Reduced Audit Quality Practices among Local-Government’s Internal Auditors: What to do with Stress and Working Condition

on

Jurnal Ilmiah Akuntansi dan Bisnis

Vol. 18 No. 1, January 2023

AFFILIATION:

1,2,3Faculty of Economics and Business, Brawijaya University, Indonesia

*CORRESPONDENCE:

rintoariwibowo@student.ub.ac.id

THIS ARTICLE IS AVAILABLE IN:

DOI:

10.24843/JIAB.2023.v18.i01.p07

CITATION:

Ariwibowo, R., Nurkholis, & Saraswati, E. (2023). Reduced Audit Quality Practices among LocalGovernment’s Internal Auditors: What to do with Stress and Working Condition? Jurnal Ilmiah Akuntansi dan Bisnis, 18(1), 90-114.

ARTICLE HISTORY Received:

23 September 2022

Revised:

30 October 2022

Accepted:

11 November 2022

Reduced Audit Quality Practices among Local-Government’s Internal Auditors:

What to do with Stress and Working Condition?

Rinto Ariwibowo1*, Nurkholis2, Erwin Saraswati3

Abstract

This study aims to reveal the influence and effect of stress and its predecessor through the lens of Job-Demand Resource Theory (JD-R). This research utilizes the quality of working life and work interference with personal life as predictors of stress and reduced audit quality practice. The subjects of this study involved 326 local government internal auditors in Bali Area. Quantitative analysis using PLS-SEM demonstrated both predictors’ effects in forming auditor’s stress. The study also confirms that stress mediates the formation of reduced audit quality practices among auditors. The result of the study is expected to give strategic recommendations to Government Internal Control Apparatus/Aparat Pengawasan Intern Pemerintah (APIP) management to promote better stress management and work-life balance programme, expecting to prevent dysfunctional audit practices while optimizing their audit quality.

Keywords: job demand resource theory, quality of working life, work interference with personal life, job stress, reduced audit quality practice

Introduction

The urgency of professional practice implementation among government auditors is related to the government’s agenda to increase the capability of APIP institutions. APIP comprise the internal control institutions of government ministries and agencies, including the local government inspectorate. In addition, APIPs play a role in the government projects internal supervisory function. Since the Indonesian government has adopted the Internal Control Capability Model (IA-CM), all APIPs must comply with several capability criteria. The capability model reflects APIP capacity and ability to do and exercise their roles as internal auditors within their scopes and responsibilities. Moreover, the capability level assessment criteria are regulated at the institutional level and more specific to the auditor’s personal and professional practice (BPKP, 2015). Hence, in this point of view, personal and professional practice among auditors is becoming crucial in line with the government agenda.

Statistics on the APIP capability model are still under specific challenges. For example, in 2021, more than half (51.11%) of the APIP institutions have not reached the expected capability level; most, or 86%, are local government institutions varying between provincial and district/municipal levels. Meanwhile, specific statistics covering the number of Local Government APIPs show that there are still 42.44% have not met the expected target (BPKP, 2021). The reflection of these statistical numbers still indicates that until recently, the government’s capability agenda on national APIP institutions still faces challenges, especially for the local government institution.

Standard regulations set by professional bodies Indonesia’s Government Internal Auditors Association (Asosiasi Auditor Intern Pemerintah Indonesia/AAIPI) state that government auditors must have the knowledge, skills, and competencies required for their supervisory assignments. Standard also specifically regulates professional auditor performance, noting that auditors must have professional skills and accuracy in carrying out their assignments. The AAIPI formal statement even technically and explicitly states that the government’s internal auditor must be able to carry out adequate identification, analysis, evaluation, and documentation in achieving their assignments’ objectives (AAIPI, 2019, 2021)

On the other hand, the quality of audit results might be measured by comparing audit procedures to the referring audit standards and regulations (Widiastuty & Febrianto, 2010). The concept of this quality audit results from a practical point of view relates to the description and the terminology of the typical quality audit concept. Widiastuty & Febrianto (2010) summarise the discussion of this concept based on two main views, namely: (1) the independence of practitioners and (2) the competencies of the auditors. Both two concepts directly or indirectly affect the quality of audit results. Practitioner independence refers to the auditor’s ability to maintain the behaviour following the references of standards and regulations (planning, work programs preparation, implementation, verification, and preparation of audit reports). Meanwhile, the second quality determinant might refer to the auditors’ competence and capability in knowledge, experience, expertise, and troubleshooting skills within the technical process of the audit assignment.

Generally speaking, the discussions on quality audit results can be conceptualized into a more straightforward and pragmatic approach. In this point of view, understanding the conformity of audit practices and applicable auditing standards is crucial in determining the audit quality itself. Hence, professional ethics and procedural professional practice compliance could become alternative parameters for measuring audit quality. Referring to the standards, the Indonesian Government Internal Auditor Association (AAIPI) issued professional and procedural standards which apply to all APIPs. Therefore, all Indonesian government internal auditors are obliged to enforce regulations and auditing standards (AAIPI, 2021). In addition, state institutions’ regulations and technical measures also regulate APIP procedural steps and technical quality control which is explicitly enforced under the technical regulation – lex specialis – of Government Regulation No. 60 of the year 2008 (Indonesian regulation on Government Internal Control System/GICS).

Meanwhile, the reduced audit quality practice (RAQP) is contrary to the ideal professional practice conceptualized by the regulation and standards. This practice is systemic action that could directly or indirectly reduce the quality of audit result quality

(Amiruddin, 2019; Anugerah et al., 2016; Smith & Emerson, 2017; Smith et al., 2017). The manifestations of these practices include (1) preparation of audit reviews that are not based on sufficient evidence, (2) incomplete audit steps, and (3) other actions that reduce audit procedures or work below standards (Smith & Emerson, 2017). This practice is systemic and could negatively affect audit result quality (Coram et al., 2003; Donnelly & Quirin, 2003). Reduced audit quality practice is also viewed as dysfunctional behaviour in all aspects of auditing (Paino et al., 2010). Therefore, this practice is also deemed a contrary point within the code of ethics and standards (AAIPI, 2019, 2021). Additionally, reduced audit quality practice is an alternative measurement approach to behaviour-related phenomena by using the reversed construct – antithesis – denoting the concept of the audit result quality.

Meanwhile, by considering the predictors of dysfunctional behaviour, several previous studies show the interrelation between auditors’ stress and the incidence of reduced audit quality practice (Amiruddin, 2019; Smith & Emerson, 2017; Smith et al., 2017). The study indicates that auditors with limited time and resources are more susceptible to job stress. It also stated that stress could increase the tendency to reduce audit quality practice (Amiruddin, 2019; Smith & Emerson, 2017; Smith et al., 2020; Smith et al., 2017). The study also reveals comprehensive influential factors which imply the stress phenomenon among auditors’ dysfunctional behaviour. The role of stress consisting of limited work resources, excessive workload, and limited working knowledge may increase workers’ psychological pressure, further complicating the job stress.

The stress paradigm in the lens of Job-Demand Resource (JD-R) Theory explains the mechanism and the formation of job stress within two interrelated factors, namely: (1) job resources and (2) job demands. This theory states that job stress may occur when the job resources are no longer answered or adequately sufficient to tackle job demands (Bakker & Demerouti, 2014b). Within the auditor context, JD-R theory may explain the auditor job resource as all capabilities embedded in the personal and auditor job characteristics, which give them a reasonable choice to stay. Capability includes all aspects of competencies, knowledge, and skill to make them work smoothly. The resource may also be related to the actual job resource provided by the quality of the working environment, consisting of sufficient financial support, time, and tools that provide sufficiency to the auditor to finish their job. In contrast, job demand naturally arises from the demand originating from the job, consisting of obligatory assignment, the inevitable specific job requirements, and other aspects which force the workers to do something within their job context (Bakker et al., 2001). Under this lens, stress happens when the auditor's job resource cannot sufficiently answer or tackle these inevitable forces.

