Accountability of Tri Hita Karana's Cultural Perspective in Socio-religious Organization

on

Jurnal Ilmiah Akuntansi dan Bisnis

Vol. 17 No. 2, July 2022

Accountability of Tri Hita Karana's Cultural Perspective in Socio-religious Organization

|

Ni Made Dwi Rina1*, I Ketut Sujana2, I Putu Sudana3, I Gde Ary Wirajaya4 | |

|

AFFILIATION: 1,2,3,4Faculty of Economics and Business, Universitas Udayana, Indonesia |

Abstract This study covers a deep understanding of how the management of the Sagraha Mandra Kantha Santhi Foundation (SMKS) carries out accountability in the Tri Hita Karana cultural perspective. The purpose of |

|

*CORRESPONDENCE: |

this study is to interpret the experiences of the informants on the actions of accountability in the perspective of Tri Hita Karana culture and in what |

|

THIS ARTICLE IS AVAILABLE IN: |

situations they interpret it. The methodology of this research is descriptive |

|

interpretive with the approach of Interpretative Phenomenological Analysis (IPA). Qualitative data was collected by conducting observations, | |

|

DOI: |

in-depth interviews and documentation. The findings indicate that the |

|

10.24843/JIAB.2020.v17.i02.p08 |

Sagraha Mandra Kantha Santhi Foundation is accountable to God (parahyangan), to others (pawongan) and to the environment |

|

CITATION: Rina, N. M. D., Sujana, I K., Sudana, I P. & Wirajaya, I G. A. (2022). Accountability of Tri Hita Karana's Cultural Perspective in Socioreligious Organization. Akuntansi dan Bisnis, 17(2), 298-312. |

(palemahan). The analysis also shows that there are three themes that emerge from the meaning of the experience of the informants in the cultural perspective of Tri Hita Karana, namely sincere offerings, economic contributions to society, and protecting the environment. Keywords: accountability, culture, tri hita karana, non-governmental |

|

ARTICLE HISTORY Received: |

organization |

28 February 2022

|

Revised: |

Introduction |

|

16 June 2022 |

The Sagraha Mandra Kantha Santhi Foundation (SMKS) is an NGO engaged |

|

in the socio-religious field, which is in Bali with the business unit being | |

|

Accepted: 15 July 2022 |

carried out is ngaben (cremation) activities through the crematorium and this NGO is not profit-oriented in accordance with the Foundation's Deed of Establishment No. AHU-0017783.AH.01.04 Year 2018. This ngaben ceremony is a completion to the body of someone who has died (Hanggara et al., 2017). In its activities, the SMKS Foundation proposes a good governance mechanism to achieve the desired goals and objectives. One element of the implementation of governance that must be observed by each entity is accountability (Kaban & Luther, 2010). Accountability begins with fulfilling a request or obligation to justify an activity that is carried out by a person against another person in response (Gray et al., 2006). The essence of accountability is about providing information between two parties, one party is responsible for providing an explanation or justification for the other party as accountability is their right, so, Accountability is the process of justifying desires and actions to assess whether the management is responsible to the stakeholders (Gross et al., 2012). |

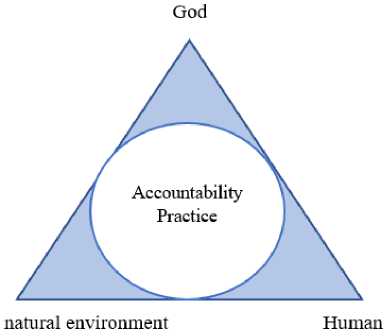

Triyuwono (2011) revealed that accountability is classified into three types, namely accountability to God, accountability to stakeholders, and accountability to nature. In Hinduism, these three accounts can be linked to the cultural concept of Tri Hita Karana, namely the three causes of human welfare in achieving the life goals of moksartham Jagadhita ya ca iti dharma which basically stems from the harmony of human relations with God (parahyangan), harmony of human relations with others (pawongan) and the harmony of human relations with the natural environment (palemahan) (Saputra et al., 2018). Several studies show that accountability is one of the important principles in good governance Kumalawati & Atmadja, (2020); Aryasa & Musmini (2020); Wijaya et al., (2020); Wati et al., (2017); Silvia et al., (2011).

