The Effects of Perceived Risks and Perceived Values on Online Purchase Intention: Evidence from Young Consumers in Indonesia

on

pISSN : 2301 – 8968

JEKT ♦ 15 [1] : 241-270

eISSN : 2303 – 0186

The Effects of Perceived Risks and Perceived Values on Online Purchase Intention: Evidence from Young Consumers in Indonesia

Aurelia Sheryl Margono, Nindy Sasabela Perwitasari, Matthew Alexander Nathaniel, Navratilova Ivita Silalahi, Istijanto Istijanto

ABSTRACT

COVID-19 pandemic has given a significant impact to both businesses and consumer behaviours. Not only businesses that have to adapt, consumers from all around the world have changed their behaviours in shopping and fulfilling their needs through online. This study aims to examine the effects of perceive risks and perceived values of young consumers on their intention to purchase online electronic products in Indonesia. The convenient sampling was employed with 314 respondents participating in the current research. Then, this study carried out a quantitative analysis by using statistical methods. Exploratory factor analysis was adopted to confirm the validity of the measuring items. Multiple regression analysis was employed to test the influence of perceived risks and perceived values on online purchase intention. The findings show that product risk and security risk have a significant negative effect on consumers' intention to purchase online products, while the escapism motive and value motive have a significant positive effect on the intention to purchase online products.

Keywords: perceived risk, perceived value, online purchase intention, online shopping, young consumers

JEL Classification: C83, E71, L81, M31

INTRODUCTION

The development of technology and the internet are continuously experiencing significant growth every year. Up to this day, the growth of internet users has reached 1,331.9% greater than in 2020 (Internet World Stats, 2021). The

COVID-19 pandemic which started in 2020 has been pushing a digital transformation in various aspects. The new health protocols such as physical and social distancing have impacted many businesses such as shopping malls, restaurants, and also traditional

markets (Chetty et al., 2020). Consequently, those who are impacted must adopt and learn the digital world in order to shift their business towards online business. Therefore, such a phenomenon is supporting the growth of e-commerce even more (Lavuri, 2021).

According to Donthu and Gustafsson (2020), the COVID-19 pandemic has given a significant impact to both businesses and consumer behaviours. Not only businesses that have to adapt, consumers from all around the world have changed their behaviour in shopping and fulfilling their needs through online (Bartik et al., 2020). The digitalization has created a new consumption pattern and shopping behaviour which give more challenges toward businesses in facing the new consumer behaviours (Santo and Marques, 2021).

Consumers from various generations are affected and possess a new behaviour of online shopping, which is dominated by the young generation such as Gen-Y (millennial) and Gen-Z.

The Gen-Y as a group of consumers who were born in 1981 until 1996, are the biggest internet users and online shoppers in Indonesia. According to the National Socio-Economic Survey (Susenas) in 2019, there are 47 million Gen-Y groups who use the internet and 17% (7.8 million) among them love to shop online in the form of products and services. Additionally, the pandemic caused digitalization to progress rapidly and foster the Gen-Z as one of the most important consumer segments that marketers want to capture, reminding that this generation is called as digital natives’ generation (Ng et al., 2019).

Gen-Z is the group of consumers who were born in 1997 until 2012, and are predicted to be one of the biggest online consumer segments (Meola, 2021). Even though this generation is not yet dominating the market, Gen-Z is considered as the core influencers who influence the shopping activities of Gen-Y and Gen-X generations (Finneman, 2020). Therefore, this research will be aimed towards the young consumers of

Gen-Z and Gen-Y with the age ranging from 15 years old to 35 years.

Many types of products are sold online, and for this research will focus on electronic products. A research result from MarkPlus found that electronic product sales increased during COVID-19 pandemic in Indonesia. From 500 respondents in MarkPlus research, they said 26% of respondents bought electronic products via online, and those products were microwave, blender, and mixer. The General Manager of Home Appliances Polytron, Albert Fleming (JPNN.com, 2021) stated that the sales of Polytron products in the pandemic era were dominated through online rather than traditional retail stores.

There are several challenges that become the main problems of online consumers such as transaction securities, data privacy, validity of electronic contract, inadequate information, product quality and rights enforcement (Paynter dan Lim, 2001). Lee and Tan (2003) shows that consumers tend to feel a higher risk when they shop online compared to buy

at traditional retail stores. These perceived risks are essentials as they indirectly affect consumers’ attitude and purchase intention (Ariff et al., 2014). The perceived risks toward online shopping have a negative impact on consumers’ intention to purchase (Almoussa, 2012).

On the other hand, according to Hill et al. (2013) online shopping can give tremendous benefits such as finding the best alternatives and providing the young generation with new activities after a long day routine. The perceived values gained by those consumers have a positive impact towards online purchase intention. Consumers will gain material value from online shopping when they could get the same benefit or quality with a lower price. This kind of material value will form a purchase intention (Santo and Marques, 2021). Emotional value can be in a form of pleasure and satisfaction from the experience of shopping online. Consumers do not just shop to get the products they want but also to fulfill their needs for experience and emotion,

satisfy the utilitarian and hedonic needs (Santo and Marques, 2021).

There is still limited research that integrated two variables of perceived risk and perceived value towards online purchase intention. The former research conducted by Kamalul Ariffin et al. (2018) stated that the relation between perceived risk and intention to purchase online products are still inconclusive. Moreover, there are still few studies that examine online purchase intention during the COVID-19 pandemic with samples in Indonesia. Therefore, the current research attempts to fill this research gap by investigating the influence of perceived risks and perceived values of young consumers on online purchase intention in Indonesia. The results can later be used as insights for business players in designing better strategies that can attract young consumers to make online purchases.

LITERATURE REVIEW AND HYPOTHESES

Online Purchase Intention

Purchase intention is often used as a measuring tool to predict the actual buying activity of consumers. According to Mirabi et al. (2015), purchase intention is the urge to buy a product in a particular buying environment. Consumer purchase intention is essential in predicting consumer behavior clearly, depending on the factors that influence the measurement under various conditions (Kamalul Ariffin et al., 2018). Based on research from Ahmed, Samad, and Khan (2021), it was found that benefits, shopping orientation, and consumer satisfaction have a positive effect on purchase intention, while perceived risk has a significant negative effect.