Job Demands-Resource Theory reveals that job demands affect the formation of psychological stress and fatigue, which then manifests into burnout, one of the side effects of job stress (Roskams & McNeely, 2021). Job demands naturally arise from the assignment of jobs, the work environment, and other aspects workers face in completing their jobs (Bakker et al., 2001). Job demands can be a physical or psychological burden that drains personal resources, resulting in psychological exhaustion (Roskams & McNeely, 2021).️ This concept is contextually related to any auditor pressure concerning interference, which inevitably affects their personal life

Quality of working life (QWL) may resemble the concept of job resources. Under the same conceptualization, quality of working life provides a comprehensive assessment

of both personal capability and job resources provided by the working environment. Quality of working life (QWL) describes the auditor’s perception of the desired working conditions. Quality of work life is identified through adequacy of remuneration based on justice, ethics, good working environment, security, safety, and social integration. This condition can encourage the growth of skills and workers’ potential (Narehan et al., 2014). Quality of working life is also stated to support workers’ psychological resilience by developing and increasing workers’ skills and personal initiatives (Serey, 2006). By the rationale of its commonalities with the job resource terminology, Quality of Working Life (QWL) could be an alternative predictor of resilience by preventing the formation of auditor stress and consequently reducing the incidence of reduced audit quality practices.

Conversely, work interference with personal life (WIPL) plays the opposite role as inevitable job demand. This interference might be formed as disturbances and other interruption conditions from the working environment, affecting the auditor’s personal life (Fisher et al., 2009). In the description of the Job Demands and Resources model, work interference with personal life has a conceptual closeness with the job demands experienced by the auditor. In line with the theoretical framework of JD-R Theory, work interference with personal life (WIPL) could also be utilized as a stressor, factors forming auditor stress and its complications.

Through understanding Job-Demand Resource Theory, the stress experienced by the auditor occurs due to the auditor’s quality of working life (QWL) no longer being able to tackle work pressure in the form of interferences. Research conducted by Salehi et al. (2020) revealed an indirect relationship between the low quality of life and its contribution to forming job burnout as one of the complex forms of stress. Fogarty & Kalbers (2006) revealed a similar phenomenological relationship between job demand and job stress among internal auditors. Based on theoretical considerations and previous research studies, the following research hypotheses were formulated.

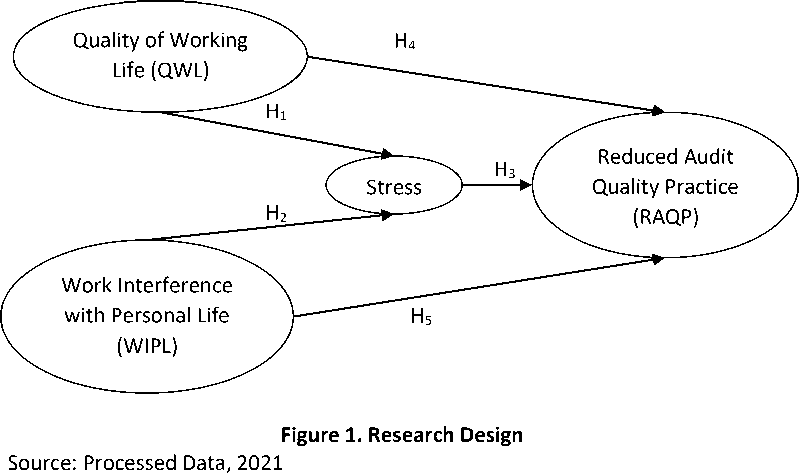

H1: The auditor’s quality of working life has a negative impact on the formation of auditor stress.

H2: The auditor’s work interference with personal life has a positive impact on stress.️

Stress levels are measured based on perceptions of psychological symptoms experienced by workers (Smith & Emerson, 2017; Smith et al., 2020; Smith et al., 2017), including compulsive thinking, symptoms of anxiety (anxiety), thoughts of disturbances that trigger emotions, and uncomfortable thoughts. Research also confirmed a significant positive relationship between stress levels and burnout – a complex form of prolonged stress – on auditors. In addition, job pressure is a strong predictor of auditors’ stress (Amiruddin, 2019; Smith & Emerson, 2017; Smith et al., 2020; Smith et al., 2017).

Asriningpuri & Gruben (2021) studied the effect of budget pressure on auditors and revealed the significant connection affecting the incident of auditors’ dysfunctional behaviour. Persiani & Tjiptohadi (2015) showed the same significance concerning time pressure, which resulted in reduced audit quality practice among auditors. The research by Elinda et al. (2019) uses a multidimensional predictor of the role of stress in predicting reduced audit quality practice among auditors resulting in a significant positive correlation between dysfunctional audit quality practices.

Reduced audit quality practices (RAQP) are also becoming a form of counterproductivity in the context of auditor performance. The Job Demand-Resource (JD-R) Theory as stipulated by Roskams & McNeely (2021) explains the indirect effect on

performance as stress consequences. The relationship between job demand and resources can contribute to counter-productive practices on auditor performance (RAQP). Based on theoretical considerations and previous research studies, the following research hypotheses were formulated.

H3: Stress experienced by auditors increases the incidence of reduced audit quality practice among auditors.

H4: Quality of working life has a negative effect on reduced audit quality practice among auditors.

H5: Work interference with personal life has a positive effect on the incidence of reduced audit quality practice.

The research mentioned earlier cited on RAQP and occupational stress generally utilize the Conservation of Resource Theory (COR) denoting the single influential factor of occupational stress; the theory stipulates single occupational stress forming factor related to the threat or disturbances of job resources. While considering the extensive theory on occupational stress, JD-R theory proposes a more comprehensive notion of occupational stress by utilizing the double forming factor of occupational stress, involving job resources and job demand as a “see-saw” mechanism.️ Under this theoretical paradigm, occupational stress is more likely to happen when job resource is no longer available to counterbalance the job demand. The JD-R theory also develops a more practical model for evaluating the relationship and impact of occupational stress on workers’ performance (Bakker & Demerouti, 2007; Bakker & Demerouti, 2014a, 2017a; Roskams & McNeely…, 2021) rather than only mentioning occupational stress as a theoretical focus. Considering these contrast points, JD-R theory is suitable to explain occupational stress and, more importantly, could practically elaborate the impact towards workers’ performance, and as an anthesis construct on this study context, the reduced audit quality practice (RAQP).

This study is intended to explain the relationship between two factors contributing to auditors’ occupational stress and its complication toward auditor dysfunctional practice. In contrast with previous research, this study uses the quality of working life as an alternative proxy to the auditors’ job resources and work interference

with personal life as the auditors’ job demand.️ This study also aims to explore contextual novelty on occupational stress under uncertain background conditions caused by the pandemic, specifically by observing local government auditors in Indonesia. Furthermore, this study also expects to comprehend better occupational stress related to the auditors’ dysfunctional behaviour by using the JD-R theory, which to the best of our knowledge still rarely applied within occupational stress studies in Indonesia.

The research model was developed by considering the relationship between variables and hypothesis statements. Quality of working life and work interference with personal life are exogenous variables to predict auditor stress and reduced audit quality practice. The research model aims to answer the research objectives, revealing the influential factors of reduced audit quality practice and its predecessor through the lens of Job-Demand Resource Theory (JD-R). This research utilizes quality of working life and work interference with personal life as exogenous predictors of stress which is further hypothesized to be the factors or antecedents forming reduced audit quality practice (Figure 1).

Research Method

The primary research method is a quantitative approach. This study utilized primary data collection through a questionnaire instrument. In addition, the qualitative approach in the form of interviews is also employed to provide a broader picture of perceptions allowing to development of deeper research discussion and adding commentaries into contextual background research discussion. This additional approach is expected to provide comprehensive and better research conclusions (Creswell & Clark, 2017).

The subject of this research was active government internal auditors working in the local government APIP in the Bali region. The research population consists of 336 auditors in ten Local Government APIP institutions in Bali Region. Bali has been chosen as the locus of study to consider the effect of pandemic strains on the tourism industry which stated to be systematically impacted people’s lives within the area (Subadra & Hughes, 2022; Yuniti et al., 2020) and subsequently trigger elevating challenges for the public sector officials, elevating challenge classically related to the likelihood of occupational stress (Prijanka et al., 2021). The area is also comprised of ten local government units varying at provincial, municipal, and district levels with the heterogenous condition within a restricted area; these characteristics could reflect brief respondent characteristics while maintaining ease of technical data collection.