The concept of Tri Hita Karana, which developed in Bali, is a cultural concept rooted in religious teachings (Saputra et al., 2018) which is considered capable of increasing financial management accountability. In increasing the economic resilience of the Balinese people, apart from seeing the existing potential, the government must also improve the local community's social structure, culture, and mentality. The concept of Tri Hita Karana religiosity is used because it is considered capable of creating a culture of honesty (Adiputra et al., 2014), openness, assistance and eliminating opportunities for fraudulent acts (Saputra et al., 2018). So, the use of the concept of religiosity in accounting, which in this case is for financial management, aims to prevent fraud, but God and nature do not need financial reports or annual reports, not like other stakeholders who require formal accountability, but what is important here is how God's laws are practiced in activities at the SMKS Foundation and how the rights of nature are fulfilled responsibly.

Human relations in the cultural perspective of Tri Hita Karana can be seen from the vertical relationship with God and the horizontal relationship with others and the natural environment. This understanding shows individual humans as agents in this life who have three principals, namely to God as "the creator, preserver and fuser", humans as social beings and the natural environment in which humans live.

An entity has an obligation to the community in the form of providing activity reports to the public as the entity reports operating activities to interested parties and this is a form of social responsibility (accountability) of the entity in general (Muttakin et al., 2015) and with good accountability it will bring three benefits. First, increasing the transparency of an entity. Second, improve the quality of decisions made by the entity.

Figure 1. Tri Hita Karana's Concept of Accountability Dimensions

Source: THK Award (Wardana & Putra, 2012) modified

The better the quality and quantity of information collected, the better the capacity the organization has in making good decisions for the organization and the public. The last benefit is to provide a clearer picture of the responsibilities of each role in the entity (Beckett & Jonker, 2002).

Based on scientific literature sources, it shows that research on the accountability of Tri Hita Karana to NGOs using the Interpretative Phenomenological Analysis (IPA) method has not been widely carried out, then in this study used the IPA method with data collection techniques carried out by conducting observations, in-depth interviews and documentation. After the data is collected, the data will be analyzed using the IPA method. Phenomenology attempts to explain the meaning of a number of people's life experiences about a concept or phenomenon, including their own self-concept or view of life (Creswell & Poth, 2018). This IPA method is unique because researchers gain an understanding of social reality through inductive thinking based on the experience of informants on accountability, which can be seen from two focuses, namely (a) textural description, what is experienced by the research subject about a phenomenon. What is experienced is an objective aspect, factual data, things that happen empirically. (b) structural description, how the subject experiences and interprets the experience. This description contains a subjective aspect. This aspect concerns the subject, judgments, feelings, expectations, and other subjective responses of the research subject related to the experience.

There are many studies examining accountability, such as for public sector organizations (Sayuti et al., 2018; Randa & Daromes, 2015; Pandeni, 2017), religious organization (Kepramareni et al., 2014; Kamaruddin & Ramli, 2018; Manguma et al., 2020), business organization (Alang et al., 2019), non-government organization (Deni et al., 2019), social organization (Massud & Aktar, 2020; Goddard, 2021), and other community organizations (Yasmin et al., 2021; Sujana et al., 2015). In terms of methodology, research that examines accountability has been carried out with a positive approach (Adiwirya & Sudana, 2015) and non-positivistic approaches such as critical (Riyanti, 2020), interpretive (Paranoan, 2015), ethnography (Wirajaya et al., 2014; Randa et al., 2011; Scobie et al., 2020; Jayasinghe & Soobaroyen, 2009), case study (Sari & Sudana, 2020). In addition, several studies that use phenomenological studies are (Komalasari et al., 2019; Rodliyah et al., 2021; Riskiyadi et al., 2022; Vidyantari et al., 2022).

