University Social Responsibility Reporting in Alignment with Sustainability Development Goals: A Conceptual Framework

on

Jurnal Ilmiah Akuntansi dan Bisnis

Vol. 18 No. 2, July 2023

AFFILIATION:

1,2,3 Faculty of Economics and Business, Universitas Brawijaya, Indonesia

*CORRESPONDENCE:

THIS ARTICLE IS AVAILABLE IN:

DOI:

10.24843/JIAB.2023.v18.i02.p03

CITATION:

Saraswati, E., Ghofar, A., Atmini, S.

& Dahlan, M. (2023). University Social Responsibility Reporting in Alignment with Sustainability Development Goals: A Conceptual Framework. Jurnal Ilmiah Akuntansi dan Bisnis, 18(2) 226-234.

ARTICLE HISTORY Received:

November 13 2022

Revised:

March 7 2023

Accepted:

June 27 2023

University Social Responsibility Reporting in Alignment with Sustainability Development Goals: A Conceptual Framework

Erwin Saraswati1*, Abdul Ghofar2, Sari Atmini3, Muhammad Dahlan4

Abstract

Universities, due to their significant energy consumption and use of non-renewable resources, have a responsibility towards environmental sustainability. This study seeks to establish a University Social Responsibility Reporting (USRR) framework, in line with the Sustainability Development Goals (SDGs), to address this issue. The framework takes into consideration key economic, environmental, and social factors, using disclosure concepts from the Global Reporting Initiative (GRI) Standards of 2016 and 2021. Relevant factors include indirect economic impacts, electricity consumption, employee rights, contributions and donations, customer service, welfare and work safety, training and development, and equal opportunities. The USRR framework also includes general disclosures as per SEOJK 16/2021, covering aspects like sustainability strategy, university profile, and governance. This approach emphasizes materiality and stakeholder participation to effectively address sustainability goals.

Keywords: general disclosure, sustainability development goals, topicspecific disclosure, university social responsibility reporting (USRR)

Introduction

The global community has recognized the imperative of implementing sustainability, with the United Nations leading the development of sustainability principles and criteria in collaboration with the Global Reporting Initiative (GRI) and the Sustainability Development Goals (SDG) (Sanches, 2019). The concept of sustainability emphasizes a balanced focus on the economy, society, and environment, using current resources in a manner that does not compromise the wellbeing of future generations. Hence, every organization, regardless of its nature or sector, is obliged to consider and contribute towards sustainability. This urgency is underscored by the alarming increase in greenhouse gases, which pose significant threats to environmental integrity. Consequently, the necessity for the adoption and application of sustainability principles is inescapable. This also extends to academic institutions, such as universities, which are not exempt from these global responsibilities.

Every organization, including universities, which enacts Corporate Social Responsibility (CSR) activities as part of sustainability implementation, has an opportunity to develop a CSR report, or a Sustainability Report. Such a report serves as a means of communication with internal and external parties and is expected to provide information related to the approach and the organizational level of CSR implementation (Hąbek & Wolniak, 2015). In the academic sphere, the CSR concept is referred to as University Social Responsibility (USR) (Speece, 2016; Jorge, 2017; Vasilescu et al., 2010; Kouatli, 2018).

Universities are major contributors to global warming, given the significant amount of greenhouse gases they produce. This is largely due to their extensive use of electricity and transportation, which account for 37% and 22% of CO2 emissions, respectively (Adha & Nurul, 2017). CO2 emissions from universities can be traced back to scopes 1, 2, and 3, with scope 1 having a direct impact and scopes 2 and 3 an indirect impact. Additionally, universities consume substantial quantities of irreplaceable resources such as paper and water.

The implementation of USR necessitates a conceptual framework for reporting on economic, social, and environmental activities - the triple bottom line. The Global Reporting Initiative (GRI) standards (2016; 2021) mandate the use of materiality to report matters significantly impacting the triple bottom line. Materiality, a principle vital in preparing a sustainability report (GRI Standard, 2016; 2021), is often underrepresented in several university sustainability reports in Indonesia. The existing sustainability reports only show alignment with the SDGs (e.g., UNHAS and IPB Sustainability Reporting, 2019).