Since the advent of e-commerce, the third most popular online activity after sending email and web surfing was online shopping (Jamali et al., 2014). Online purchase intentions in a webshopping environment will drive strongly consumers to buy products online (Salisbury, et al., 2001). Online purchase intentions also represent consumer desires and intentions for a

product to be purchased at a certain time period or a certain situation through an online transaction platform (Cheong et al., 2020). According to Pavlou (2003), online purchase intention is seen from the extent to which consumers are willing to purchase a product online.

Li and Zhang (2002) defined online purchase intentions as consumers' willingness to buy products or services via the internet. Masoud (2013) reveals that product risk, financial risk, security risk, and time risk will negatively affect online purchase intentions. In the future, online purchase intentions will increase if the level of perceived risk by consumers is low. Based on previous research, this study will use product risk, financial risk, security risk, time risk, and social risk as perceived risk variables that influence online purchase intentions.

Online purchase intention is also significantly influenced by perceived value, where there is a positive relationship between perceived value and purchase intention (Chen, 2012). In

line with the research carried out by Dharmesti et al. (2021), escapism motive and value motive have positive effects on online purchase intention among young consumers in Australia and the United States. Young consumers are classified as bargain hunters (Phau and Woo, 2008), realizing the power of online shopping as a way to find the best value among many options (Hill et al., 2013). Based on previous research, this study will use escapism motive and value motive as perceived value variables that influence online purchase intentions.

Perceived Risk

Perceived risk is one of the critical factors influencing online purchasing decisions. An analysis of the factors of perceived risk in online shopping is a step that must be taken to determine the content and influence of risk on consumers (Masoud, 2013). Chang (2008) sees that the effect of online interactions is the main obstacle in online shopping. In general, active online shopping behaviour will have an

impact on the success of e-commerce transactions (Safie et al., 2019).

In an online shopping environment, consumers' perceived risk is more significant due to limited access to see the product physically or meet directly with the seller of the product (Schiffman and Kanuk, 2007). Lee and Tan (2003) stated that customers who have a high-risk perception are unlikely to purchase products online. This is supported by Kim and Lennon (2013) that stated the greater the perceived risks with online shopping, the weaker the consumers’ purchase intention.

Financial Risk

Financial risk is one of the main types of customers’ risks when consumers shop online (Sinha & Singh, 2017). Financial risk also acts as a strong predictor in influencing online purchase intention (Bhatti et al., 2020). This happens as financial risk could cause a threat that leads to a negative perspective and consequently affect consumer behaviour (Barnes, Bauer et al., 2007). According to Pavlou (2003), shopping online has a bigger potential of loss, especially when

the product could not function very well or not worth the price. The former research conducted in India and Pakistan found that financial risk has a significant negative influence on online purchase intention (Bhukya and Singh, 2015; Haider dan Nasir, 2015). Based on the previous studies, H1 is proposed as:

H1: Financial risk has a significant negative influence on online purchase intention.

Product Risk

Product risk happens when the purchased product gets broken or has no function as how consumers expected it to be (Kim et al., 2008). The failure of a product in meeting consumers’ standards often occurs in online shopping as consumers have limited information about the products and could not see the real form of product before buying (Popli & Mishra, 2015). Product information can be limited as consumers can only rely on information provided by online sellers (Kamalul Ariffin et al., 2018). The previous studies have stated that product risk has a negative influence towards online

purchase intention (Han dan Kim, 2017; Kamalul Ariffin et al., 2018). Based on these findings, H2 is proposed as:

H2: Product risk has a significant negative influence on online purchase intention.

Security Risk

Security risk arises due to online fraud or hacking, which exposes the security of online transactions as a potential loss (Soltanpanah et al., 2012). Moreover, Kayworth and Whitten (2010) stated that customers tend to avoid websites that require personal data for the sign up, which causes the consumers to provide fake or incomplete data. This case happens because consumers are concerned in giving their shipment address and credit card information, or settle their transaction online (Leeraphong dan Mardjo, 2013). Tran (2020) also explained that consumers are mostly afraid that their credit card information will be exploited or abused. Moreover, if there is no information about the secure mechanism of online shopping, the online purchase intention

will decrease (Masoud, 2013). For that reason, H3 is proposed as:

H3: Security risk has a significant negative influence on online purchase intention.

Time Risk

Time risks include time and effort in the process of returning or exchanging products, technology problems such as slow websites, delivery times, and waiting time for products (Almousa, 2011). Time, convenience, or effort may be discarded if the purchased product is repaired or exchanged (Hanjun et al., 2004). Sometimes, consumers can also leave online sites without buying any products because they do not get the products they are looking for or have problems opening the online shopping sites (Popli and Mishra, 2015). The time spent by consumers in searching for information on unfamiliar products will reduce consumers' purchase intentions to buy online (Kamalul Ariffin et al., 2018). Time risk is one factor that influences consumer online purchase intention (Ye, 2004). Seeing this, H4 is formed:

H4: Time risk has a significant negative influence on online purchase intention.

Social Risk

Social risk is one of the crucial elements in perceived risk because it interprets the influence of people around in purchasing decisions (Kamalul Ariffin et al., 2018). This is because social risk refers to the perceived assessment of the product or service purchased to create displeasure among families, friends, or the community (Dowling & Staelin, 1994). Everyone has the possibility to be influenced by their partner and by their group or community through their concerns about people's assessment of the costs and benefits of the product or service, how the product or service affects other people, or about how the product maintains a positive selfidentity (Woods & Hayes, 2012). On the other hand, Gen Y and Gen Z consumers pay attention to the perception of the assessment given by their friends, family, and followers on social media (Goldring & Azab, 2020). So if these concerns have an impact on

negative judgments, people will change their interpretation of the risk of a product after receiving confirmation of their group's assessment of the amount of risk that must be borne (Beuhler & Griffin, 1993). Seeing this, H5 is formed:

H5: Social risk has a significant negative influence on online purchase intention.

Psychological Risk

Psychological risk reflects consumers’ disappointment towards themselves due to bad product choice or bad service (Ueltschy et al., 2004). Psychological risk is also defined as the possibility where a certain type of product does not correspond to consumer’s desired selfimage (Littler & Melanthiou, 2006). Psychological risk is often felt by the consumers when the products they receive are different from what they expected, hence creating the feelings of discomfort, expectation and its actual form could trigger mental pressure in the next online purchase due to worry of uncertainty (Kamalul Ariffin et al., 2018). According to Mitchell (1998), even though the received product could

function very well and as expected, other people’s expectation and judgement could give an inferior impression towards the product. Therefore, psychological risk is one of the main dimensions that deter online purchase intention. Based on this discussion, H6 is developed:

H6: Psychological risk has a significant negative influence on online purchase intention.

