|

X1 |

0.870 | ||||

|

X2 |

0.762 | ||||

|

X3 |

0.847 | ||||

|

X4 |

0.847 | ||||

|

Y |

0.876 |

Source: Processed Data, 2022

validity test using the AVE value listed in Figure 5.

The next step is composite reliability, which shows that a measuring instrument can measure the same symptoms with consistent or reliable results. The measuring instrument was reliable if Cronbach's Alpha value was more than 0.7. According to the results, the measuring instrument was determined to be trustworthy because Cronbach's Alpha score was higher than 0.7.

Following the study of the outer model, the inner model is examined, particularly the goodness of fit model test, by examining the R-square value. To determine how much the exogenous variable has an impact on the endogenous variable, the coefficient of determination (R2) is used. For a strong model, the R2 score must be at least 0,75; for a moderate model, it must be at least 0,50; and for a poor model, it must be at least 0,25 (Sarstedt et al., 2017). Figure 4 shows a path diagram representation of the structural model (inner model).

Figure 5. Average Variance Extracted (AVE) Value

|

Table 7. Composite Reliability Value | |||

|

Cronbach's Alpha |

Composite Reliability |

R Square | |

|

Implementation of Environmental Management Accounting (Y) |

0.982 |

0.983 |

0.861 |

|

Attitude toward Behavior (X1) |

0.959 |

0.965 | |

|

Subjective Norm (X2) |

0.929 |

0.938 | |

|

Perceived Behavioral Control (X3) |

0.960 |

0.965 | |

|

Intention to Implement Environmental Management Accounting (X4) |

0.955 |

0.965 |

0.976 |

Source: Processed Data, 2022

The R-square value is used to calculate how much the exogenous variable affects the endogenous variable. For a strong model, the R-Square must have a minimum score of 0,75, a minimum score of 0,50, and a minimum score of 0,25 for a weak model. The R Square value for the desire to apply EMA and EMA Implementation variables is based on the data in Table 8's data. The intention to implement EMA for textile businesses in Denpasar City is mostly predicted by attitude, subjective norm, and perceived behavioural control, with the remaining 2.4 per cent being influenced by a number of other characteristics, according to a strong model with an R Square of 0.976. The intention to apply EMA may predict 86.1 per cent of EMA implementation in textile enterprises in Denpasar City, while the remaining 13,9 per cent is impacted by other factors, according to the R Square associated with the EMA implementation variable, which is 0.861 (strong model).

Hypothesis Testing or Bootstrapping is run at the final stage of data analysis. The bootstrapping procedure produces t-statistical values and p-values, which are then compared with the t-statistics and p-value tables. Research with an error rate of 5 per cent has a t-table requirement of more than 1.96 and a p-value of less than 0.05. If these two conditions are met, the hypothesis is accepted (Ghozali and Latan, 2015). Table 8 shows the results of the analysis of p-value and t-statistics

The p-value on hypothesis 1 (H1) is 0.000, which is lower than 0.05. The t-statistic value of hypothesis 1 (H1) is 5.671. This value is higher than 1.96 while the coefficient value is 0.069, which means hypothesis 1 (H1) is accepted. These results can be interpreted that the attitude toward behaviour has a positive and significant effect on the intention to implement environmental management accounting. Legitimacy theory

Table 8. Hypothesis Test Results

|

Original Sample (O) |

Sample Means (M) |

Standard Deviation (STDEV) |

T Statistics (|O/STDEV|) |

P Values |

Accepted/ rejected | |

|

H1 |

0.391 |

0.391 |

0.069 |

5,671 |

0.000 |

accepted |

|

H2 |

0.042 |

0.044 |

0.027 |

1,543 |

0.124 |

rejected |

|

H3 |

0.573 |

0.571 |

0.077 |

7,429 |

0.000 |

accepted |

|

H4 |

0.775 |

0.800 |

0.154 |

5,021 |

0.000 |

accepted |

|

H5 |

0.155 |

0.128 |

0.166 |

0.935 |

0.350 |

rejected |

Source: Processed Data, 2022

explains that a business will be able to survive in the long term by supporting

Figure 6. Measurement Model Evaluation Results

Source: Processed Data, 2022

environmental preservation. In this case, entrepreneurs and their managers see that implementing EMA is something that can build a good image in society and among stakeholders. The belief that implementing EMA is an activity that has a good impact is a proxy for attitude toward behaviour. The theory of planned behaviour also states that the more a person has the belief that something he is going to do is a good thing, the higher the intention to do that activity.