The application of stakeholder theory in sustainability reports gives rise to the concept of materiality due to stakeholder involvement. Sustainability reports provide general disclosures mandated for every organization, including organizational strategy, leadership commitment, governance, and others. However, the disclosure of specific topics (Economic, Environmental, and Social) can vary across organizations. Therefore, it's crucial to determine the specific topics to be disclosed via a materiality matrix (GRI, 2016; 2021).

Aligning the sustainability report with the SDGs supports the achievement of the SDGs, contributing to the development of a healthy ecosystem in the market, such as rulebased market, a transparent financial system, and well-governed, corruption-free institutions. The SDGs offer a communicative language framework that aids organizations in delivering performance impacts (Frost et al., 2007). Universities, as key stakeholders, must exhibit commitment towards social and environmental matters through comprehensive reporting (Nicolo et al., 2021). University sustainability reporting is a response to accountability towards the community and other stakeholders, with the proactive implementation of USR having the potential to significantly influence societal development (Shek et al., 2017).

This study seeks to devise a conceptual framework for university sustainability reports by considering the concept of materiality in line with GRI standards and the SDGs. Universitas Brawijaya is used as a pilot project to identify materiality. This research presents a comprehensive sustainability report framework in accordance with the GRI Standard (2016; 2021), POJK 51 (2017) or SEOJK 16/2021, and the SDGs.

Research Method

This research adopts a case study methodology with a qualitative descriptive approach, focusing on Universitas Brawijaya (UB). Data collection involved semi-structured interviews with various stakeholders, such as active students, lecturers, university leaders like the Rector and Dean, educational personnel, alumni, prospective students, the local community impacted by UB's operations, and the Local Government of Malang City. These stakeholders were carefully chosen for their relevance to UB, both internal and external, the influence they experience from UB's operations, their governmental role, and their status as collaboration partners.

The data sought for this research encompass a variety of aspects. Firstly, it includes the sustainability strategy employed by the dean of FEB UB, which serves as a model for understanding the commitment of FEB officials to sustainability. It also incorporates the vision and mission of FEB UB regarding sustainability issues. The profile of FEB UB, complete with name, address, contact details, including telephone and facsimile numbers, email address, website, as well as any branch and representative offices, is also considered. In addition, the research seeks data on association membership, the number of employees and lecturers at FEB UB, and the gender breakdown amongst them. Finally, the research includes a brief overview of the organization's governance.

UB was chosen as the sample due to it having the largest student population in Indonesia. It is perceived as a representative of stakeholder opinions and a model for other universities. Data collection was executed using semi-structured interviews for primary data sources and a review of related literature for secondary data. The distribution of questionnaires was facilitated through a convenience sampling method. These questionnaires were designed based on Certified Sustainability Reporting Specialist (CSRS) certification training materials, with modifications specific to the University context.

The study sample consisted of 106 respondents (47 men and 59 women) categorized as follows: Approximately one third of the respondents were external stakeholders, comprising 5 alumni, 15 community members (representing small to midsized enterprises), and 3 partners or representatives from other universities. The remaining two thirds were internal stakeholders, including 18 lecturers, 40 students, and 25 education personnel, as provided in Table 1.

Table 1. Research Respondents

|

No. |

Composition |

Amount |

|

1 |

External Stakeholders: | |

|

- Alumni |

5 | |

|

- Society (UMKM) |

15 | |

|

- Partner/University |

3 | |

|

2 |

Internal Stakeholders: | |

|

- Lecturers |

18 | |

|

- Students |

40 | |

|

- Education Personnel |

25 | |

|

Total sample |

106 |

Source: Processed Data, 2022

This sample composition provides a balanced representation of both internal and external stakeholders. By including responses from both groups, the study captures a holistic understanding of the attitudes and perspectives regarding the University's social responsibility efforts. The external stakeholders such as alumni, community members, and partners offer valuable insight into the public perception and societal impact of the University's initiatives, while the internal stakeholders (lecturers, students, and educational personnel) provide an inside perspective on the University's approach to sustainability. This diverse mix of respondents ensures a comprehensive evaluation of the University's actions, strategies, and impacts from multiple angles, contributing to a robust and inclusive analysis. The responses gathered from both internal and external stakeholders serve as the foundation for identifying specific topics that should be disclosed.