Perceived Value

Perceived value in online shopping has impact towards consumer behaviour and shopping intention (Ahn et al., 2007). In the midst of the digital era where most shopping activity is often occurring via online, Gen-Y and Gen-Z are the generations who are tech savvy, optimistic, and engaged through online (Goldring & Azab, 2020). Therefore, young consumers are aware with the power of online shopping in helping them to find the best value among many product alternatives (Ahn et al., 2007). Meanwhile, the level of excitement from Gen-Y and Gen-Z to be engaged in the online world could be seen as a form of

escaping from their daily mundane activities or called as escapism motive (Hill et al, 2013). As a result, this research proposed value motive and escapism motive as the factors of perceived value that positively influence online purchase intention.

Escapism Motive

Escapism motive in online context could be defined as the level of an individual's longingness in using the internet with the intention to escape himself from the daily mundane activities (Hill et al., 2013). This refers to consumers’ positive desire to get rid of boredom induced by daily activities that are monotonously structured (Goldring & Azab, 2020). Not only to avoid boredom, the distress that is faced in the real world also makes consumers escape through online. This online escapism can be in the form of communication, social networking, information search, and online shopping (McLean et al., 2021; Stocchi et al., 2020). Based on this discussion, H7 is developed:

H7: Escapism motive has a significant positive influence on online purchase intention.

Value Motive

Value motive has close relations to price, cost, and benefits from the exchange of a particular transaction (Jackson et al., 2011). The research conducted by Zeithaml (1988) also reports that price could give an extrinsic signal regarding a product’s quality, especially for unfamiliar brands. Such perceived quality will give consumers a glimpse of illustration regarding the benefit and value they will gain from purchasing the product.

On the other hand, consumers sometimes wish to gain value from the experience of online shopping which is beyond the functional purpose and beyond task orientation (Bloch et al., 1986), and wish that shopping could give a satisfying and enjoyable experience (Holbrook & Corfman, 1985). Henceforth, shopping satisfaction is not only obtained when the product is economical, but also obtained from the shopping experience felt by the

consumers (Ahn et al., 2007). It is important for Gen Y to take advantage of the moment that is lived by the day in the best possible way, thus such point of view influences Gen-Y’s expectation of shopping where they tend to find the benefits as much as possible with least sacrifice (Dharmesti et al., 2021). Therefore, the following hypothesis is posited:

H8: Value motive has a significant positive influence on online purchase intention.

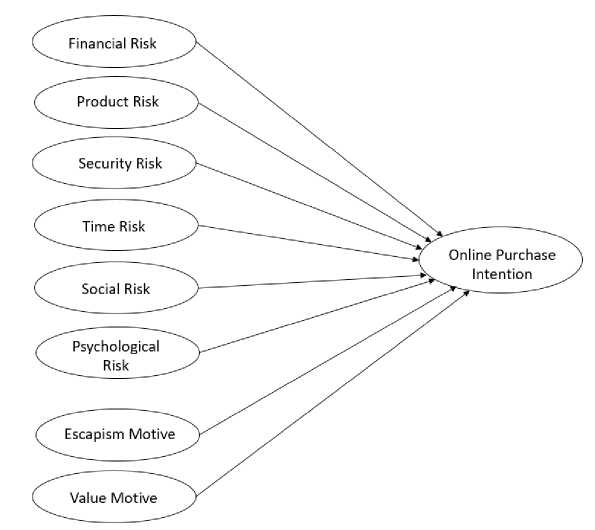

Research Model

The conceptual model used in this research is built from two former studies (Kamalul Ariffin et al., 2018; Dharmesti et al., 2021) which examined the factors that influence online purchase intention. Kamalul Ariffin et al. (2018) tested perceived risk variables that consist of financial risk, product risk, security risk, time risk, psychological risk, and social risk as the determinant factors in online purchase intention. Those perceived risks have negative influence towards consumers’ online purchase intention where the

higher the perceived risk, the lower the online purchase intention becomes. Additionally, this research also combines the examination towards perceived value or motivation as the determinant factor in online purchase intention. Adopting from the research of

Dharmesti et al. (2021), this research examined the variables of escapism motive and value motive which are hypothesized to have positive effects on online purchase intention. The conceptual model for this research is shown in Figure 1.

Figure 1: Theoretical Framework

Source: Authors’ own elaboration

METHODOLOGY

Research design

Primary data collection for this study was conducted using an online questionnaire created with the web

application service, Google Forms. The sampling method was convenience sampling. With this method, respondents who are willing to take the time to fill out questionnaires are found and the data of those who have

purchased electronic products online are used for further data analysis. The amount of data from valid respondents that could be used is 314 data.

Instrument

The questionnaire used to measure a total of eight independent variables and one dependent variable contains a total of 38 measurement items (Table 1). The measurement items were adopted from the former research, which is 6 perceived risk variables adapted from Kamalul Ariffin et al. (2018). Whereas two variables perceived value and one variable online purchase intention were adapted from Dharmesti et al. (2021). All items were measured using a 7-point Likert (1=strongly disagree to 7=strongly agree).

Data analysis and techniques

A Software Statistical Package SPSS version 25 is used to perform statistical tests. The demographic characteristics of the respondents were analyzed by descriptive statistics. Exploratory Factor Analysis (EFA) is used to extract factors and confirm the conceptual basis of variables or testing the validity.

Furthermore, Cronbach's Alpha is used to test the reliability of the measurements. And finally, multiple regression analysis is employed to test the effects of the independent variables on the dependent variable.

RESULTS

The questionnaire was distributed to various social media platforms such as Whatsapp, Instagram, Twitter, Facebook, to Telegram, and a total of 346 respondents were obtained. Before doing further analysis, the data were checked and only 314 data were valid. The data that did not match the research context, as some respondents had never purchased electronic products online and were over 36 years old, were eliminated. Details of the demographic characteristics of respondents are shown in Table 1. Majority respondents have bought electronic products online through the online marketplaces such as Tokopedia (76.7%) and Shopee (57.2%), and the most purchased products are laptop accessories (67.3%) and audio system (64.2%).

Goodness of Measurements

This research adopts and combines two different studies with slightly different contexts. Therefore, to ensure that the measurement items used to measure the variables are appropriate and accurate, it is necessary to measure goodness of

measures (Kamalul Ariffin et al., 2018). According to Sekaran and Bougie (2009), to test the goodness of measures can be used factor analysis and reliability analysis.