The p-value hypothesis 2 (H2) is 0.124, which is higher than 0.05. The statistical t value found in hypothesis 2 (H2) is 1.543. This value is lower than 1.96 while the coefficient value is 0.027, which means that hypothesis 2 (H2) is rejected since this value is less than 1.96 and the coefficient value is 0.027. These findings imply that subjective norms do not greatly influence the intention to use environmental management accounting. This means that a company actor's ambition to use environmental management accounting remains unaffected regardless of how much or how little pressure comes from outside sources like the government, family, or other businesspeople.

A number of circumstances may influence the relationship between subjective norms and the intention to adopt EMA. The first possible factor is government regulation. According to coercive institutional theory, an organization or business must comply with the rules that apply in a certain environment to gain legitimacy or public trust. In this study, it was found that the rules and regulations did not work well. Based on field observations, it is known that businesses that have polluted waste do not receive as severe sanctions as stated in Article 58 Paragraph (2) Denpasar City Regional Regulation No. 1 of 2015, which states that the sanction that should be received is a maximum imprisonment of 6 months in prison and a maximum fine. 5 million rupiah (Denpasar City Government, 2015). However, what happened in the field of business only received reprimands and fines without being held accountable for repairing the damage that had been caused. The business is then allowed to continue operations as usual, without strict supervision so it is very vulnerable for a business to repeat the same behaviour. This means that sanctions do not run according to the applicable rules. The results of this study found that government regulations related to environmental pollution still need to be improved. This means that an organization or business will comply with applicable

regulations only if the rules and regulations are properly implemented, and the organization has political interests. The second factor is weak political interests. MSMEs and their stakeholders do not have high political interests. Stakeholders involved in environmental issues with the textile business are family, community, and government, while consumers are not too concerned with the good image of businesses related to the environment. This is what makes the influence of subjective norms insignificant to intention. This is also supported by the acceptance of hypothesis 1, which explains that beliefs influence intentions; people with high beliefs tend not to be easily influenced by outside pressure as long as they stick to their beliefs. The third factor is demography. This research was conducted in Denpasar City, one of the cities in Indonesia, which is a developing country. Similar results support the effect of differences in research locations in research conducted by Dinc & Budic (2016) found that subjective norms did not significantly affect entrepreneurial intentions in Bosnia and Herzegovina, a developing country in Europe. Another factor that may be variable between subjective norms and intentions is the level of compliance. Basically, most people in developing countries tend to be more indifferent to rules than in developed countries. This finding is also in accordance with the institutional theory, which states that organizations in the same sector tend to behave similarly.

Testing the influence of perceived behavioural control on the intention to implement EMA has a 0.000 p-value, which is less than 0.05. The statistical t-value for the correlation between the intention to use EMA and perceived behavioural control is 7.429. The coefficient value is 0.077, and this value exceeds 1.96, indicating that hypothesis 3 (H3) is accepted. According to these findings, the intention to use environmental management accounting is positively and significantly influenced by perceived behavioural control. This result is in line with the legitimacy theory, which holds that a business can maintain itself over the long term by helping to safeguard the environment. In this instance, business owners and managers understand that putting EMA into practice is one technique to ensure business continuity by preserving the calibre of the surrounding resources. EMA implementation confidence serves as a stand-in for perceived behavioural control.

The study's findings are consistent with the idea of planned behaviour, which holds that an individual's desire to engage in a certain activity increases with their level of confidence in their capacities and available resources. The p-value to test the effect of perceived behavioural control on the implementation of EMA is 0.000. This value is lower than 0.05. The statistical t-value found in the relationship between perceived behavioural control and the intention to implement EMA is 5.021. This value is higher than 1.96 while the coefficient value is 0.154, which means that hypothesis 4 (H4) is accepted. These results can be interpreted that perceived behavioural control has a positive and significant effect on implementation. This means that the more a person believes in his own abilities or the resources of the business he owns related to the environment, the higher the implementation of environmental management accounting.

The next hypothesis analyzes the relationship of intention to apply EMA; the p-value is 0.350, which is higher than 0.05 and also has a statistical t-value of 0.935 which is lower than 1,96. Hypothesis 5 (H5) is rejected since this value is less than 1.96 and the coefficient value is 0.166. These findings suggest that the aim has little to no impact on applying environmental management accounting. This research is supported by the institutional theory, which states that organizations that are in the same environment tend to have the same characteristics; in this case, the business of the research