The specific respondent’s profile consists of Functional Auditors (Pejabat Fungsional Auditor/PFA) and Supervisors for implementing Government Affairs (Pengawas Penyelenggaraan Urusan Pemerintahan di Daerah /P2UPD). A functional auditor (PFA) is a civil servant with a definitive operational auditor position and a definitive professional background (certified). P2UPD are endorsed with specific acts of duty issued by local government regulation under the Ministry of Home Affairs, assigned supervisory tasks similar to the auditor job characteristic. Therefore, both profiles are government auditors functionally in charge of supervisory assignments in local government APIPs. In sample-wise, both PFA and P2UPD are not explicitly classified into different groups and are treated the same. Simple random sampling is used to provide a more general population presentation.

Table 1. Measurement and Operationalization

|

No. |

Variable |

Measurement* |

Adaptation | |

|

Operational Terminology |

Indicator | |||

|

1 |

Quality of Working Life (QWL) |

Auditors’ psychological perceptions regarding their working life. Including several qualitative characteristics of remuneration, justice, ethics, safety, and social integration. |

Dimensional Consists of 7 dimensions, 12 reflective indicators |

Sabonete et al. (2021) |

|

2 |

Work Interference with Personal Life (WIPL) |

Auditors psychological perception of any disturbances and overlapping demands affecting their personal life originating from their working life. This perception includes qualitative judgment on how their working life affects their personal life in terms of extra-working hours, extra-emotional attachment, and other forms. |

Five reflective indicators |

Gim and Ramayah (2020) |

|

3 |

Stress (STRES) |

Qualitative judgment refers to auditors’ physical and psychological anxiety, worry, and rumination. |

Four reflective indicators |

Smith and Emerson (2017) |

|

4 |

Reduced Audit Quality Practice (RAQP) |

All forms of practice result in the reduction of audit quality. Includes any practice of all forms of practice or actions in carrying out the assignments or work that can reduce the audit quality result or other things that are contrary to government internal audit standards. |

Four reflective indicators |

Smith and Emerson (2017) |

*The detail of each measurement indicator is shown in the appendices

Source: Processed Data, 2021

The minimum sample size to form the research model is 266, calculated using G*Power Statistics regarding effect size parameters of 0.20, a significance level of 0.05, and a statistical power of 0.95. Additionally. to maximize the collectability of the research instrument, the questionnaire was distributed to all population subjects in Bali (all 336 population-wise).

The questionnaire used four-response Lickert questions/statements adopted from previous studies. The pilot test is also conducted before the research to ensure that the instrument meets adequate validity and reliability criteria.

This study utilizing Non-Linear Partial Least Square – Structural Equation Modelling/PLS-SEM as a statistical analytical tool, considering its flexibility for various research purposes, theoretical confirmation, predicting the influence between variables, and other objectives (Astrachan et al., 2014; Benitez et al., 2020; Hair et al., 2017). PLS-SEM is also commonly used for Exploratory Factor Analysis (EFA), which can also be helpful for Confirmatory Factor Analysis (CFA)-based testing. CFA testing is commonly used for theoretical confirmation within a priori theories and concepts that have been previously developed (Sholihin & Ratmono, 2021).

The research procedure includes sequential steps, e.g. (1) path model specification, (2) measurement model specification, (3) data collection or screening, (4) model estimation, (5) measurement model evaluation/testing, (6) evaluation/testing of structural models, and then (7) interpretation of results and conclusions. This study uses Warp-PLS software to provide non-linear approach modelling. Therefore, the approach is considered more realistic for personal perception and behaviour study (Sholihin & Ratmono, 2021).

The interviews employed unstructured inquiries to the auditor with the same study subject profile. Additional information was also gathered from the local representative office of Badan Pengawasan Keuangan dan Pembangunan (BPKP) Indonesia’s Internal Control Agency representative office in Denpasar. The additional informants support the triangular information regarding the Bali regional APIP supervisory and monitoring. Consultant and instructor in BPKP Denpasar were deemed to have a comprehension of various technical troubleshooting abilities in the context of APIP capability development within the area, including working culture development related to this study’s issue. The respondents were chosen conveniently while delivering or collecting returns of the questionnaire packages.

Result and Discussion

Primary data collection during June – July 2022 has collected 326 questionnaires (above minimum sample-size number) from ten local government APIPs in the Bali area. All instruments collected are deemed complete and can be followed up with statistical modelling analysis. The instrument collection also reflects all forms of local government in Bali, consisting of Municipal, Regency, and Provincial APIP. Descriptive statistics from the results of data collection are described in table 2.

The details of the questionnaire collected from the local government in the Bali area, including the Inspectorate of Bangli Regency (20 questionnaires/6.13%); Denpasar City (29 questionnaires/8.90%); Gianyar Regency (40 questionnaires/12,27%); Buleleng Regency (16 questionnaires/4.91%); Jembrana Regency (15 questionnaires/4.60%); Karangasem Regency (21 questionnaires/6.44%); Badung Regency (47 questionnaires/14.42%); Tabanan Regency (53 questionnaires/16.26%); Klungkung Regency (25 Questionnaires/7.67%), and Inspectorate of Bali Province (60 Questionnaires/18.40%).

Table 2. Descriptive Statistics

|

Ind. Var.* |

1 |

Lickert R 2 |

esponses 3 |

4 |

Min. |

Max. |

Modes |

Std. dev. |

|

QWL1.1 |

29,45% |

43,25% |

21,47% |

5,83% |

1 |

4 |

2 |

0,86 |

|

QWL1.2 |

52,45% |

35,58% |

10,12% |

1,84% |

1 |

4 |

1 |

0,74 |

|

QWL2.1 |

9,20% |

46,32% |

40,49% |

3,99% |

1 |

4 |

2 |

0,71 |

|

QWL3.1 |

2,45% |

6,44% |

79,14% |

11,96% |

1 |

4 |

3 |

0,53 |

|

QWL3.2 |

2,15% |

11,04% |

67,18% |

19,63% |

1 |

4 |

3 |

0,63 |

|

QWL4.1 |

4,60% |

21,47% |

67,79% |

6,13% |

1 |

4 |

3 |

0,63 |

|

QWL5.1 |

13,50% |

22,70% |

59,20% |

4,60% |

1 |

4 |

3 |

0,78 |

|

QWL5.2 |

7,67% |

13,50% |

69,94% |

8,90% |

1 |

4 |

3 |

0,70 |

|

QWL6.1 |

2,15% |

16,87% |

76,07% |

4,91% |

1 |

4 |

3 |

0,53 |

|

QWL7.1 |

0,92% |

5,52% |

76,99% |

16,56% |

1 |

4 |

3 |

0,50 |

|

QWL7.2 |

1,23% |

2,15% |

65,64% |

30,98% |

1 |

4 |

3 |

0,56 |

|

QWL8.1 |

1,23% |

14,42% |

64,11% |

20,25% |

1 |

4 |

3 |

0,63 |

|

QWL8.2 |

1,23% |

14,42% |

76,69% |

7,67% |

1 |

4 |

3 |

0,51 |

|

SA1 |

23,93% |

60,12% |

12,58% |

3,37% |

1 |

4 |

2 |

0,71 |

|

SA2 |

25,77% |

61,35% |

10,43% |

2,45% |

1 |

4 |

2 |

0,67 |

|

SA3 |

22,09% |

62,58% |

13,80% |

1,53% |

1 |

4 |

2 |

0,65 |

|

SA4 |

34,97% |

54,29% |

8,90% |

1,84% |

1 |

4 |

2 |

0,68 |

|

WIPL1 |

8,28% |

60,74% |

25,77% |

5,21% |

1 |

4 |

2 |

0,69 |

|

WIPL2 |

14,11% |

75,46% |

9,20% |

1,23% |

1 |

4 |

2 |

0,53 |

|

WIPL3 |

13,50% |

69,63% |

15,03% |

1,84% |

1 |

4 |

2 |

0,60 |

|

WIPL4 |

25,77% |

68,10% |

4,91% |

1,23% |

1 |

4 |

2 |

0,57 |

|

WIPL5 |

16,26% |

65,95% |

16,56% |

1,23% |

1 |

4 |

2 |

0,61 |

|

RAQP1 |

22,70% |

66,56% |

10,43% |

0,31% |

1 |

4 |

2 |

0,57 |

|

RAQP2 |

67,79% |

24,85% |

6,13% |

1,23% |

1 |

4 |

1 |

0,66 |

|

RAQP3 |

57,67% |

35,89% |

5,83% |

0,61% |

1 |

4 |

1 |

0,64 |

|

RAQP4 |

49,69% |

44,48% |

5,83% |

0,00% |

1 |

3 |

1 |

0,60 |

*Indicator variables notes described in the appendices Source: Processed Data, 2022

The respondent demographic illustrated a relatively equal number of male and female respondents. More than half of the survey respondents were undergraduate and graduate university level consisting of 62.9%, while the rest percentage consisted post graduate level. The majority of the respondent was in the group ages 36 – 40, consisting of 19.3%, while the age group of more than 40-year-old for 64.4%. The demographic also shows the variation in auditor position as follows: Auditor Pelaksana (35.6%); Auditor Pertama (39%); Auditor Muda (24.2%); and Auditor Madya (1.2%).