As a foundation that provides services from religious activities, the relationship between the SMKS Foundation and the community is quite close, because it is not an economic relationship but rather a moral and non-formal relationship. The concept of accountability, especially in the SMKS Foundation, arises because of the differences in the functions and duties within the Foundation so that a separate evaluation is required of the duties and work. In addition, conflicts can also occur when the community cannot monitor and do not have much information about the SMKS Foundation as a whole. So that good governance, one of which is accountability, is expected to reduce the occurrence of fraud. Ethically, the management of the SMKS Foundation does not only pay attention to the management of funds, but also pays attention to the impact it has on the social, natural environment and the highest is to God, in this case it can be related to the Tri Hita Karana culture, so this research is important to do to explore how far where the management of the Foundation defines accountability in the perspective of the Tri Hita Karana culture and in what situations the management gains this experience. So, the

purpose of this study is to interpret the experiences of the informants about accountability actions in the perspective of Tri Hita Karana culture and in what situations they interpret it. In addition, this research can also be used as a reference for entities engaged in the crematorium regarding the accountability implemented by the SMKS Foundation.

The difference between previous research and current research is the entity being studied, namely the Sagraha Mandra Kantha Santhi Foundation, Bangli with its activity, namely Ngaben. Then in terms of moments, the SMKS Foundation has for one year been the only Foundation in Bali that accepts corpses that are positive for Covid-19 to carry out the Ngaben ceremony and this is what distinguishes this research from previous research.

Research Method

This study uses an Interpretative Phenomenological Analysis (IPA) approach proposed by Jonathan Smith in 1996. IPA is an approach where data is obtained and studied in an indepth way and sees each case as something unique (Smith et al., 2009). In addition, IPA aims to reveal in detail how informants interpret their personal and social world (Helaluddin, 2018). This study also uses an interpretive paradigm as a basis for obtaining meaning regarding the harmonization of accountability practices on the understanding of informants. Interpretive research does not place objectivity as the most important thing, but recognizes that in order to gain a deep understanding, the subjectivity of the informants must be explored as deeply as possible and this allows a trade off between objectivity and the depth of research findings (Chariri, 2009).

This study uses qualitative data types. The data sources in this study consisted of two sources, first primary data, namely data obtained directly from the source by conducting direct observations in the field in order to obtain internal data from respondents and then processed by researchers. The primary data in this research is in the form of data obtained directly from informants in the form of direct communication (interviews), as well as observations of activities that occur during the research process in order to find out information about accountability in the perspective of local culture at the SMKS Foundation. Second, secondary data, namely data obtained from other sources or existing data, collected for a specific purpose. The data obtained using the literature and also related to this research. This data was obtained by using the method of literature study and field study. The secondary data in this study are the SMKS Foundation Decree, the 2019 and 2020 management accountability reports, and the 2019 and 2020 general cash books.

In this study, the researcher chose to use two types of informants, namely key informants and supporting informants. Key informants are those who know in depth the problems being researched, and supporting informants are informants who are determined on the basis of consideration of having knowledge and often dealing formally or informally with key informants. The key informants in this study were the management of the SMKS Foundation, namely the chairman, treasurer, and secretary, then the supporting informants were the supervisors of the SMKS Foundation and service users. For the data collection process, the researcher did it in three ways, namely by observation, in-depth interviews, and documentation. Observation is used to collect data related to an event, location, object, and image design (Sugiyono, 2011). Through the application of observation techniques, researchers will make direct visits to the research site, namely the SMKS Foundation in Bangli. This was carried out to obtain valid and accurate data in

accordance with the reality observed by the researcher. After observing and determining informants, the next step is to conduct in-depth interviews. According to Smith et al., (2009), using data collection techniques with in-depth interviews is one of the best ways in the science method. In the process, the interview must be personal and the informant must feel comfortable and familiar. So that informants are more flexible in telling their experiences. The process of obtaining data can also be done using documentation techniques to provide complete data from the results of interviews and observations. Documentation techniques are usually needed to provide an overview of the confirmation that the research carried out is guaranteed to be authentic.