respondents is located in Denpasar City, and it was found that the rules and regulations related to water pollution still need to be improved in their implementation. Sanctions obtained by violators are still not in accordance with applicable regulations. Institutional theory predicts that businesses or organizations of the same type will tend to be more similar because there are coercive, normative and mimetic. Coercive means having to carry out the rules that pass in the business area, normative means that everyone is required to act professionally and mimetic means that an organization acts to imitate other successful organizations. The results of this study enrich institutional theory related to coercive pressure, which results that if sanctions are not applied in accordance with applicable regulations, then organizations or businesses will tend not to be afraid to violate applicable rules even though clear sanctions have been stated in these rules. This means that the intention of a business actor to implement environmental management accounting does not affect the intention of a business actor to implement environmental management accounting. Even if a business actor intends to implement the EMA, it may not necessarily be realized and vice versa. At the organizational level, this phenomenon is very likely to occur. Echegaray & Hansstein (2017) found that most respondents had a positive intention to recycle, but not all of them were realized. This research was conducted on respondents who came from low-income groups with very little chance of turning their intentions into actual behaviour by adopting relatively few adequate recycling practices. When viewed from the characteristics of the respondents, most of the textile businesses are relatively new businesses, so business management still considers income from the business to be prioritized for returns and additional working capital. In addition, the situation of businesses that are just running tends to be unstable so that even though respondents are sure to implement EMA, incidental constraints and lack of internal control can cause the implementation of EMA not to be realized and only stop at the intention. Sisdyani et al. (2020) mention that there are variables that stand between intentions and green behaviour in organizations. The majority of respondents in this study came from businesses under the age of 5 years. The majority of newly established businesses need a better management control system. This finding is in accordance with the institutional theory, which states that organizations in the same sector tend to have similar behaviour. This is also related to unstable business conditions, especially in the financial aspect. Sisdyani et al. (2020) found that the results of testing the direct effect of the implementation of Levers of Eco-Control on green behaviour provide evidence that boundary control has a positive effect on green behaviour; in this case, regulation is needed from both the government and organizations to ensure that intentions are realized into behaviour.

Conclusion

This research found that the TPB and theory of legitimacy cannot be applied in some situations and at the same time, are in line with institutional theory. In this study, TPB cannot fully predict behaviour at the organizational level, namely at the micro, small and medium enterprise levels. Legitimacy theory also cannot fully predict the model due to certain factors. The factors in question are organizational culture, management control, low political interest, geographical location and government regulations that still need to be improved. This study provides an overview regarding the extent to which EMA is implemented in MSMEs and the extent to which government regulations can control the

environmental behaviour of business actors. The results of this study indicate that government regulations still need to be tightened regarding environmental regulations.

Based on the analysis's findings, it can be said that higher attitudes toward behaviour and perceived behavioural control related to the implementation of EMA, higher intentions to do so, and higher levels of perceived behavioural control make it more likely that those intentions will come to pass. High or low subjective norms or external pressure have no bearing on the intentions to implement the EMA, and the intentions have no bearing on the actual implementation of the EMA. The analysis's findings demonstrate that perceptions of behavioural control can be used to predict both intention and EMA implementation and attitudes toward behaviour and perceived behavioural control. It is advised that more studies be done on the mediation effects of financial stability, geographic differences, and governmental regulation in the relationship between subjective norms and the intention to adopt EMA, as well as the mediating effects levers of eco-control. It is suggested that municipal governments tighten environmental and regulatory requirements.

Reference

Adibatunabillah, S. R., Tjahjanto, H. K., Kurnia, M., & Rahayu, P. (2022). Intensi Owner-

Manajer UMKM Kabupaten Sleman Mengembangkan Bisnis Ramah Lingkungan. Jurnal MD. 8(1), 19–49.

Ajzen, I. (1991). The Theory of Planned Behavior. Organizational Behavior and Human

Decision Processes, 50, 179–211.

https://doi.org/10.1080/10410236.2018.1493416

https://idp.springer.com/authorize/casa?redirect_uri=https://link.springer.com/article/

10.1007/s10551-005-1902-

9&casa_token=F3Go73KhMf8AAAAA:swn6JM1glQXfQLtbLHntQV2vdJRO13JUnCI JTRxIPvkx5urdyFwbxhVsj_E-FJ9YC-pzwJU-9Hm8fVKDCKo

Aska, W. L. (2017). Implementasi The Theory Of Planned Behavior Terhadap Perilaku

Pembelian Produk Kosmetik Ramah Lingkungan. S2 thesis, UAJY.

Botetzagias, I., Dima, A. F., & Malesios, C. (2015). Extending the Theory of Planned Behavior in the context of recycling: The role of moral norms and of demographic predictors. Resources, Conservation and Recycling, 95, 58–67. https://doi.org/10.1016/j.resconrec.2014.12.004

Cahyandito, D. rer. nat. M. F. (2006). Environmental Management Accounting (Akuntansi Manajemen Lingkungan). School of Management, Faculty of Economics, University of Padjadjaran, 1(September).