Result and Discussion

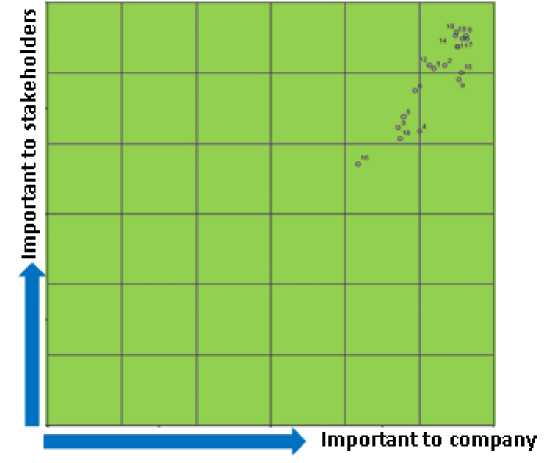

Stakeholder theory mandates organizations to engage with and consider the interests of their stakeholders. This includes involving stakeholders in determining the materiality of a sustainability report. "Material aspects" refer to those facets that embody significant social, economic, and environmental impacts on the organization or influence the evaluations and decisions of stakeholders (GRI, 2016; 2021).

The most critical materiality aspects, as represented in the upper right quadrant, encompass indirect economic impacts, electricity consumption, occupational health and safety, training and development, customer satisfaction and service, employee rights, contributions and donations, and equal opportunity. Additionally, these material aspects align with the objectives set forth by the Sustainable Development Goals (SDGs). The subsequent outcomes from the mapping of these materiality aspects play a significant role in the attainment of the SDGs.

The eight materiality aspects identified must be reported (as illustrated in Table 3) based on their impacts as perceived by internal and external stakeholders. Each aspect is further discussed below in terms of its material relevance to stakeholders.

Indirect economic impact largely originates from the owners of boarding houses and Small and Medium Enterprises (SMEs) around Universitas Brawijaya (UB). A significant positive impact is the income generated for these business owners from students, thereby stimulating economic growth. Consequently, the existence of UB yields economic benefits to the surrounding stakeholders. UB should disclose the percentage of economic growth of the surrounding community or the proportion of total stakeholders affected. This indirect economic impact can potentially reduce unemployment, alleviate poverty, and contribute to community wellbeing, aligning with SDGs 1 and 11.

Electrical energy, a major contributor to global warming, is predominantly consumed by UB for air conditioning, lighting, LCD displays, and elevators. Despite being a Scope 2 (tier 2) emission source, electricity consumption indirectly results in carbon emissions. UB should regularly report on energy reduction measures, detailing plans for implementation. Such measures could include transitioning to solar energy, improving natural ventilation, and optimizing lighting. Utilizing solar and wind energy not only reduces electricity consumption but also promotes clean energy use, aligning with SDGs 7 and 12.

Table 2. Materiality Matrix

Materiality Matrix and o. Material Topics

-

1 Indirect Economic Impact

Electricity energy consumption

Water recycled and reused

4

5

6

7

8

9

Energy indirect (AC, LCD) Carbon Emission Mitigation

New employee hires Occupational Health and Safety

Training and Development Remuneration and rewards

10 Customer Satisfaction

-

11 Employee rights

Contribution and Donation

-

13 Customer Care

-

14 Equal Opportunity

Diversity and Human

Rights

16 Political contributions

Customer health and 17

safety

Carbon Footprint

Management

Source: Processed Data, 2022

UB should disclose its occupational health and safety practices, detailing the measures in place to prevent accidents and ensure a safe work environment. This aligns with the commitment to ensuring health and wellbeing for all, as stipulated in SDG 3.

UB should disclose measures taken to gauge and improve customer (student) satisfaction. Information on service provision to students should also be provided. Such disclosure would demonstrate the university's commitment to achieving its organizational goals, in line with SDG 17.

UB should disclose its employee training and development programs, detailing the frequency of training, the programs provided, and how these contribute to performance improvement and career development. Ultimately, employee training and development aligns with the objectives of SDGs 4 and 16 to strengthen institutions and promote quality education.