Although this research has received approval from the Head of the SMKS Foundation and all informants, the ethical principles of inform consent, anonymity, confidentiality, and justice (Hidayat, 2007) are still being carried out by researchers, (1) inform consent aims to provide an explanation to the informant regarding the aims and objectives of the research as well as to provide a consent form to become an informant so that the informant understands the aims and objectives of the research and knows its impact, (2) anonymity is trying to maintain confidentiality, meaning that the identity of the respondent is maintained, (3) confidentiality is maintaining the confidentiality of all information obtained from research informants, and (4) justice is that researchers will treat all informants well and fairly, all informants will get the same treatment from research conducted by researchers.

From the data obtained in the field, it was analyzed using the IPA method (Smith et al., 2009), namely (1) reading and re-reading, the form of activity at this stage is to write interview transcripts from audio recordings into written transcripts. (2) initial noting, at this stage the researcher can note something interesting from the transcript that has been made. (3) developing emergent themes, at this stage the researcher is allowed to take a theme from the data. (4) searching for connections across emergent themes, after the researcher finds the existing themes, the researcher must connect one theme to another to find a continuity between themes. (5) moving to the next case, if stage one to stage four has been carried out, then move to the next informant. (6) looking for patterns across cases, the final stage in this analysis is looking for relationships that exist between one case and another so that it forms a pattern that shows the relationship between cases.

To obtain the validity of the data, in this research, the technique of checking the validity of the data is carried out first. The validity of the data in qualitative research (Sugiyono, 2011) includes (1) credibility (internal validity), internal validity testing was carried out by triangulation, researchers chose to use source triangulation in this study. (2) transferability (external validity), external validity is used to determine whether the research can be applied or used in other situations. (3) dependability, a research that is dependability if other people can repeat or replicate the research. (4) confirmability, is proof of the truth of the research results, where the research results are in accordance with the data collected and included in the field report. This is done by confirming the results of the study with informants.

Result and Discussion

There are several steps in the IPA analysis carried out by researchers to find emerging themes. Manuscripts of each key informant were analyzed using the IPA analysis proposed by Smith, namely the first reading and re-reading by repeatedly reading the script obtained from the informant, then the second step is initial noting, namely making

Table 1. Matrix of Themes and Informants

|

Informant Identity |

Themes in THK |

Themes outside THK | ||

|

Parahyangan |

Palemahan |

Pawongan | ||

|

I1 |

|

|

a. protecting the environment |

- |

|

I2 |

a. Sincere offerings |

|

a. protecting the environment |

- |

|

I3 |

a. Sincere offerings |

|

a. protecting the environment |

- |

Source: Processed Data, 2021

some notes from the text that has been read which can also be called a significant statement. The third step is developing emergent themes, from some notes made will help researchers to find emerging themes. The fourth step is searching for connections across emergent themes, so to find continuity between the themes obtained, the researcher connects all the existing themes. The fifth step is moving to the next case, which is doing stages one to the fourth stage for the next informant, and the last step is looking for patterns across cases, which is looking for relationships in all cases so as to form a pattern that shows the interrelationships between cases. As a study material the interpretation of the meaning of experience is based on a theme matrix that contains emerging themes from each informant. The following is a table of themes and informants that displays emerging themes in each matrix box.

The general description of the theme matrix that has been presented shows that the three informants have the same three themes. From the parahyangan accountability theme carried out by the three informants, it is interpreted as a sincere offering. In the pawongan accountability theme carried out by the three informants, it is interpreted by making economic contributions to the community. On the theme of palemahan accountability carried out by the three informants it is interpreted as protecting the environment.