Dallas, B. K., Sprong, M. E., & Upton, T. D. (2014). Toward Inclusive Teaching Strategies.

Journal of Rehabilitation, 80(2), 12–20.

de Leeuw, A., Valois, P., Ajzen, I., & Schmidt, P. (2015). Using the theory of planned behavior to identify key beliefs underlying pro-environmental behavior in highschool students: Implications for educational interventions. Journal of Environmental Psychology, 42, 128–138.

https://doi.org/10.1016/j.jenvp.2015.03.005

Dinc, M. S., & Budic, S. (2016). The impact of personal attitude, subjective norm, and perceived behavioural control on entrepreneurial intentions of women. Eurasian Journal of Business and Economics, 9(17), 23-35.

Echegaray, Fabian; Hansstein, Francesca Valeria (2016). Assessing the intention-behavior

gap in electronic waste recycling: the case of Brazil. Journal of Cleaner Production, (), S0959652616305285–. doi:10.1016/j.jclepro.2016.05.064

Fitriani, I., Widyawati, W., & Syafrial, S. (2021). Pengaruh Sikap, Norma Subjektif, Persepsi Kendali Perilaku terhadap Niat Perilaku Konsumsi Berkelanjutan Pembelian Makanan Berkemasan Ramah Lingkungan Foopak. Jurnal Ekonomi Pertanian Dan Agribisnis, 5(4), 1115–1125.

https://doi.org/10.21776/ub.jepa.2021.005.04.14

Ghozali, I., & Latan, H. (2015). Partial least squares konsep, teknik dan aplikasi menggunakan program smartpls 3.0 untuk penelitian empiris. Semarang: Badan Penerbit UNDIP.

Ginta, Y. V. S. (2022, April 13). Buang Limbah ke Sungai hingga Air Jadi Merah, Pengusaha Sablon di Denpasar Didenda Rp 2,5 Juta. Kompas.Com. denpasar.kompas.com/read/2022/04/ 13/173747078/buang-limbah-ke-sungai-hingga-air-jadi-merah-pengusaha-sablon-di-denpasar?page=all.

Ikbal, Mohammed, Rakesh Banerjee, Sanghamitra Atta, Dibakar Dhara, Anakuthil Anoop, and N. D. P. S. (2012). Synthesis, Photophysical and Photochemical Properties of Photoacid Generators Based on N-Hydroxyanthracene-1,9-dicarboxyimide and Their Application toward Modification of Silicon Surfaces. The Journal of Organic Chemistry, 77(23), 10557–10567.

Kuasirikun, N. (2005). Attitudes to the development and implementation of social and environmental accounting in Thailand. Critical Perspectives on Accounting, 16(8), 1035–1057. https://doi.org/10.1016/j.cpa.2004.02.004

Mersi. (2016). Tanggungjawab lLngkungan dan Peran Informasi Biaya Lingkungan dalam Pengambilan Keputusan Manajemen: Studi Kualitatif. Jurnal Ilmiah Revenue, 2(2), 1–18.

Morren, M., & Grinstein, A. (2016). Explaining environmental behavior across borders: A meta-analysis. Journal of Environmental Psychology, 47, 91–106.

https://doi.org/10.1016/j.jenvp.2016.05.003

Nguyen, H. Q., & Le, O. T. T. (2020). Factors Affecting the Intention to Apply Management Accounting in Enterprises in Vietnam. The Journal of Asian Finance, Economics and Business, 7(6), 95–107.

https://doi.org/10.13106/jafeb.2020.vol7.no6.095

Pangestika, S., & Prasastyo, K. W. (2017). Pengaruh Sikap, Norma Subjektif, Kontrol Perilaku yang Dipersepsikan Terhadap Niat Untuk Membeli Apartemen di DKI Jakarta. Jurnal Bisnis Dan Akuntansi, 19(1a-4), 249–255. http://jurnaltsm.id/index.php/JBA

Paschoalotto, M. A. C., Passador, J. L., Passador, C. S., & Oliveira, P. H. D. (2021). Local government performance: Evaluating efficiency, efficacy, and effectiveness at the basic education level. BAR-Brazilian Administration Review, 17.

Pemerintah Kota, D. (2015). Peraturan Daerah no 11 Tahun 2015 tentang Lingkungan Hidup. https://jdih.denpasarkota.go.id/produk-hukum/peraturan-perundang-undangan/perda/21

Povey, R., Conner, M., Sparks, P., James, R., & Shepherd, R. (2000). Application of the theory of p 2.pdf. 121–139.