Table 1: Demographic Characteristics of the Respondents

|

Item |

Option |

Frequency |

% |

|

Gender |

Male |

191 |

60.8% |

|

Female |

123 314 |

39.2% | |

|

Age |

15-25 years old |

244 |

77.7% |

|

26-35 |

70 314 |

22.3% | |

|

Income (in Rp) |

<3.000.000 |

83 |

26.4% |

|

3.000.000 - 5.000.000 |

67 |

21.3% | |

|

5.000.001 - 10.000.000 |

116 |

36.9% | |

|

> 10.000.000 |

48 314 |

15.3% | |

|

Frequency of online shopping |

Once a week |

4 |

1.3% |

|

(for electronic product) |

Once a month |

10 |

2.9% |

|

Once in 3 months |

37 |

11.8% | |

|

Once in 6 months |

28 |

8.9% | |

|

Once a year |

154 |

49.0% | |

|

More than a year |

84 314 |

26.1% |

Source: Data Processed

Factor analysis

The factor analysis used in this study was exploratory factor analysis (EFA).

The use of EFA can confirm whether the measurement items used can measure the variables correctly in accordance

with variables previously identified. The EFA examines the structure of the interrelationships from a number of measurement items and groups the highly intercorrelated measurement items into dimensions that have the same factors or components, which means that the measurement items measure similar dimensions (Hair et al., 2019). Assumptions that must be met before conducting the EFA are Measure of Sampling Adequacy (MSA) and Bartlett's Test.

MSA is a measurement to measure the level of inter-correlation between variables (Hair et al., 2019). This study uses the Kaiser-Meyer-Olkin (KMO) measure of sampling adequacy which has a criterion value above 0.5 or in the range of 0.7 to 0.8 to be considered as good (Hair et al., 2019; Damasio, 2012). The next test used is the Bartlett's Test which examines the correlation between variables. Bartlett's test of sphericity is statistically significant if the p-value is below 0.05. In this study, the results of testing assumptions for all measurement items were carried out simultaneously

and resulted in a KMO value of 0.816 and a significant Bartlett's Test (p = 0.000). This indicates that the assumptions are met and the sample is adequate to run a factor analysis.

KMO testing, Bartlett's Test and the results of factor loadings for each variable are shown in Table 2. For each variable, the KMO value is above 0.5, which ranges from 0.640 to 0.814; Bartlett's Test for each variable is significant with significance level at 0.000; factor loading above 0.50. According to Hair et al. (2019), a factor loading value of 0.50 or more is considered as significant and a value above 0.70 is considered as an indication of a well-defined structure. There were 3 measurement items that were eliminated because they did not meet the factor loading criteria, namely ProdRisk5, TimeRisk4, and PsyRisk4.

Reliability

To evaluate the reliability, this study assesses the internal consistency of the measurement items that make up each variable or construct by looking at the Cronbach's Alpha coefficient. This

reliability measurement is needed to see Cronbach's Alpha for each variable is in

the consistency of the measurement the range of 0.635 to 0.862, which means

items in assessing a concept (Sekaran it has exceeded the lower limit and

and Bougie, 2009). The acceptable limit indicates that the measurement items

for Cronbach's Alpha is 0.7, but the used are stable and consistent in

lower limit of 0.6 can be used for measuring the concepts in each of the

exploratory research (Hair et al., 2019). existing variables.

As shown in Table 2, the value of

Table 2: Measurement of Scale and Exploratory Factor Analysis

|

Variabel / Construct |

Items Reference Factor KMO Loadings |

|

Financial Risk (Cronbach’s α = 0.750) |

FinRisk1: I tend to overspend my money Kamalul 0.639 0.750 (spendthrift) when buying electronic products Ariffin et online. al., 2018 0.743 FinRisk 2: I may be paying more than I should when buying electronic products online. FinRisk3: The electronic products I buy online 0.828 may not be worth the money I spend. FinRisk4: Shopping for electronic products 0.771 online can waste my money. FinRisk5: I don't trust companies that sell 0.548 electronic products online. |

|

Product Risk (Cronbach’s α = 0.787) |

ProdRisk1: I can't find the electronic product I Kamalul 0.596 0.755 want online. Ariffin et ProdRisk2: I may not receive the right quality of al., 2018 0.861 electronic products I buy online. ProdRisk3: I think the description about the size 0.844 of electronic product that is being sold online might not be accurate. ProdRisk4: It is difficult for me to compare the 0.808 quality of electronic products sold online with the other similar products. |

|

Security Risk (Cronbach’s α = 0.806) |

SecRisk1: I feel that the personal data on my Kamalul 0.787 0.753 credit or debit card is not safe when making Ariffin et transactions online. al., 2018 SecRisk2: I feel that websites or apps that sell 0.837 electronic products online may not be safe. |

|

SecRisk3: Companies that sell electronic products online may share my personal information. SecRisk4: I might be annoyed if I was contacted by other companies selling electronic products online. SecRisk5: I consider that information about companies selling electronic products online may be incomplete. |

0.811 0.669 0.647 |

|

Time Risk TimeRisk1: Buying electronic products online Kamalul (Cronbach’s can be a waste of my time. Ariffin et α = 0.813) TimeRisk2: It's hard for me to find websites or al., 2018 apps that sell electronic products online properly. TimeRisk3: It's hard for me to find the right electronic product online. |

0.785 0.677 0.876 0.896 |

|

Social Risk SocRisk1: The electronic products I buy online Kamalul (Cronbach’s may not be approved by my family. Ariffin et α = 0.755) SocRisk2: Shopping for electronic products al., 2018 online may affect my image in the eyes of the people around me. SocRisk3: Electronic products sold online may not be recognized by my relatives or friends. SocRisk4: Shopping for electronic products online may make others less judgmental of me. |

0.725 0.706 0.845 0.670 0.806 |

|

Psychological PsyRisk1: I can't trust a company that sells Kamalul Risk electronic products online. Ariffin et (Cronbach’s PsyRisk2: I am afraid that the electronic al., 2018 α = 0.635) products I buy online will not be delivered properly. PsyRisk3: I can get frustrated if I am not satisfied with the quality of the electronic products I buy online. |

0.744 0.640 0.802 0.737 |

|

Escapism EscMot1: Shopping for electronic products Dharmesti Motive online makes me feel like I'm in a new world. et al., 2021 (Cronbach’s EscMot2: I get so caught up in shopping for α = 0.836) electronics online that I forget everything. EscMot3: Shopping for electronic products online makes me “away from everything”. |