Accountability to God is abstract and individual, everything that is done by informant 1, informant 2, and informant 3 as the management of the SMKS Foundation and all the truth can only be felt and understood by the person concerned. Foundation management can remind each other to always do good and act according to God's orders, especially when holding the trust of service users so that all funds given can be used according to the flow. When the Foundation's management holds the trust of service users, at that time the Foundation's management holds the trust of God, because if the Foundation's management does bad things to other people, it's the same as the Foundation's management does not keep the trust of God because they do bad things. All of that is only felt by the Foundation's management personally, so maintaining a

relationship with God is very important so that the management can control the actions they do personally as a form of accountability aimed at God.

There are many things that can be done to give accountability to God, for example, is to give a sincere offering without any burden to God. God never asks for large and luxurious offerings to the people, a simple offering but given with sincere feelings will be more meaningful. This is what the management of the SMKS Foundation understands, so that the management of the Foundation in carrying out offerings and when performing the ritual is always carried out in accordance with the capabilities possessed by the Foundation so that it does not become a burden in the future. Whatever and however much one has, that amount is given as an offering to God. Like the meaning of a sincere offering from informant one.

“…God never asks about big or small offerings, obviously the literature is also "give me a sip of water, a flower" is finished, but it is our ego that makes us when small offerings are afraid…” (M1-16)

“…we must always maintain a relationship with God, do not live based on selfishness, offer what we have sincerely not because of joining in, or competition that will only become a burden for us in the future. Because we definitely feel calmer when we can make sincere offerings.” (M1-17)

The statement from informant one is confirmed from the verse in Bhagavad Gita 9.26. patraḿ puṣpaḿ phalaḿ toyaḿ yo me bhaktyā prayacchati tad ahaḿ bhakty-upahṛtam aśnāmi prayatātmanaḥ Which means:

“Whoever with devotion offers Me a leaf, a flower, a fruit, a drop of water, I accept this offering with love from a pure-hearted person.”.

Bhagawad Gita 9.26

From the verse that is relevant to the statement of this one informant, we know that God's power is so great, but God's request is very simple. God never demands anything from humans excessively, the important thing is that the offering is from a pure heart, not a dirty heart, not a heart and mind filled with selfishness. This is what the Foundation management always strives to do, namely to make offerings and sacrifices (yadnya) with a sincere heart and always do good and selflessly.

In addition, the Foundation's management also provides sacrifices and dedication as a form of accountability to God. The sacrifices and dedication made by the

Figure 2. Offerings to God in the Ngaben ceremony

Source: balipost.com, 2019

management of this Foundation are carried out by working sincerely, honestly, and comfortably. When the Foundation's management works comfortably and feels that all the sacrifices and dedications made are not a burden, then all the sacrifices and dedications that are made are not hard to do, on the contrary, the management will enjoy and be happy to carry out all the existing work. With a comfortable and happy feeling, it will make the work carried out by the management more optimal, besides that when carrying out sacrifices or yadnya in the form of offerings, the Foundation's administrators will feel happy, calm, and comfortable, so the offering will feel more meaningful.

In addition to God, devotion is also given to others (pawongan accountability). The pawongan element in the Foundation related to its financial management is manifested in the form of good relations with members, supervisors, coaches and the community. As a form of accountability for the management related to financial management, the management carries out an accountability report which is carried out at the end of the year, namely by providing a report at the end of the year meeting, then some are carried out after every activity carried out through the WhatsApp group as evaluation material for the Foundation's management. The annual accountability report is made by the treasurer who is approved by the head of the Foundation, then examined by the Foundation supervisor, and if it has been checked and approved by the supervisor, the accountability report will be approved by the Foundation Trustees. In addition to members, supervisors, and Foundation Trustees, financial reports are also made for service users, but the reporting form is different, namely a memorandum as evidence of approval for the details of the use of funds paid by service users for cremation activities carried out at the SMKS crematorium.