Table 3. Materiality in line SDGs

|

Materiality Aspects |

Goals |

SDGs Target | |

|

Indirect economic impact |

1 |

No Poverty | |

|

1 |

11 | ||

|

Sustainable cities and communities | |||

|

7 |

Affordable and clean energy | ||

|

2 |

Electrical consumption |

12 |

Responsible consumption and production |

|

7 |

Occupational health and safety |

3 |

Good Health and well-being |

|

8 |

Training and development |

4 16 |

Quality Education Peace, Justice, and Strong Institution |

|

Customer satisfaction and |

Partnership for The Goals | ||

|

10 |

service |

17 | |

|

11 |

Employee rights |

16 |

Peace, Justice, and Strong Institution |

|

12 |

Contributions and donations |

1 |

No Poverty |

|

14 |

Equal opportunity |

5 |

Gender Equality |

|

10 |

Reduced Inequalities |

Source: Processed Data, 2022

In compliance with the GRI Standard (2021), UB should report on its adherence to human rights principles, particularly in relation to its employees. This would demonstrate the university's commitment to fostering strong institutions and promoting peace and justice, in line with SDG 16.

UB should disclose its contributions and donations to stakeholders in need. Such disclosures are expected to underscore the university's commitment to reducing poverty, aligning with SDG 1.

UB should provide detailed disclosures on equal opportunities between men and women in relation to remuneration and positioning within the organization. Such disclosures support gender equality and efforts to reduce inequality, in line with SDGs 5 and 10.

Sustainability reports should include general information that details the organization's vision and mission, strategy statements, sustainability commitments from leaders, and organizational profiles. This is in line with SEOJK 16/2021 to foster a comprehensive, sustainable organization while managing risks and achieving expected results.

This section outlines the university's vision and mission in executing its sustainability strategy and the ensuing impact from the university's operations. It elaborates on how universities enact sustainability measures in alignment with the SDGs, thereby fostering sustainability values among stakeholders. This strategy, given its high-level nature, is a representation from the highest leadership in the organization, namely the chancellor and their team. An example of a sustainability strategy statement from a Dean is provided in the attachment for reference.

The profile disclosure gives a comprehensive overview of the university, encapsulating its vision, mission, and values related to sustainability. Additionally, it includes specific information like the university's address, number of faculties and study programs, staff headcount, and organizational memberships.

This section presents insights from the university's top leadership, including: Policies developed in response to sustainability strategy issues and strategies to address

General Disclosure

Sustainability Strategy

University Profile

Explanation from Top Management

University Governance

Specified Topic Disclosure

Economic

Environment

Social

Employee Rights (SDGs 16)

Indirect Economic Impact (SDGs 1 and 11)

Electricity Consumption (SDGs 7 and 12)

Contribution and Donation (SDGs 1)

Customer Satisfaction (SDGs 17)

Occupational Health and Safety (SDGs 3)

Training and Development (SDGs 4 and 16)

Equal Opportinity (SDGs 5 and 10)

Figure 1. University Social Responsibility Reporting Conceptual Framework Source: Processed Data, 2022

these issues; b. Progress towards achieving sustainability performance targets; c. An outlined sustainability roadmap.

Sustainability governance features information about the university's commitment to implementing sustainable governance, with special consideration for economic, social, and environmental aspects. The preparation and disclosure of sustainability reports necessitate active involvement from the management and engagement with stakeholders. The methodology for stakeholder involvement is to be described in the management approach.

This research identifies the topics and disclosures that are necessary for a comprehensive sustainability report, as illustrated in Figure 1. By discussing general disclosures and specific topics, we propose a conceptual framework for university social responsibility reports, aiding in the development of a University Sustainability Report. The USRR is designed based on the level of materiality, emphasizing crucial disclosures and their impact on economic, social, and environmental stakeholders. The sustainability reports, crafted with a focus on materiality, reveal essential elements for the University before aligning them with the SDGs. The USRR incorporates general disclosures, which are obligatory according to GRI standards, and specific topics pertaining to the economy, society, and environment.

Conclusion

Universities must address the issue of greenhouse gases, a leading contributor to global warming. The use of electricity and transportation by universities contributes to 37% and 22% of CO2 emissions respectively. These CO2 emissions originate from Scopes 1, 2, and 3, where Scope 1 has a direct impact and Scopes 2 and 3 have indirect impacts. In addition, significant amounts of irreplaceable resources, such as paper and water, are consumed in universities. Consequently, universities must fulfil their social responsibilities.