The measuring model test ensures that the research model has met the reliability and validity criteria for all indicators and dimensions forming the latent variables. The measuring model test consists of (1) convergent validity, (2) internal consistency reliability, and )3( discriminant validity (Hair et al., 2017).

The results of the convergent validity test by utilizing the information on the loading factor on each indicator and dimensions forming latent variables values between 0.520 to 0.917. Sholihin & Ratmono (2021) explain that loading factors ranging from 0.40 to 0.70 could be maintained for exploratory and pioneering research. Additionally, Hair et

al. (2017) are also stressing out that the loading factor for the following range could be maintained along with considering the impact of deleting indicators for better internal consistency reliability.

Convergent validity by utilizing the Average Variance Extractor (AVE) value in 0.376 - 0.778. Ideally, the AVE value should be greater than 0.50 to be convergently reliable. One latent variable has an AVE value of <0.50, namely the auditor’s quality of life (QWL) of 0.376. Fornell & Larcker (1981) stipulate considering the composite reliability value (CR) and the Cronbach Alpha (CA) value >0.60 to maintain as predictors (CR: QWL 0.807, WIPL 0.896, STRESS 0.933 and RAQP 0.863; CA: QWL 0.720, WIPL 0.853, STRESS 0.904, and RAQP 0.788). Hence, the interpretation convergent validity testing result of all indicators and the latent variables were stated to be met the statistical acceptance requirements.

Internal consistency reliability is supported by interpreting the Composite Reliability (CR) and Cronbach Alpha (CA). The composite reliability test results ranged in values between 0.807 and 0.933. Hence, all the latent variables' composite reliability test scores have met the acceptance requirements >0.70 (Hair et al., 2017; Sholihin & Ratmono, 2021). The Cronbach Alpha values were in the range of 0.720 to 0.904, and all latent research variables met the acceptance requirements between 0.60 and 0.90 (Hair et al., 2017).

Discriminant validity uses two determining indicators, cross-loading and the Fornell-Larcker criterion. Both tests resulted in the loading factor in the pair of indicators forming the latent variable greater than the loading factor formed between the same indicators and other latent variables (Sholihin & Ratmono, 2021). The Fornell-Larcker criterion compares the square root of the AVE value in a pair of latent variables greater

Table 3. Structural Model Testing

Model Fit and Quality Indices

|

No. |

Indices |

Result Value |

Reference (Kock, 2021) |

|

1 |

Average path coefficient |

0.209 at p-value <0.001 | |

|

2 |

Average R-squared |

0.178 at p-value <0.001 |

p-value |

|

3 |

Average adjusted R-squared |

0.172 at p-value <0.001 |

<0.05 |

|

4 |

Average block VIF |

1.113 |

≤5 or ideally ≤3.️300 |

|

5 |

Average full collinearity VIF |

1.214 |

≤5 or ideally ≤3.️300 |

|

6 |

Tenenhaus GoF |

0.327 (medium) |

small ≥0.️100; medium ≥0.️250; dan large ≥0.️360 |

|

7 |

Sympson’s paradox ratio |

1.000 |

Accepted if ≥0.️700 or |

|

Ideally 1.000 | |||

|

8 |

R-squared contribution ratio |

1.000 |

≥0.️900 or ideally 1.000 |

|

9 |

Statistical suppression ratio |

1.000 |

Accepted if ≥0.️700 |

|

10 |

Non-linear bivariate causality direction ratio |

1.000 |

Accepted if ≥0.️700 |

|

Source: Processed Data, 2022 | |||

than that of other pairs of latent variables (Hair et al., 2017). Both approaches conclude that the discriminant validity criteria are accepted.

Structural model testing aims to measure the research model quality. A good research model could produce an acceptable predictive model and might support a better and firm conclusion on the research hypothesis. Structural model testing has generally shown favourable indices. Statistical indices are shown in Table 3.

The inner model test result for the endogenous variable of auditor stress (STRESS) showed the R-square value of 0.25 from two exogenous predictors, namely Quality of Working Life (QWL) and Work Interference with Personal Life (WIPL). This score indicates that both exogenous models could predict approximately 25% of the construct variability phenomenon. The R-square value of the endogenous variable of Reduced Audit Quality Practice (RAQP) indicated by the predictor of stress (STRESS) is 0.104, explaining 10,4% of its predecessor of stress. The inner model test also shows that the most considerable effect on the model involves work interference with personal life (WIPL) toward stress (STRESS).

The conclusion of the hypothesis testing shows that four of the five hypotheses’ statements could be supported at an acceptable level of significance. The fifth hypothesis that WIPL has a positive effect on RAQP cannot be supported, and it indicates that there was possibly a significant indirect effect between those two variables via STRESS mediation. There is a partial STRESS mediation effect by influencing the paths of the auditor’s quality of working life and reduced audit quality practice (QWL ÷ RAQP).

The value of the indirect effect of QWL ÷ RAQP was not significant (β: -0.022; Sig. 0.072 or >0.05; Standard of Error (SE) 0.015; Effect Size (ES) 0.005; and Total Effect (TE) -0.022). While the indirect effect of WIPL ÷ RAQP is significant (e:0.062; Sig. 0.012 or <0.05; SE 0.027; ES 0.014; and TE 0.062. The statistical significance value of the indirect relationship between WIPL ÷ RAQP was in line with the direct relationship hypothesis testing of direct effect within WIPL ÷ RAQP (Hypothesis 5), which is also referring that the mediating effect of STRESS within this path was strong and significant. Considering the indirect relationship between QWL ÷ RAQP was not significant, it also strengthens

Table 4. Hypothesis Testing

|

Hypothese s |

Path/s |

Coefficient β |

Significance (Sig.) |

Hypotheses Testing*** | |

|

p-value |

t | ||||

|

H1 |

QWL÷ STRESS |

-0,158 |

*0,024 |

-1,983 |

Supported |

|

H2 |

WIPL ÷ STRESS |

+0,435 |

*<0,001 |

7,745 |

Supported |

|

H3 |

STRESS ÷ RAQP |

+0,141 |

*0,009 |

2,389 |

Supported |

|

H4 |

QWL ÷ RAQP |

-0,179 |

*0,007 |

-2,471 |

Supported |

|

H5 |

WIPL ÷ RAQP |

+0,131 |

**0,074 |

1,449 |

Not Supported |

* Significance within α 0.️05

** significance within α 0.️10

*** t-statistics on hypothesis testing by using critical t-ratios (one-tail) 1,645; within the

significance level of 95% (α 5%)

Source: Processed Data, 2022

the conclusion of the partial mediation relationship of STRESS on QWL ÷ RAQP relationship (QWL ÷ STRESS ÷ RAQP). There is a competitive partial mediation effect on the QWL ÷ RAQP because of the variability of direction between three pairs (1) QWL ÷ STRES (Neg.); (2) STRES ÷ RAQP (Pos.); and (3) QWL ÷ RAQP (Neg.).

Acceptance of the first hypothesis statement (QWL÷ STRESS) proves that auditors’ quality of working life impacts their resilience toward job stress. This statement is consistent with the theory and model explaining the stress phenomenon in the Job Demand-Resource (JD-R) theory. Job resources, which in this case are the quality of working life, reflect all work resources that support the resilience of auditors to answer the challenge of their work demands. The comprehensive side of the quality of working life includes adequacy of remuneration based on justice, work ethics, safety, security, and social integration. These conditions can then encourage the growth of skills and the potential of workers. This test’s results are consistent with the research by Salehi et al. (2020), which revealed a significant influence between the quality of work life and perceptions of psychological well-being on burnout which is also a complex form of job stress.