As accountability to others, the SMKS Foundation also contributes economically to the village. The economic contribution given by this Foundation comes from social funds prepared by the Foundation's management which comes from the income of the crematorium unit. The Foundation's budget is prepared for 20% of development costs, 15% of remuneration for management and other workers, and 5% of social funds. This social fund of 5% of income is used to help Bebalang Village, so the greater the income earned by the Foundation from the crematorium unit, the more help that can be given to the community, as stated by the following informants two.

“So far it's still going well. Maybe we can say that in 2021 we have a work program, especially a work program in development and a social work program, because in the distribution of results there are percentages. The first is for the construction of 20%, 15% for the management and 5% for social funds…” (M2-14).

The development funds are used to build the Foundation's facilities so as to provide comfort to the people who come to mourn or use the cremation services of the Foundation. The development funds were also used to help the process of repairing temples, especially the Bebalang Temple. As stated by informant two in the following interview results.

“…like this year, we have done a lot of development programs, such as building genah nyekah, but the system is a lease. Incidentally the head of the foundation who owns this place, he provided the place and we rented it. Second, we installed lights in front of the cremation to make it more beautiful. Well, there is also a resting place for the mourners who come to the crematorium. Incidentally we also make a canteen, from the canteen also provides income for the Foundation. In the future, we will also give the term "punia-punia" to pretending every six months to

temples throughout Bebalang and even outside Bebalang and through social funds we also donate. then to the people in Bebalang we give social donations. In addition, for the biggest temple in Bangli, we have donated.” (M2-14)

The statement from informant two was confirmed by informant five in the following interview results.

“…we from the Foundation donate to the temple in Bebalang, according to the offerings taken. If the offering that is taken is ‘mepebangkit’, then what is offered is the price of a pig, if the 'aplayuan' is below that, the rate is half of the price of the pig. To the temples in Bebalang and outside Bebalang like at the Kehen Temple, at that time the offering of buffalo was worth eighteen million…” (M5-26)

Development funds and social funds have been used properly in accordance with their portions by the Foundation. Such as development funds used to add lighting facilities around the Foundation, build genah nyekah buildings, meperoras, build canteens, and make places for people to rest who come to the Foundation. In addition, social funds have also been used well by the Foundation to provide social donations to the community.

The social assistance provided to the Village is donations or basic necessities for the community in Bebalang Village and also for people outside Bebalang Village, besides that the Foundation also makes donations to temples in Bangli which are carried out every six months and some are carried out once a year. From the activities carried out by the Foundation by leaving its income for the community, it can be interpreted that the orientation of the Foundation is not to obtain high profits, but 'labda', namely how the Foundation feels its presence and benefits for the community, especially in maintaining Balinese customs and culture.

In accountability activities, the SMKS Foundation provides economic contributions to employees as well, one of which is by creating job opportunities for the community around Bebalang Village, then also making economic contributions to employees or work teams at the crematorium, because the success achieved by the Foundation at this time did not escape the efforts and the hard work of the human resources within the Foundation, namely the team of workers in the crematorium unit. So, the Foundation's management must pay attention to the welfare of the crematorium work team, namely by giving bonuses on Galungan and Kuningan Day, besides that the work teams also receive social assistance in the form of basic necessities from the Foundation.

Figure 3. Buffalo donation at Kehen Temple, Bangli

Source: Research Data, 2022

As accountability to crematorium service users, the Foundation contributes to service users with poor community status to be able to carry out the cremation process (ngaben) at the crematorium free of charge with the condition that they attach a certificate of incapacity and a letter from the social service. This requirement is made because the SMKS Foundation stands as a solution and not as a goal. The solution here is that the Hindu community cannot cremation (cremation) because they do not get a grave, so with this Foundation, people can take cremation at the crematorium, and cremation at the crematorium is not the goal of Hindus but, if possible, the community can carry out cremation in the graveyard in the village.