This study's objective is to establish a conceptual framework for constructing a university sustainability report pertaining to social responsibility. Through an examination of 106 respondents, this study identified materiality topics needed in disclosing economic, social, and environmental matters. Identified materiality topics include indirect economic impacts (SDGs 1 and 11) as an economic aspect; consumption of electrical energy (SDGs 7 and 12) as an environmental aspect; and multiple social aspects, such as occupational health and safety (SDG 3), customer satisfaction and service (SDG 17), training and development (SDGs 4 and 16), employee rights (SDG 16), contributions and donations (SDG 1), and equal opportunities (SDGs 5 and 10).

General disclosures mandated by SEOJK 16/2021, such as sustainability strategies, university profiles, statements from top management, and university governance, must align with the SDGs. One limitation of this research is the challenge of acquiring data from the university's top leadership due to their demanding schedules. The study primarily relies on data from the Faculty of Economics and Business, where the researcher is employed, due to ease of access. The intent is for these findings to be representative of all universities, especially regarding specific topics. This research can contribute a framework that could be utilized by other universities beyond UB. Additionally, the implications of this research support the stakeholder theory.

References

Bebbington, J. & Larrinaga, C. (2014). Accounting and sustainable development: An exploration. Accounting, Organizations and Society 39 (2014) 395-413.

Bellantuono, N., Pontrandolfo, P., & Scozzi, B. (2016). Capturing the Stakeholders’ View in Sustainability Reporting: A Novel Approach. MDPI Sustainability Journal.

Bertelsmann Stiftung and Sustainable Development Solutions Network. (2018). Global Responsibilties: Implementing the Goals. SDG Index and Dashboards 2018. Diakses dari https://www.sdgindex.org/reports/sdg-index-and-dashboards-2018/

Deegan, C. (2004). Financial Accounting Theory. McGrow-Hill Book Company; Sidney.

Donaldson, T. & Preston, L.E. (1995). The Stakeholder Theory of the Corporation: Concepts, evidence, and implications. Academy of Management Review 20: 6591.

Freeman, R.E. (1984). Strategic Management. A stakeholder approach. Pitman: Boston.

Gray, R., Kouhy, R., & Lavers, S. (1995). Constructing A Research Database of Social and Environmental Reporting by UK Companies. Journal of Accounting, Auditing and Accountability. Vol. 8, pp. 47-77.

Hąbek, P & Wolniak, R. (2015). Assessing the quality of corporate social responsibility reports: the case of reporting practices in selected European Union member states. Silesia University of Technology: Poland.

Jones, S., G. Frost, J. Loftus, and S. van der Laan. (2007). An Empirical Examination of the Market Returns and Financial Performance of Entities Engaged in Sustainability Reporting. Australian Accounting Review Vol. 17 No. 1 pp. 78.

Kurniawan, T., Sofyani, H., dan Rahmawati, E. (2018). Pengungkapan Sustainability Report dan Nilai Perusahaan: Studi Empiris di Indonesia dan Singapura. Kompartemen: Jurnal Ilmiah Akuntansi, Vol. XVI, No1, 1-20.

Panuluh, S. dan Meilia R.F. (2016). Perkembangan Pelaksanaan Sustainable Development Goals (SDGs) di Indonesia. Briefing Paper 02. International NGO Forum on Indonesian Development (INFID).

PwC. (2016). 19th Annual Global CEO Survey: Redifining business success in a changing world. Diakses dari https://www.pwc.com/gx/en/ceo-survey/2016/landing-page/pwc-19th-annual-global-ceo-survey.pdf diakses pada 21 Juli 2019.

Sánchez, Isabel M. G., Nazim Hussain, Jennifer M., & Emiliano R. (2019). Impact of disclosure and assurance quality of corporate sustainability reports on access to finance. Corporate Social Responsibility and Environmental Management 2019, 1–17.

Suchman, M. C. (1995). Managing Legitimacy: Strategic and Institutional Approaches. Academy of Management Journal, Vol. 20, No. 3, pp. 571 - 610.

Jurnal Ilmiah Akuntansi dan Bisnis, 2023 | 234

Discussion and feedback