0.792 0.678 0.908 0.908 |

|

Value Motive ValMot1: I like shopping electronic products Dharmesti (Cronbach’s online for discounted items. et al., 2021 α = 0.862) ValMot2: I like shopping for electronic products online to find cheaper prices. |

0.751 0.814 0.907 |

|

ValMot3: I can find good deals when shopping 0.897 for electronics products online. ValMot4: I like to hunt for electronics products 0.842 online to get a good deal. | |

|

Online Purchase Intention (Cronbach’s α = 0.833) |

OPI1: I like shopping for electronic products Dharmesti 0.854 0.774 online. et al., 2021 OPI2: I have a strong intention to buy electronic 0.905 products online in the future. OPI3: I will buy electronic products online in 0.874 the future. OPI4: I often consider buying electronic 0.614 products online. |

Source: Data Processed

Regression analysis

Before doing regression testing, it is necessary to perform an examination in order to see the issue of multicollinearity. The ability to predict an independent variable can be influenced by the correlation between independent variables. It is stated than the higher the correlation between the independent variables, the lower the unique variance and predictive power of these independent variables (Hair et al., 2019). Multicollinearity testing can use 2 measurements, namely tolerance value and VIF.

The tolerance value is the amount of predictive ability of the independent

variable that is not predicted by other independent variables or in other words shows the unique variance of the independent variable. While the VIF value is the opposite of the tolerance value. According to Hair et al. (2019), a tolerance value of up to 0.1 or a VIF value of 10 usually indicates a multicollinearity problem. Meanwhile, based on Bhukya and Singh (2015), a VIF value below 3.0 indicates no multicollinearity problem. In this study, the tolerance value is obtained from 0.435 to 0.854 and the VIF value is in the range of 1.170 to 2.301 which indicates that there is no multicollinearity problem (Table 3).

Table 3: Multicollinearity Statistics

Collinearity Statistics

|

Tolerance |

VIF | |

|

Financial Risk |

0.532 |

1.879 |

|

Product Risk |

0.435 |

2.301 |

|

Security Risk |

0.711 |

1.406 |

|

Time Risk |

0.527 |

1.896 |

|

Social Risk |

0.651 |

1.535 |

|

Psychological Risk |

0.515 |

1.941 |

|

Escapism Motive |

0.731 |

1.367 |

|

Value Motive |

0.854 |

1.170 |

Notes: Dependent Variable: Online Purchase Intention

Source: Data Processed

Testing the fit model is firstly done by looking at the significance of the predictive model. The results of the ANOVA test showed that the predictive model was statistically significant with F(8, 305) = 18.212, significant at p < 0.001. The measurement of the coefficient of determination (R2) is used to measure the accuracy prediction for the regression model by showing the combined effect of the independent variables in predicting the dependent variable (Hair et al., 2019). However, the adjusted R2 value will be more useful because it can reflect overfitting and shows that the addition of variables does not contribute significantly to predictive accuracy.

The results of R2 and adjusted R2 in this study were 0.323 and 0.306 respectively. This means that the predictor variables, namely Financial Risk, Product Risk, Security Risk, Time Risk, Social Risk, Psychological Risk, Escapism Motive, and Value Motive can explain 30.6% -32.3% of the total variance of the dependent variable, namely Online Purchase Intention. This value is relatively low where the expected coefficient of determination is higher and closer to 1, as it means that the ability to predict the dependent variable is better. The last test of the fit model is the autocorrelation assessment using the Durbin-Watson Test. In this study, the Durbin-Watson value was in 2.027 or

close to 2 where a value equal to 2 indicates no autocorrelation in the model (Bhukya and Singh, 2015).

Multiple regression testing is used to examine the direct effects of the independent variables on the dependent variable as well as to test the proposed hypothesis. The perceived risk test built on 6 independent variables which is hypothesized as H1, H2, H3, H4, H5, H6 has a significant negative relationship to the dependent variable, i.e. online

purchase intention. The perceived value test built on 2 independent variables which are hypothesized as H7 and H8 has a significant positive relationship to the dependent variable online purchase intention. To see how influential the independent variable on the dependent variable is described with the value of the standardized coefficient (β) as the parameter estimation. The results of multiple regression can be seen in Table 4.

Table 4: Multiple Regression Coefficient and Hypothesis Testing

|

Hypothesis |

Path |

Standardized coefficients (β) |

t-values |

p-values |

Result |

|

H1 |

Financial Risk → Online Purchase Intention |

0.088 |

1.358 |

0.176 |

Not Supported |

|

H2 |

Product Risk → Online Purchase Intention |

-0.157 |

-2.193 |

0.029 |

Supported |

|

H3 |

Security Risk → Online Purchase Intention |

-0.113 |

-2.025 |

0.044 |

Supported |

|

H4 |

Time Risk → Online Purchase Intention |

-0.033 |

-0.504 |

0.615 |

Not Supported |

|

H5 |

Social Risk → Online Purchase Intention |

0.101 |

1.731 |

0.085 |

Not Supported |

|

H6 |

Psychological Risk → Online Purchase Intention |

-0.010 |

-0.156 |

0.876 |

Not Supported |

|

H7 |

Escapism Motive → Online Purchase Intention |

0.290 |

5.272 |

0.000 |

Supported |

H8 Value Motive → Online

0.368 7.213 0.000 Supported

Purchase Intention

Notes: Significant levels p < 0.05 Source: Data Processed

With p<0.05, the t-value results were only significant on four factors: product risk (β = -0.157, p<0.05), security risk (β = -0.113, p<0.05), escapism motive (β = 0.290, p<0.05) and value motive (β = 0.368, p<0.05). It can be concluded that of the 6 hypotheses related to perceived risk (H1 to H6), there is only 2 hypothesis, namely H2 and H3 are proven which are product risk has a significant negative relationship to online purchase intention and security risk has a significant negative relationship to online purchase intention. Meanwhile, from 2 hypotheses related to perceived value (H7 and H8), both of them are proven that the escapism motive variable has a significantly positive relationship to online purchase intention and the value motive variable has a significantly positive relationship to online purchase intention. Of the four significant factors,

value motive variable has the highest coefficient value or it can be said that increasing the value motive will give the highest positive impact on online purchase intentions.