Work interference with personal life (WIPL) increased auditor stress via inevitable disturbance. This perception is measured by psychological perception of how auditors view their job in case of extra hours. All demands, which consequence their work-life balance, show the incidence of stress. This research, held during post-pandemic Covid-19,

Quality of Working Life (QWL)

β: -0.179 P< 0.01

7 Dimensions

β: -0.158

P: 0.02

β: +0.️435 P< 0.01

Stress

4 Indicators R-sq 0.25

β: +0.️141 P < 0.01

Reduced Audit Quality Practice (RAQP) 4 Indicators

R-sq 0.10

Work Interference with Personal Life (WIPL) 5 Indicators

β: +0.️131 P< 0.07

Figure 2. Hypothesis Testing Result

*) Dash shows the insignificant (unsupported hypothesis) relationship among variables.

Source: Processed Data, 2021

shows the alternative view of how the local government auditors view their dynamic job upon the challenge of online working hours in the pandemic era.

This research successfully interviewed an auditor at the regional inspectorate in Gianyar and Bangli while collecting the questionnaire packages; these interviews were followed by the “triangular” interviews with three senior auditors at BPKP Bali representative office (speciality in the regional inspectorate supervisory unit) to provide a better understanding on how general regional inspectorate management during the pandemic. In addition, BPKP Bali representative office maintained regular consulting and managerial troubleshooting in the context of APIP capability assessment. It provided technical assistance for the regional inspectorate in the Bali area. This additional information might provide a better understanding of the dynamics of supervisory regulation applied toward regional inspectorate during the Covid-19 Pandemic.

Qualitative interviews with research respondents provide a contextual explanation of this interference as a phenomenon related to the COVID-19 pandemic. The pandemic made most of the respondents’ interpersonal interaction patterns altered. One of the auditors stated explicitly that the pandemic indeed alters the audit mechanism: “Bali province actually enacted several regulations regarding the COVID-19 pandemic, the provincial government even issued social restrictions which indeed force us to alter our working hours, there was no other option instead that, even when we can do offline work it is only for preliminary coordination, all data collection concerning audit assignment managed online, send via WhatsApp and email”; while responding to the question about how to manage their working hours in specific, the respondent showed general technique was applied by mentioning, “just working online, via WhatsApp there was no specific technique applied, we meet in the office for the first coordination in order to split the tasks, and we proceed according to the WFH [working from home] schedule”.️

Concerning the flexible hours which might be applied and interfere with the auditor’s personal hours, the respondent’s reply could be inferred the possibility existed in a particular condition: “Supervisory assignments increased in the time of the pandemic, we should manage Covid-related assignments in a hurry. So, there is no other way. We communicate via WhatsApp, when needed, even at night, just text it”, stressing the possibility of work communication in personal auditor hours. Moreover, while responding to the statement of how the pandemic related to the general audit process among their peers, the respondent said: “some of the audit processes are shifted, especially regular audit assignment, audit assignment are allocated into the pandemic-related assignment, especially when the refocusing took place, Kemendagri ordered the budget refocusing and other supervisory assignments, it is increasing in general”.️

Restrictions on social interaction and changes in work systems – offline into online – have created difficulties in adaptation. In addition, the dynamics of online working systems affect unpredictable changes in working hours. This also created overlapping perceptions among respondents; they perceived that their “personal hours” might have been decreased by the flexible working hours.

Explicating auditor workload, the Ministry of Home Affairs issued regulations for disaster emergencies concerning Covid-19 for the local government in Indonesia (Kemendagri, 2020a, 2020b, 2020c, 2021). The regulation provides a unique mandate to APIP to review the procurement of goods/services in disaster emergencies. This new mandate is to be inferred to impact respondents’ perceptions of increasing pressure on

their work, primarily in the case of workload. Related to this inference was the mandate of local government supervisory unit to ensure pandemic-related supervisory assignment on economic stimulus toward people highly strained, assuring the public health system, and even supervisory assignment on regional food supply security (Akbar, 2022; Safrizal, 2022)

In addition to the quality of working life, qualitative interviews collected from the respondent also shows that working resource plays an essential role in their stance, e.g. the availability of financial support, remuneration, promotion, and safety. Citing auditor statement: “online work ideally support pulsa – air time/internet credit – and any other instrument needed for an online job, but ideally doesn’t mean compulsory especially when there was no such resource available from the office; because budget refocusing not only impact the supervisory budget but also decrease our monthly remuneration for several months”.️ The fascinating figure of this statement is the complication on budget refocusing, which is stated to impact auditors' remuneration; the statement also could be inferred as there was also a concern about the availability of job resources during the time of difficulties, including financial support, technical support systems, especially when the auditor should work remotely from their homes and the workload is perceived to increase.

Safety issues have been a big concern among auditors in the context of pandemic health issues, as common safety concerns. Auditors perceived the threatening condition of the pandemic as a real issue. They managed to adapt to the background condition, consistent with the auditor informant’s statement in regards to the casual question on how they perceived the pandemic in general: “of course, pandemic exist, that is why we do many things [inferred as various pandemic-related asignments], we do not travel, and we wore mask”, followed by their response on safety concern in the context of their job, respondent replied, “we do understand the risks, and we do it carefully, even when there was no available health safety protection support, e.g. APD [alat perlindungan diri/personal protective equipment], we do procure ourselves because we do have concern on our safety”.️ The interesting statement of self-procuring safety protection during the pandemic could be related to the complication of auditor job resources during the pandemic, which is problematic in the absence of adequate budgetary support, which is inevitable by the impact of refocusing policy.

Currently, the bonus system among civil servants in Indonesia does not relate to variable remuneration. As an example of contextual local government auditor, the remuneration system for the Bali provincial inspectorate office still entitled to the auditor position and daily presence, the other known factor to decrease the amount of remuneration entitled with disciplinary punishment, while the rewards to consider specific accomplishment or working merits still not mentioned in the regulation (Bali, 2020). Additionally, the respondent from the BPKP Bali representative office replied on how the inspectorate remuneration system, cited as: “The regular remuneration system applied within regional inspectorate in Bali, the same mechanism as an ordinary civil servant, there were the different amount of remuneration based on fiscal capability on each local government, so the amount varies, but there was no remuneration based on how well their supervisory result”.️

The bonus system known from respondent perception is fixed monthly with extra remuneration based on the auditors’ daily work presence percentage. This fact is

contextually different from the number of studies or research on variable remuneration. The classical perspective used in previous research, for example, the survey by Salehi et al. (2020), shows variable remuneration as one of the substantial factors in shaping the perception of the quality of working life. This notion is contextually opposed to the condition in Indonesia.

Another disclosure from the interview stated that their perception of the quality of working life is not exclusively tied to the variable income – in the form of performance bonuses or other variables – but alternatively relies on interpersonal support at the senior management level. This perception actually reflects the remuneration system applied within local government civil servants; the respondent explicated the reward system applied within the context of the fulfilment of criteria on the APIP capability model endorsed by Badan Pengawasan Keuangan dan Pembangunan (Indonesia’s Internal Control Agency), in which one of the criteria was related with non-financial rewards. The respondents stated “Thus, rewards are also one of the factors in APIP capability criteria, we also introduce such thing here, but the essential would be seniors support as they never leave us alone in the difficult time” while commenting on the effect of those rewards on interpersonal and quality of working life, the informant replied, “there were such financial rewards exist within the system, we do have tukin [tunjangan kinerja – literal translation as performance rewards], even though its decreases for several months, but rewards also help to motivate”.️

Noticing the impact of the budget refocusing during the pandemic while considering the statement from respondents: “we have our tukin unpaid for several months by refocusing policy" could be problematic in nature, as the subsequential impact of the background of pandemics, exhibit the pandemic strain among auditor as a form of job demand on elevated workload, flexible hours interference, and inadequate job resource support. Recapping these three items could be systemic and induce auditors’ occupational stress under the lens of JD-R theory.

In curious about how the various non-financial token of reward were applied within the regional inspectorate in the Bali area, the author interviewed the BPKP Bali Representative office, cited: “Currently, the rewards system is related with APIP capability criteria number two, the Key Process Area (KPA), in which each inspectorate should provide rewards policy to give appreciation to the auditors”, furthermore, while responding to the specific rewards might from within the context, the respondent replied: “most of them applies written piagam penghargaan [Certificate of Merit]. Kan, that is the most practical way to express gratitude”.️ While considering the form of such rewards might shed light upon alternative bonuses upon the perception of the auditors that the bonuses not only tied up with financial tokens but also interpersonal compliments and verbal attentions alternatively could also increase the quality of working life.