Ramli, A., Razak, A., Nabilah, F., & Abdul Rasit, Z. (2019). Organisation Isomorphism as Determinants of Environmental Management Accounting Practices in Malaysian Public Listed Companies. International Conference on Accounting and Management. Faculty of Accountancy, Universiti Teknologi MARA Puncak Alam,

Ranggawari, G., Supriyatna, H., & Jingga, S. R. (2021). Petaka limbah pewarna. Validnews.Id; Valid News. https://www.validnews.id/nasional/petaka-limbah-pewarna

Ratnadi, N. M. D. (2014). Pengungkapan Corporate Social Reponsibility terhadap Nilai Perusahaan.pdf (p. Volume 01 No 2 Pp. 166-174). Jurnal riset Akuntansi.

Rosenwald, A., Wright, G., Chan, W. C., Connors, J. M., Campo, E., Fisher, R. I., Gascoyne, R. D., Muller-Hermelink, H. K., Smeland, E. B., Giltnane, J. M., Hurt, E. M., Zhao, H., Averett, L., Yang, L., Wilson, W. H., Jaffe, E. S., Simon, R., Klausner, R. D., Powell, J., … Staudt, L. M. (2002). The Use of Molecular Profiling to Predict Survival after Chemotherapy for Diffuse Large-B-Cell Lymphoma. New England Journal of Medicine, 346(25), 1937–1947. https://doi.org/10.1056/nejmoa012914

Sarstedt, M., Ringle, C. M., & Hair, J. F. (2021). Partial least squares structural equation modeling. In Handbook of market research (pp. 587-632). Cham: Springer International Publishing.

Sayoga, D. (2019). Buang Limbah ke Sungai, Satpol PP Kota Tertibkan Usaha Sablon di Jalan Pulau Misol - Pena Bali. Pena Bali. https://penabali.com/buang-limbah-ke-sungai-satpol-pp-kota-tertibkan-usaha-sablon-di-jalan-pulau-misol/

Seni, N. N. A., & Ratnadi, N. M. D. (2017). Theory of Planned Behavior untuk Memprediksi Niat Berinvestasi. 12, 4043–4068.

Shirokova, G., Osiyevskyy, O., & Bogatyreva, K. (2016). Exploring the intention–behavior link in student entrepreneurship: Moderating effects of individual and environmental characteristics. European Management Journal, 34(4), 386–399. https://doi.org/10.1016/j.emj.2015.12.007

Sisdyani, E. A., Subroto, B., Saraswati, E., & Baridwan, Z. (2020). Levers of eco-control and green behavior in medical waste management. International Journal of Energy Economics and Policy, 10(4), 194–204. https://doi.org/10.32479/ijeep.9342

Suparta, I. K. (2022). Tim DLHK Denpasar tertibkan usaha sablon yang cemari sungai -ANTARA News Bali. Bali Antara News.

https://bali.antaranews.com/berita/275497/tim-dlhk-denpasar-tertibkan-usaha-sablon-yang-cemari-sungai

Suryawan, I. W. K., Prajati, G., Afifah, A. S., & Apritama, M. R. (2021). Nh3-n and cod reduction in endek (Balinese textile) wastewater by activated sludge under different do condition with ozone pretreatment. Walailak Journal of Science and Technology, 18(6), 1–11. https://doi.org/10.48048/wjst.2021.9127

Tashakor, S., Appuhami, R., & Munir, R. (2019). Environmental management accounting practices in Australian cotton farming: The use of the theory of planned behaviour. Accounting, Auditing and Accountability Journal, 32(4), 1175–1202. https://doi.org/10.1108/AAAJ-04-2018-3465

Wang, Y., Liang, J., Yang, J., Ma, X., Li, X., Wu, J., Yang, G., Ren, G., & Feng, Y. (2019). Analysis of the environmental behavior of farmers for non-point source pollution control and management: An integration of the theory of planned behavior and the protection motivation theory. Journal of Environmental Management, 237(January), 15–23. https://doi.org/10.1016/j.jenvman.2019.02.070

Yadav, R., & Pathak, G. S. (2017). Determinants of Consumers’ Green Purchase Behavior

in a Developing Nation: Applying and Extending the Theory of Planned Behavior.

Ecological Economics, 134, 114–122.

https://doi.org/10.1016/j.ecolecon.2016.12.019

Zemore, S. E., & Ajzen, I. (2014). Predicting substance abuse treatment completion using a new scale based on the theory of planned behavior. Journal of Substance Abuse Treatment, 46(2), 174–182. https://doi.org/10.1016/j.jsat.2013.06.011

Jurnal Ilmiah Akuntansi dan Bisnis, 2023 | 133

Discussion and feedback