Discussion

The main objective of the current study is to examine the factors of perceived risk and perceived value that influence online purchase intention of electronic products in Indonesia. From the perceived risk perspective, the results showed that product risk factor and security risk factor have a significant negative impact on online purchase intention. Regarding to the product risk, this finding is supported by the previous literature where consumers tend to have a high concern if the received product could not function as how they expected it to be (Kim et al., 2008). The product risk intensifies when it comes to electronic products as

electronics is not considered as a cheap product category, young consumers find it difficult to find accurate information about the product’s specifications such as product features and sizes. Moreover, as stated by Popli & Mishra (2015); Kamalul Ariffin et al., (2018), prevalent young consumers who buy electronic products online find it hard to only rely on seller’s given information as they think that the given information is limited. For that reason, according to Google Research (2011), an average electronic shopper utilizes 21 sources of information to come to a decision. This is even aggravated with the fact that young consumers could not see the product directly before buying.

The findings about security risk were also supported prior study that stated security risk has a negative influence on online purchase intentions. The previous literature suggests that consumers are mostly afraid to make online purchase if there is no information about the secure mechanism of online shopping (Masoud, 2013). Consumers are more

likely to have security fears when the companies do not give them assurance that their website or payment methods are secure. They worried because online mechanism is related to hacking and online fraud. Consumers usually perceived that hackers can expose online consumer card information which exposes the security of online transactions as potential loss. Further, consumers also concerned that the online shopping companies or the hacker can leak their personal information. For these reasons, consumers’ purchase intention is negatively influenced by the perceived security risk. The more security risks perceived by the consumers, the online purchase intentions will be lower.

Moreover, the other factors of perceived risk are not supported by the previous research (Kamalul Ariffin et al., 2018), where financial risk, time risk, and psychological risk are found to have significant negative influence on consumer online purchase intention. The financial risk has no significant negative effect as nowadays, after the

COVID-19 pandemic hits, young consumers tend to have built their trust towards the companies who sold their products online. Moreover, in the context of financial risk, most ecommerce nowadays are providing plentiful discounts or promos and allowing young consumers to compare product prices among different stores. This might be the reason for the insignificant effect of financial risk. As for the time risk, with current advanced technology, young consumers tend to perceive online shopping as time saving because there is no need to visit the retail store. Moreover the findings stated by Almousa (2011), time risks are not very relevant in today’s era as nowadays because it does not take long time for a website to load, consumer’s order tends to be processed quickly, and lastly, consumers could choose the ‘instant or same day’ delivery system. These arguments could be the reason for the insignificant effect to time risk. In terms of psychological risk, although there is a bit of concern if the product might not correspond to consumer’s expectation, many online companies or

e-commerce nowadays have provided solution if the product does not match, damaged, or other problems with the purchased product by allowing the consumers to return the product and claim a refund to the seller. Therefore, the young consumers’ psychological risk can be redeemed by using those solutions offered by e-commerce. Lastly, the social risk is corresponding with the research of Kamalul Ariffin et al. (2018) where this variable is found to be insignificant.

Further, in terms of perceived value, the results showed both escapism motive and value motive to have significant positive influence on online purchase intention. The escapism motive is found to be significant as shopping electronic products online could help the young consumers to escape themselves from the boredom of daily activities (Goldring & Azab, 2020). Furthermore, the extensive research which young consumers perform before buying the electronic product, makes them feel away from boredom of the daily activities. As for the value motive,

young consumers feel that shopping for electronic products online will help them to find the great value between a product's quality and its price. With the ease of comparing among products, brands, and stores and the abundant promos offered by online shopping companies, the value motive significantly influences young consumers' online purchase intention in a positive way.

CONCLUSIONS

From the findings and discussions, it is found that product risk and security risk of young consumers in Indonesia have a significant negative effect on their online purchase intentions. To reduce the product risk perceived by the consumers, online sellers of electronics products can give a detailed and accurate description (e.g features, size, photo of product) so that the consumers know exactly the specification of the products they are buying. By giving detailed and accurate information, sellers can set the consumers expectation based on the description available. Product risk can also be

reduced by providing reviews from existing consumers or discussion forums. For example, online sellers can provide an open discussion forum so that the consumers can ask the seller about any question before buying, and also the other consumers can read the discussion. Regarding security risk, online sellers must ensure that they create a secure transaction system and ensure the privacy of their customers. Online sellers can take advantage of increasingly sophisticated technologies such as working with trusted third parties (such as payment gateways) or using well-known e-commerce platforms to make sales. Online sellers also need to communicate their regulatory policy framework to consumers so that they can be confident in making purchases.

The findings also confirmed that the two motives of perceived value can increase the online purchase intention, namely escapism motive and value motive. To increase the escapism motive, sellers can create and set the product display as interesting as possible. The more

comfortable the online shopping place, the more likely consumers gain positive feelings during the online shopping process and drive the intentions to purchase (Lim, 2017). The online sellers can formulate their strategies. Thus, more consumers will be more interested and boost their intention to purchase, especially when the main target are young consumers who usually are bargain hunters (Phau and Woo, 2008). Young consumers tend to recognize the power of online shopping in order to find the good value amongst many alternatives (Hill et al., 2013).

The present study bears some limitations that can provide direction for future studies. First, related to the sample. The current study only examined young consumers in Indonesia. Future research can examine other generations. It is an opportunity to compare inter-generations and get further insights for different marketing strategies. In addition, to enhance the generalizability of findings, future research can examine young consumers

in other developing and developed countries.

Second, this research examined the direct effects of perceived risks and perceived values on online purchase intention. Future research can elaborate the mediation or moderation variables in the model. This will enrich the findings that contribute on theoretical and managerial contributions.

REFERENCES

Ahmed, M.E., Samad, N. and Khan, A.G., 2021. Factors Influencing Online Purchase Intention: A Case of University Students in Pakistan. EJSS 9, 31–43.

https://doi.org/10.15604/ejss.2 021.09.01.004

Ahn, T., Ryu, S. and Han, I., 2007. The impact of Web quality and playfulness on user acceptance of online retailing. Information & Management 44, 263–275.

https://doi.org/10.1016/j.im.20 06.12.008

Almousa, M., 2011. Perceived Risk in Apparel Online Shopping: A Multi Dimensional Perspective. Canadian Social Science 7, 23-31.

Ariff, M.S.M., Sylvester, M., Zakuan, N., Ismail, K. and Ali, K.M., 2014. Consumer Perceived Risk, Attitude and Online Shopping Behaviour; Empirical Evidence from Malaysia. IOP Conf. Ser.: Mater. Sci. Eng. 58, 012007.

https://doi.org/10.1088/1757-899X/58/1/012007

Barnes, S.J., Bauer, H.H., Neumann, M.M. and Huber, F., 2007.