The influence or relationship between the disturbance and job stress is not mutually exclusive, considering the postulate of the job demand resource theory, which is always interrelated with the consequences of inadequate job resources relative to the job’s demand. Job resources are provided to any support system which enhances the capability of the auditor to do the job, e.g. technology infrastructure, tools and extra money and even additional time to manage their job. Within this context, the influential phenomenon concerning extra working hours reflected the increasing factor of job

demand. In contrast, auditor stress might reflect the inadequacy of job resources to tackle the job resource of extra hours.

Disturbance has an inevitable impact on unfavourable working conditions. It has the potential to create a variety of physical and psychological stress—the results of the direct relationship on the second hypothesis (WIPL ÷ STRESS) support this statement. Additionally, the fifth hypothesis (WIPL ÷ RAQP), which resulted in a non-significant effect between work interference and personal life toward reduced audit quality practice (RAQP), gives a better explanation of how job demand alone could not provide a reasonable predictor of dysfunctional behaviour. Conversely, quality of working life does.

Symptoms of physical and psychological fatigue characterize the phenomenon of stress. Stress occurs due to the perception of an unhealthy work environment. Stress may also arise simply from the auditor’s perception needs to meet the auditor’s expectations. Symptoms of stress have complex side effects on performance. The third hypothesis (STRESS ÷ RAQP) results in a significant positive impact on stress toward dysfunctional behaviour formation among auditors. Considering the risk and professional ethic of the auditor’s job, under any circumstances, the auditor should provide acceptable professional practice by conducting standard audit procedures. These findings show that stress in certain circumstances could also impact their professional practice, reducing audit quality.

Roskams and McNeely (2021) stated that the final impact of stress created a link between resources and Job demands that could affect workers’ performance. In understanding the auditing working environment, this study can prove the mediating impact of stress experienced by auditors on forming the antithesis of performance (RAQP). In addition, dysfunctional behaviour has a systemic effect on the quality of the audit results and the stakeholders (Widiastuty & Febrianto, 2010). The study of influence involving these two variables is also consistent with prior studies conducted by Asriningpuri & Gruben (2021), Elinda et al. (2019), Persiani & Tjiptohadi (2015).

Conclusion

This study’s general results explain the relationship between variables in the research hypotheses. In line with the theoretical basis/model, this research can also empirically prove the relationship between the quality of working life and the work interference with personal life in forming stress among auditors. The study also concluded that quality of working life is vital in tackling auditor stress and could prevent dysfunctional practices. This study also shows that even though the interference does not directly imply dysfunctional behaviour, the interference has strongly related to the incidence of auditor stress. The notion of the direct impact of work interference perceived as inevitable job demand in this research might become a novelty to the study of occupational stress.

These findings are related to the JD-R theory, under the perception of quality of working life as a job resource and work interference with personal life as an inevitable force contributing to job demand. This study may also add literature to the theoretical contribution of the Job-Demand Resources (JD-R) theory, especially in the context of local government internal auditors in Indonesia. This research also gives an alternative study to the plethora of occupational stress research based on the classical Conservation of Resource Theory.

APIP management needs to provide a better working environment for the audit institution. The takeaway from this research stated that the importance of pursuing a better working life impacts the auditor’s professionalism. The quality of the auditor’s working environment can be pursued by improving the auditor’s work culture through increasing transparency in career paths, time management, and personnel allocation under the proper workload analysis and promoting better employee justice.

Government agencies’ remuneration and performance bonus systems are diverse and tend to be flexible with the auditor’s performance appraisal system. APIP management should be able to look for other alternatives to improve the quality of the work environment by providing alternative performance bonuses based on non-financial tokens, e.g. better career promotion system or simple interpersonal verbal compliments. APIP management is expected to be able to create breakthroughs while maintaining compliance with applicable regulations. Fairness in promotions and career opportunities must also be considered in formulating APIP’s career management.

On the other hand, while maintaining the quality of working life is essential to create substantial job resources for the auditors, the management should also consider job demand factors. APIP management should control the extra-hours system for the auditor by providing scheduled and systematic job arrangements, appropriate workload analysis, and adequate resources in accordance with the needs of the audit assignment.

Regarding adaptability in difficult and unavoidable times, such as in the COVID-19 pandemic, several concerns should be considered. Management resilience in the face of uncertain conditions requires work management that can reduce the impact on auditor stress. It is undeniable that changes in work patterns during the pandemic can affect the interference in their personal space. Therefore, time arrangements through the online working system must be tightly considered to avoid interfering with the auditor’s personal life. This adaptability can also help to assist APIP’s management in creating resilience to crucial situations in the future.

APIP Management should also consider creating an early warning system to counter the reduced audit quality practice. An adequate quality control system could be developed by allowing better supervision, elevating employee competence, and allocating supervisory resources per the assignment’s needs. APIP’s management should focus more on the broader aspect of causality, by providing a deeper assessment of the diversity of perceptions that underlie this dysfunctional practice, including revisiting auditor stress and developing psychological assessment tools.

Regarding research methodology, the research concerning local government behavioural aspects is still under development in Indonesia, especially those that involve the two predictors (QWL and WIPL). The emergence of quality of working life and study on interference in personal space resembles the attention and concern toward civil servants’ well-being, which is still lacking in Indonesia, in the author’s humble opinion. Research instruments require more contextual adaptation and refinement, especially when adapted to the contexts and scopes of government sector auditing in Indonesia, particularly regarding the availability of instruments revealing the quality of working life and psychological well-being.

This study only revealed a simple relationship between the three predictor variables (namely quality of working life, work interference with personal life and auditors’ stress) and utilizing a restricted research subject within local government

auditor in the Bali area. The extensive model using more predictors and broader respondent numbers and profiles is more likely to form a more comprehensive result. Furthermore, the extensive model is also expected to increase the research model’s predictability.

The partial mediating effect of auditor stress can be better illustrated along with the extensive modelling of the job Demand-Resource/JD-R Theory in the extended version (Bakker & Demerouti, 2014b, 2017b; Bakker et al., 2001). Future research can also consider involving other variables to refine the test model, allowing exploration of the more extensive model to determine the reduced audit quality practice. These alternative variables include resilience, attachment to work, and job burnout. In addition, more extensive testing of the other construct, which is related to job performance and psychological well-being, might also help fill the gap in this study.

References

AAIPI, (2019). Peraturan Kepala Asosiasi Auditor Intern Auditor Pemerintah Indonesia (AAIPI) Nomor 85/AAIPI/PER/DN/2019 tentang Kerangka Praktik Profesional Pengawasan Intern Pemerintah.

AAIPI, (2021). Peraturan Asosiasi Auditor Intern Auditor Pemerintah Indonesia (AAIPI) Nomor: PER-01/AAIPI/DPN/2021 tentang Standar Audit Intern Pemerintah Indonesia.

Akbar, B. (2022). Tantangan Deseentralisasi pada Masa Pandemi. In A. F. Sampurna (Ed.), Kebijakan Pemerintah, Peluang, Tantangan, dan Kepemimpinan di Masa dan Pascapandemi COVID-19: Pandangan Pengambil Kebijakan di Tingkat Pusat dan Daerah (Vol. 2, pp. 130-148). Badan Pemeriksa Keuangan Republik Indonesia/Kompas Media Nusantara.

Amiruddin, A. (2019, 4 4). Mediating effect of work stress on the influence of time pressure, work–family conflict and role ambiguity on audit quality reduction behavior [computer-program]. International Journal of Law and Management, 61(2), 434-454. https://doi.org/https://doi.org/10.1108/IJLMA-09-2017-0223

Anugerah, R.️, Anita, R.️, & Sari…, R.️ N.️ (2016).️ The analysis of reduced audit quality behavior: The intervening role of turnover intention. International Journal of Economics and Management, 10 (S2): 341 – 353 (2016).

Asriningpuri, G. P., & Gruben, F. (2021). The Effect of Time Budget Pressure and Dysfunctional Auditor Behavior on Audit Quality: A Case Study in an Audit Firm in Indonesia. Diponegoro Journal of Accounting.