Segmenting cyberspace: a

customer typology for the internet. European Journal of Marketing 41, 71–93.

https://doi.org/10.1108/030905 60710718120

Bartik, A.W., Bertrand, M., Cullen, Z., Glaeser, E.L., Luca, M. and Stanton, C., 2020. The impact of COVID-19 on small business outcomes and expectations. Proc Natl Acad Sci USA 117, 17656– 17666.

https://doi.org/10.1073/pnas.2 006991117

Buehler, R. and Griffin, D., 1994.

Change-of-meaning effects in

conformity and dissent:

Observing construal processes over time. Journal of Personality and Social Psychology 67, 984– 996.

https://doi.org/10.1037/0022-3514.67.6.984

Bhatti, A., Saad, S. and Gbadebo, S.M., 2019. Effect of Financial Risk, Privacy Risk and Product Risk on Online Shopping Behavior. Pak. J. Humanit. Soc. Sci 7, 342– 356.

https://doi.org/10.52131/pjhss. 2019.0704.0091

Bhukya, R. and Singh, S., 2015. The effect of perceived risk dimensions on purchase

intention. American Journal of Business 30, 218–230.

https://doi.org/10.1108/AJB-10-2014-0055

Bloch, P.H., Sherrell, D.L. and Ridgway, N.M., 1986. Consumer Search: An Extended Framework. J CONSUM RES 13, 119.

https://doi.org/10.1086/209052

Chen, H., 2012. The Influence of

Perceived Value and Trust on Online Buying Intention. Journal of Computers, 1655– 1662.

https://doi.org/10.4304/jcp.7.7. 1655-1662

Cheong, J.W., Muthaly, S., Kuppusamy, M. and Han, C., 2020. The study of online reviews and its relationship to online purchase intention for electronic products among the millennials in Malaysia. APJML 32, 1519–1538. https://doi.org/10.1108/APJM L-03-2019-0192

Chetty, R., Friedman, J.N., Hendren, N. and Stepner, M., n.d. Real-Time Economics: A New Platform to Track the Impacts of COVID-19 on People, Businesses, and Communities Using Private Sector Data 26.

Damásio, B.F., 2012. Uso da análise

psicologia 11, 16.

Derbaix, C., 1983. Perceived risk and risk relievers: An empirical investigation. Journalof

https://doi.org/10.1016/0167-4870(83)90056-9

Dharmesti, M., Dharmesti, T.R.S.,

Kuhne, S. and Thaichon, P., 2021. Understanding online

shopping behaviours and purchase intentions amongst millennials. YC 22, 152–167.

https://doi.org/10.1108/YC-12-2018-0922

Donthu, N. and Gustafsson, A., 2020. Effects of COVID-19 on business and research. Journal of Business Research 117, 284–289. https://doi.org/10.1016/j.jbusr es.2020.06.008

Dowling, G.R. and Staelin, R., 1994. A Model of Perceived Risk and Intended Risk-Handling

Activity. J CONSUM RES 21, 119.

https://doi.org/10.1086/209386

Finneman, B., 2020. Meet Generation Z: Shaping the future of shopping. [online] McKinsey & Company. Available at:

Goldring, D. and Azab, C., 2021. New rules of social media shopping: Personality differences of U.S. Gen Z versus Gen X market mavens. J Consumer Behav 20, 884–897.

https://doi.org/10.1002/cb.189 3

Thinkwithgoogle.com. 2011. The zero moment of truth for consumer electronics study. [online] Available at:

<https://www.thinkwithgoogle .com/consumer-insights/consumer-trends/zmot-consumer-electronics/>

Haider, A. and Nasir, N., 2016. Factors Affecting Online Shopping Behavior of Consumers in Lahore, Pakistan 6.

Hair, J., Anderson, R., Babin, B. and Black, W., 2019. Multivariate

data analysis. Australia:

Cengage.

Han, M.C. and Kim, Y., 2017. Why

Consumers Hesitate to Shop

Online: Perceived Risk and

Product Involvement on

Taobao.com. Journal of

Promotion Management 23, 24– 44.

https://doi.org/10.1080/104964 91.2016.1251530

Heirsh Soltanpanah, 2012. A review of the literature of perceived risk and identifying its various facets in e- commerce by customers: Focusing on

developing countries. Afr. J.

Bus. Manage. 6.

https://doi.org/10.5897/AJBM 11.1409

Hill, W.W., Beatty, E.S. and Walsh, G., 2013. A segmentation of adolescent online users and shoppers. Journal of Services Marketing 27, 347–360.

https://doi.org/10.1108/JSM-10-2011-0157

Holbrook, M.B. and Corfman, K.P., 1985. Quality and value in the consumption experience:

Phaedrus rides again. Perceived quality, 31, 31-57.

Hsin Chang, H. and Wen Chen, S., 2008. The impact of online store environment cues on purchase intention: Trust and perceived risk as a mediator. Online

Information Review 32, 818–841. https://doi.org/10.1108/146845 20810923953

Internetworldstats.com. 2021. World Internet Users Statistics and 2021 World Population Stats. [online] Available at:

<https://internetworldstats.co m/stats.htm> [Accessed 23 November 2021].

Jackson, V., Stoel, L. and Brantley, A., 2011. Mall attributes and shopping value: Differences by gender and generational cohort. Journal of Retailing and Consumer Services 18, 1–9.

https://doi.org/10.1016/j.jretco nser.2010.08.002

Jamali, S.K. and Samadi, B., 2014.

Prioritizing electronic commerce technologies in Iranian family SMEs 6, 35.

Kamalul Ariffin, S., Mohan, T. and Goh, Y.-N., 2018. Influence of

consumers’ perceived risk on consumers’ online purchase intention. JRIM 12, 309–327.

https://doi.org/10.1108/JRIM-11-2017-0100

Kayworth, T.R. and Whitten, D., 2010. Effective information security requires a balance of social and technology factors. MIS

Quarterly Executive, 9, 163.

Kim, D.J., Ferrin, D.L. and Rao, H.R., 2008. A trust-based consumer decision-making model in electronic commerce: The role of trust, perceived risk, and their antecedents. Decision Support Systems 44, 544–564.

https://doi.org/10.1016/j.dss.2 007.07.001

Kim, J. and Lennon, S.J., 2013. Effects of reputation and website quality on online consumers’ emotion, perceived risk and purchase intention: Based on the

stimulus‐organism‐response model. Journal of Research in Interactive Marketing 7, 33–56. https://doi.org/10.1108/175059 31311316734

Ko, H., Jung, J., Kim, J. and Shim, S.W., 2004. Cross-Cultural Differences in Perceived Risk of Online Shopping. Journal of Interactive Advertising 4, 20–29.

https://doi.org/10.1080/152520 19.2004.10722084

Lavuri, R. 2021. "Intrinsic factors affecting online impulsive shopping during the COVID-19 in emerging markets",

International Journal of

Emerging Markets.

https://doi.org/10.1108/IJOEM -12-2020-1530

Lee, K.S. and Tan, S.J., 2003. E-retailing versus physical retailing. Journal of Business Research 56, 877–885.

https://doi.org/10.1016/S0148-2963(01)00274-0

Leeraphong, A. and Mardjo, A., 2013. Trust and Risk in Purchase Intention through Online Social Network: A Focus Group Study of Facebook in Thailand. JOEBM 314–318.

https://doi.org/10.7763/JOEB M.2013.V1.68

Li, N. and Zhang, P., 2002. Consumer Online Shopping Attitudes and Behavior: An Assessment of

Research. AMCIS 2002

Proceedings, 74

Lim, W.M., 2017. Untangling the

relationships between consumer characteristics, shopping values, and behavioral intention in online group buying. Journal of Strategic Marketing 25, 547–566. https://doi.org/10.1080/096525 4X.2016.1148767.

Littler, D. and Melanthiou, D., 2006. Consumer perceptions of risk and uncertainty and the

implications for behaviour

towards innovative retail services: The case of Internet Banking. Journal of Retailing and Consumer Services 13, 431– 443.

https://doi.org/10.1016/j.jretco nser.2006.02.006.

Masoud, E.Y., 2013. The Effect of

Perceived Risk on Online Shopping in Jordan. European Journal of Business and Management 14.

McLean, G., AlNabhani, K. and Marriott, H., 2021. ‘Regrettable escapism’ the negative effects of mobile app use: A retail

perspective. Psychology and marketing.

https://doi.org/10.1002/mar.21 584

Meola, A., 2021. Generation Z News: Latest characteristics, research, and facts. [online] Insider Intelligence. Available at: <https://www.insiderintelligen

ce.com/insights/generation-z-facts/>

Mirabi, D.V., Akbariyeh, H. and

Tahmasebifard, H., 2015. A

Study of Factors Affecting on Customers Purchase Intention. Journal of Multidisciplinary Engineering Science and Technology (JMEST), 2,7.

Mitchell, V., 1998. A role for consumer risk perceptions in grocery retailing. British Food Journal 100, 171–183.

https://doi.org/10.1108/000707 09810207856.

Ng, S.I., Ho, J.A., Lim, X.J., Chong, K.L. and Latiff, K., 2021. Mirror,

mirror on the wall, are we ready for Gen-Z in marketplace? A study of smart retailing technology in Malaysia. YC 22, 68–89.

https://doi.org/10.1108/YC-06-2019-1006.

Pavlou, P. A., 2003. Consumer

Acceptance of Electronic Commerce: Integrating Trust

and Risk with the Technology Acceptance Model, 2003..

134.

https://doi.org/10.1080/108644 15.2003.11044275.

Paynter, J. and Lim, J., 2001. Drivers and impediments to e-commerce in Malaysia. Malaysian Journal of Library and Information Science 6, 1-9

Phau, I. and Woo, C., 2008.

Understanding compulsive

buying tendencies among young Australians: The roles of

money attitude and credit card usage. Marketing Intelligence & Plan 26, 441–458.

https://doi.org/10.1108/026345 00810894307.

Popli, A. and Mishra, S., 2015. Factors of Perceived Risk Affecting Online Purchase Decisions of

Consumers. Pacific Business Review International 8, 49.

Salisbury, W.D., Pearson, R.A., Pearson, A.W. and Miller, D.W., 2001.

Perceived security and

worldwide web purchase intention. Industrial

Management & Data Systems 101, 165-177.

Santo, P.E. and Marques, A.M.A., 2021, Determinants of the online purchase intention: hedonic

motivations, prices, information and trust. Baltic Journal of Management, Vol. ahead-of-print No. ahead-of-print.

Satar, M., Safie, N., Dastane, O. and Maarif, M. Y., 2019. Customer value proposition for Ecommerce: A case study

approach. International Journal of Advanced Computer Science and Applications 10, 454-458.

http://dx.doi.org/ 10.14569/IJACSA.2019.0100259.

Schiffman, L. and L.L. Kanuk, 2007. Consumer Behavior, 8th

Edition. Pearson Education.

Sinha, P. and Singh, S., 2017. Comparing Risks and Benefits for the Value Enhancement of Online

Purchases. Gadjah Mada International Journal of Business 21.

http://dx.doi.org/10.22146/ga maijb.10512.

Stocchi, L., Pourazad, N. and Michaelidou, N., 2020.

Identification of two decision‐ making paths underpinning the continued use of branded apps. Psychology & Marketing 37, 1362–1377.

https://doi.org/10.1002/mar.21 385 .

Tran, V. D., 2020. The Relationship

among Product Risk, Perceived Satisfaction and Purchase Intentions for Online Shopping. The Journal of Asian Finance, Economics and Business 7, 221– 231.

https://doi.org/10.13106/JAFE B.2020.VOL7.NO6.22.

Ueltschy, L.C., Krampf, R.F. and Yannopoulos, P., 2004, A Cross National Study Of Perceived Consumer Risk Towards Online (Internet) Purchasing.

Multinational Business Review 12, 59-82.

https://doi.org/10.1108/152538 3X200400010

Uma Sekaran and Bougie, R., 2009.

Research Methods For Business: A Skill Building Approach, 5th ed. United Kingdom: Wiley.

Wood, W. and Hayes, T., 2012. Social influence on consumer

decisions: Motives, modes, and consequences. Journal of Consumer Psychology 22, 324– 328.

https://doi.org/10.1016/j.jcps.2 012.05.003.

Ye, N., 2004. Dimensions of consumer’s perceived risk in online shopping. Journal of Electronic Science and Technology of China 2.

Zeithaml, V. A., 1988. Consumer

Perceptions of Price, Quality, and Value: A Means-End Model and Synthesis of Evidence. Journal of Marketing, 52, 2.

https://doi.org/10.2307/125144 6.

270

Discussion and feedback