Astrachan, C. B., Patel, V. K., & Wanzenried, G. (2014). A comparative study of CB-SEM and PLS-SEM for theory development in family firm research. Journal of Family Business Strategy, Volume 5, Issue 1, March 2014, Pages 116-128, 116-128. https://doi.org/https://doi.org/10.1016/j.jfbs.2013.12.002

Bakker, A.️ B.️, & Demerouti, E.️ (2007).️ The Job Demands‐Resources model: state of the art. Journal of Managerial Psychology, 22(3), 309-328.

https://doi.org/https://10.1108/02683940710733115

Bakker, A. B., & Demerouti, E. (2014a). Job demands and resources theory. In P. Y. Chen & C. L. Cooper (Eds.), Work and Well-being: Well-being: A Complete Reference Guide Volume III (Vol. Volume III, pp. 37-64). John Wiley & Sons, Ltd. Published 2014 by John Wiley & Sons, Inc.

Bakker, A. B., & Demerouti, E. (2014b). Job demands & resources theory. In Work and Well-being: Well-being: A Complete Reference Guide (Vol. Volume III). John Wiley & Sons, Ltd. Published 2014 by John Wiley & Sons, Inc.

Bakker, A. B., & Demerouti, E. (2017a). Job demands and resources theory: Taking stock and looking forward. Journal of Occupational Health Psychology, 22(3), 273–285. https://doi.org/https://doi.org/10.1037/ocp0000056

Bakker, A. B., & Demerouti, E. (2017b). Job demandsâresources theory: Taking stock and looking forward. Journal of Occupational Health Psychology, 22(3), 273–285. https://doi.org/https://doi.org/10.1037/ocp0000056

Bakker, A. B., Nachreiner, F., & Schaufeli, W. B. (2001). The job demands-resources model of burnout. Journal of Applied Psychology, Vol 86(3), Jun 2001, 499-512. https://psycnet.apa.org/journals/apl/86/3/499.html?uid=2001-06715-012

Peraturan Gubernur Bali tentang Perubahan Ketiga atas Peraturan Gubernur Nomor 125 Tahun 2016 Tentang Tambahan Penghasilan Pegawai, (2020).

Benitez, J., Henseler, J., Castillo, A., & Schuberth, F. (2020). How to perform and report an impactful analysis using partial least squares: Guidelines for confirmatory and explanatory IS research. Information & Management, Volume 57( Issue 2), 116 -128. https://doi.org/https://doi.org/10.1016/j.im.2019.05.003

BPKP, (2015). Pedoman Teknis Penilaian Mandiri Kapabilitas APIP.

BPKP, (2021). Laporan Kinerja Badan Pengawasan Keuangan dan Pembangunan Tahun 2021.

Coram, P., Ng, J., & Woodliff, D. (2003). A survey of time budget pressure and reduced audit quality among Australian auditors. Australian Accounting Review, Volume 13(Issue 29). https://doi.org/https://doi.org/10.1111/j.1835-2561.2003.tb00218.x

Creswell, J. W., & Clark, V. L. P. (2017). Designing and conducting mixed methods research . Sage Publishing House.

Donnelly, D. P., & Quirin, J. J. (2003). Auditor acceptance of dysfunctional audit behavior: An explanatory model using auditors’ personal characteristics. Behavioral Research in Accounting (2003), 15 (1)((1)), 87-110.

https://meridian.allenpress.com/bria/article-abstract/15/1/87/67066

Elinda, A. I., Iswati, S., & Setiawan, P. (2019). Analysis of the influence of role stress on reduced audit quality. Jurnal Akuntansi Universitas Tarumanegara(2), 301-315. https://doi.org/https://doi.org/10.24912/ja.v23i2.593

Fisher, G. G., Bulger, C. A., & Smith, C. S. (2009, Oct). Beyond work and family: a measure of work/nonwork interference and enhancement. Jurnal Occupational Health Psychology, 14(4), 441-456. https://doi.org/https://10.1037/a0016737

Fogarty, T. J., & Kalbers, L. P. (2006). Internal auditor burnout: An examination of behavioral consequences. Advances in Accounting Behavioral Research (Advances in Accounting Behavioural Research, Vol. 9, 51-86.

https://doi.org/https://doi.org/10.1016/S1475-1488(06)09003-X

Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of marketing research, 18(1), 39 - 50. https://doi.org/https://doi.org/10.1177/002224378101800104

Gim, G. C. W., & Ramayah, T. (2020). Predicting turnover intention among auditors: is WIPL a mediator?. The Service Industries Journal, Vol.40(9-10), 726 - 752. https://doi.org/https://doi.org/10.1080/02642069.2019.1606214

Hair, J. F., Sarstedt, M., Ringle, C. M., & Gudergan, S. P. (2017). Advanced issues in partial least squares structural equation modeling . Sage Publishing House.

Peraturan Pemerintah Republik Indonesia Nomor 60 tahun 2008 tentang Sistem Pengendalian Intern Pemerintah, (2008).

Instruksi Menteri Dalam Negeri Nomor 1 Tahun 2020 tentang Pencegahan Penyebaran dan Percepatan Penanganan Corona Virus Disease 2019 di Lingkungan Pemerintah Daerah, (2020a).

Keputusan Menteri Dalam Negeri Nomor 119/2813/SJ Tahun 2020 tentang Keputusan Bersama Menteri Dalam Negeri dan Menteri Keuangan tentang Percepatan Penyesuaian Anggaran Pendapatan dan Belanja Daerah Tahun 2020 dalam Rangka Penanganan Corona Virus Disease 2019 (Covid-19), serta Pengamanan Daya Beli Masyarakat dan Perekonomian Nasional, (2020b).

Surat Edaran Irjen Kementerian Dalam Negeri Nomor 700/1101/IJ tanggal 29 Mei 2020 tentang Pengawasan Penyaluran Bantuan Sosial untuk Penanganan COVID-19, (2020c).

Instruksi Menteri Dalam Negeri Nomor 21 Tahun 2021 tentang Penyediaan dan Percepatan Penyaluran Bantuan Sosial dan/atau Jaring Pengaman Sosial yang Bersumber dari Anggaran Pendapatan dan Belanja Daerah, (2021).

Kock, N. (2021). WarpPLS user manual: Version 7.0 . WARP PLS Official Website (https://scriptwarp.com/warppls/).

Narehan, H.️, Hairunnisa, M.️, & Norfadzillah…, R.️ A.️ (2014).️ The effect of quality of work life (QWL) programs on quality of life (QOL) among employees at multinational companies in Malaysia. Procedia - Social and Behavioral Sciences, Vol. 112, 2432. https://doi.org/https://doi.org/10.1016/j.sbspro.2014.01.1136

Paino, H., Ismail, Z., & Smith, M. (2010). Dysfunctional audit behaviour: an exploratory study in Malaysia. Asian Review of Accounting, Vol.18(2), 162-173. https://doi.org/https://doi.org/10.1108/13217341011059417

Persiani, A.️, & Tjiptohadi…, T.️ (2015).️ The Association of Time Budget Pressure and Reduced Audit Quality (RAQ) Behavior (Study among Indonesian Auditors). The Indonesian Journal of Accounting, Vol.18(3).

https://doi.org/http://doi.org/10.33312/ijar.386

Prijanka, M., Trisdiarto, T., & Abdullah, E. H. (2021). The Covid-19 Pandemic: Impacts on Hotel Workers’ Job Stress, Well-Being and Self-Assessed Mental Health at the Nusa Dua Bali. Budapest International Research and Critics Institute (BIRCI-Journal): Humanities and Social Sciences, 4(4), 13431 - 13444.

https://doi.org/https://doi.org/10.33258/birci.v4i4.3423

Roskams, M.️, & McNeely…, E.️ (2021).️ Job Demands-Resources Model: Its applicability to the workplace environment and human flourishing. In V. D. Rianne Appel-Moelenbroek (Ed.), A Handbook of Theories on Designing Between People and the Office Environment (pp. 27-38). Routledge.

https://doi.org/https://doi.org/10.1201/9781003128830

Sabonete, S. A., Lopes, H. S. C., Rosado, D. P., & Reis, J. C. G. (2021). Quality of work life according to Walton’s model: Case study of the higher institute of defense

studies of Mozambique. Social Science (MDPI), 10, 244. https://doi.org/https://doi.org/10.3390/socsci10070244

Safrizal, Z. A. (2022). Perkembangan Kasus dan Respons Pemerintah dalam Penanganan Covid-19. In A. F. Sampurna (Ed.), Kebijakan Pemerintah, Peluang, Tantangan, dan Kepemimpinan di Masa dan Pascapandemi COVID-19: Pandangan Pengambil Kebijakan di Tingkat Pusat dan Daerah (Vol. 2, pp. 130-148). Badan Pemeriksa Keuangan Republik Indonesia/Kompas Media Nusantara.

Salehi, M., Seyyed, F., & Farhangdoust, S. (2020). The impact of personal characteristics, quality of working life and psychological well-being on job burnout among Iranian external auditors. International Journal of Organization Theory & Behavior, Vol.23, 189-205. https://doi.org/https://doi.org/10.1108/IJOTB-09-2018-0104

Serey, T. T. (2006). Choosing a robust quality of work life. Business Forum, Vol. 27(2).

Sholihin, M., & Ratmono, D. (2021). Analisis SEM-PLS dengan WarpPLS 7.0 untuk hubungan nonlinier dalam penelitian sosial dan bisnis . Penerbit Andi.

Smith, K. J., & Emerson, D. J. (2017). An analysis of the relation between resilience and reduced audit quality within the role stress paradigm. Advances in Accounting, Vol.37, 1-14. https://doi.org/https://doi.org/10.1016/j.adiac.2017.04.003

Smith, K.️ J.️, Emerson, D.️ J.️, & Boster…, C.️ R.️ (2020).️ Resilience as a coping strategy for reducing auditor turnover intentions. Accounting Research Journal, Vol.33, 483498. https://doi.org/https://doi.org/10.1108/ARJ-09-2019-0177

Smith, K. J., Emerson, D. J., & Everly, G. S. (2017). Stress arousal and burnout as mediators of role stress in public accounting. Advances in Accounting Behavioural Research, Vol.20, 79-116.

https://doi.org/https://doi.org/10.1108/S1475-148820170000020004

Subadra, I. N., & Hughes, H. (2022). Pandemic in paradise: Tourism pauses in Bali. Tourism and Hospitality Research, 22(1), 122-128.

https://doi.org/https://10.1177/14673584211018493

Widiastuty, E., & Febrianto, R. (2010). Pengukuran kualitas audit: sebuah esai. Jurnal Ilmiah Akuntansi dan Bisnis, Vol.5(2).

https://ojs.unud.ac.id/index.php/jiab/article/download/2621/1833

Yuniti, I., Sasmita, N., Komara, L. L., Purba, J. H., & Pandawani, N. P. (2020). The impact of covid-19 on community life in the province of Bali, Indonesia. International Journal of Psychosocial Rehabilitation, 24(10), 1918-1929.

Acknowledgement:

We would like to express special gratitude toward The Indonesia Endowment Fund for Education (LPDP) for research funding. The special appreciation also goes to all respondents in the regional inspectorate in Bali.

|

Appendix Appendix 1. The Quality of Working Life (QWL) | ||

|

No. |

Dimension of Measurements |

Indicators |

|

1 |

Safety and health in working conditions |

1) Work brings you worries and annoyances QWL 1.1. Rasa khawatir dan cemas yang diakibatkan oleh pekerjaan Anda |

|

Kondisi keamanan dan kesehatan kehidupan kerja |

2) How your superior make considerations and QWL 1.2 observations about your work and productivity cause you humiliation or other inconvenience in the face of co‐workers.️ Cara atasan Anda dalam menilai atau mengawasi Anda dalam hal pekerjaan membuat Anda merasa direndahkan atau perasaan tidak nyaman di depan kawan kerja yang lain. | |

|

2 |

Constitutionalism |

superiors Anda dapat mengekspresikan pendapat kepada atasan

employees, regardless of sex, age, or occupation, is equal and without prejudice Dalam persepsi Anda perlakuan antara sesama auditor bersifat setara tanpa membeda-bedakan |

|

3 |

Fair and adequate compensation Kompensasi yang adil dan memadai |

You consider your salary to be adequate compared QWL 3 to your contribution to the institution Kompensasi yang Anda dapatkan (gaji dan tunjangan) sesuai dengan kontribusi Anda dalam bekerja |

|

4 |

Career opportunities and job security Kesempatan dan Peluang Karier |

compared to

Terdapat mekanisme promosi berdasarkan kompetensi dan kinerja

offers of scholarships to continue your studies or to take complementary or specialization courses Terdapat kesempatan pengembangan pendidikan dalam bentuk beasiswa dan lainnya |

|

5 |

Opportunity to use and develop human capabilities |

You need to receive authorisation from your QWL 5 superior to decide what and how to do your job Anda memerlukan otorisasi atau persetujuan khusus dari atasan Anda terkait dengan apa dan bagaimana tugas yang Anda laksanakan |

|

Dimension of No. Measurements |

Indicators |

Kesempatan

Pengembangan Kapabilitas Pegawai

|

6 Social relevance of work life Relevansi Sosial |

Institusi tepat Anda bekerja sekarang dikenal dan memiliki reputasi yang memadai

|

|

7 Social integration in the organization Integrasi Sosial dalam Organisasi |

(Auditor and Non-Auditors) Terdapat perbedaan perlakuan antara pegawai auditor dan non auditor

Pendapat Anda dipertimbangkan dalam konteks permasalahan atau hal lain yang melibatkan pegawai auditor dan non auditor |

Source: Contextual adaptation from Sabonete et al. (2021) using a 4-scale Lickert scale varying from strongly disagree to agree strongly.

Appendix 2. Work Interference with Personal Life (WIPL), Stress (STRESS) and Reduced Audit Quality Practice (RAQP)

|

No. Variables/Constructs**) |

Indicators*) |

|

2 WIPL 4-scale Lickert scale (strongly disagree to agree strongly) |

1 I come home from work too tired to WIPL 1 do things I want. (WIPL 1) Saya merasa sangat lelah ketika saya pulang dari bekerja dan saya terlalu lelah untuk mengerjakan yang lainnya 2 My job makes it difficult to maintain WIPL 2 the kind of personal life I would like (WIPL 2) Pekerjaan saya menggagu hubungan personal saya 3 I often neglect my personal needs WIPL 3 because of the demands of my work. (WIPL 3) Saya kerap kali mengabaikan kehidupan personal saya akibat tuntutan pekerjaan saya 4 My personal life suffers because of WIPL 4 my work (WIPL 4) Kehidupan pribadi saya ‘menderita’ akibat dari pekerjaan saya 5 I have to miss out on important WIPL 5 personal activities due to work time. (WIPL 5) Saya melewatkan aktivitas sosial yang penting disebabkan waktu saya digunakan untuk pekerjaan saya |

|

3 STRESS 4-scale Lickert (Seldom/never to almost always) |

1 Anticipating or remembering STRESS 1 upsetting things? Memikirkan atau mengingat hal yang tidak nyaman atau membuat marah 2 I was thinking about things which STRESS 2 upset you? Berpikiran tentang sesuatu yang mengganggu/tidak nyaman 3 Are you concerned or worried? STRESS 3 Khawatir dan mencemaskan sesuatu 4 Are you repeating unpleasant STRESS 4 thoughts? Pemikiran atas ketidaknyamanan yang berulang |

|

4 RAQP |

1 Failed to research an accounting RAQP 1 principle*** |

|

No. Variables/Constructs**) |

Indicators*) |

|

4-scale Lickert (Seldom/never to almost always) |

Anda tidak berhasil menentukan permasalahan audit secara pasti terutama dalam hal pelanggaran apa yang sebenarnya dilakukan oleh auditan |

|

2 |

Made superficial reviews of RAQP 2 documents*** Anda membuat reviu yang tidak berdasarkan bukti yang memadai (REKOCUMA: Relevan, Kompeten, Cukup, dan Material) |

|

3 |

Prematurely signed-off on an audit RAQP 3 step*** Melewatkan prosedur audit yang seharusnya dilaksanakan |

|

4 |

Reduced work below what you RAQP 4 considered reasonable*** Mengurangi pekerjaan tertentu yang menurut Anda seharusnya dilakukan |

*) The research originally used indicator of measurements using Bahasa Indonesia (shown in italics); **) WIPL are contextually adopted from Gim and Ramayah (2020), STRESS and RAQP from Smith and Emerson (2017); ***) Contextual translation within Indonesia’s local government terms and audit procedures.

Jurnal Ilmiah Akuntansi dan Bisnis, 2023 | 114

Discussion and feedback