Another assistance provided by the Foundation from the crematorium unit was that for one year the SMKS crematorium was the only crematorium that received bodies that were positive for Covid-19, besides that the community also felt that holding a cremation ceremony (ngaben) at the SMKS crematorium would be more efficient in the use of time, energy and costs without reducing the meaning of the cremation ceremony, even by carrying out the cremation ceremony at the SMKS crematorium, the public will better understand the meaning of the ngaben process for Hindus because they get enlightenment from the sermon given at the cremation event that is not found in the conventional ngaben process, so that service users feel confident and comfortable carrying out the cremation process at the SMKS Foundation.

The comfort felt by service users apart from the service is also due to the beautiful and well-maintained environment around the SMKS Foundation (palemahan accountability). The environment is a place that is close to the existence of human life, besides that the environment also has an important meaning for humans. With the physical environment, humans can use it to meet their material needs. In accountability to the natural environment, it is very necessary to pay attention to the impact that will occur if we carry out an activity in nature. This is a consideration of the management of the SMKS Foundation when they want to open this crematorium unit. So, it was decided that the location of the crematorium building was in the back corner which was quite far from community settlements, because as we know, in the ngaben process, there will be cremation activities so that there will be smoke produced, besides that the sound from the burning equipment is also loud so that by making a crematorium building in the back corner will reduce the impact of discomfort that occurs to the surrounding environment. As the expression of informant three.

“…We also make disposal facilities such as after bathing a corpse there is a special disposal, because after washing a corpse so as not to throw water into the surrounding community, we make a special disposal, to make it cleaner and more comfortable for us. We also carry out the burning process by making the building in the back corner, so that the smoke from the burning does not disturb the surrounding community as well...” (M3-18)

Caring for the environment can also be done by using environmentally friendly facilities, because in addition to not harming the environment, it can also provide comfort for the surrounding community. For example, by making a special disposal site for waste or dirty water so that it does not flow into the settlements of local residents, building a building for burning corpses which is quite far from the residential areas, so that the environment is not polluted and the community does not feel disturbed by all activities carried out at the Foundation. As the statement from informant three.

“…We also have to be responsible for the environment, like in the crematorium, we have made places, for example, the baths have been specially made so as not to pollute the environment, because if we take care of the environment, the environment will also take care of us…” (M3-19)

The statement from informant three was confirmed by informant four in the following interview results.

“…especially for the environment, when we wait for those six hours, we see them cleaning, so it doesn't become a scary place because sometimes we feel that the crematorium is a scary place, but there it's not, good, good accountability, service too…” (M4-23)

In addition to the community around the Foundation, the comfort of service users must also be considered, so it is very important that the Foundation's management pay attention to cleanliness and the facilities provided such as rest areas, canteens, toilets, hand washing facilities and so on. Because the management of the Foundation feels that it is not only an effective implementation that is needed by service users, but a comfortable and clean environment is also a consideration for the community to use the services of a crematorium. So, the management of the Foundation also improved its facilities so that the environment around the crematorium was more beautiful, and clean, and this was successful, because service users felt that the management services and facilities provided were very serious so that service users felt very comfortable carrying out the ngaben ceremony and also chose this SMKS crematorium as a place to carry out the ngaben ceremony many times.

The Foundation's accountability for environmental aspects does not indirectly affect the products it produces, but the management believes that the regulation of environmental aspects will affect the sustainability of the SMKS Foundation, which means it will also affect the growth and development of the SMKS Foundation. With a well-organized environment, from a crematorium that is considered spooky and full of mystique, it will turn into a comfortable place with a variety of positive things, because if we take care of nature then nature will also take care of us, that is a form of human harmony with nature which is mutually related and mutual benefit.

Conclusion

The general description of the themes in the cultural perspective of Tri Hita Karana that has been presented shows that the three informants have the same three themes. From the parahyangan accountability theme carried out by the three informants, it is interpreted as a sincere offering. On the theme of accountability, pawongan carried out by the three informants is interpreted by making economic contributions to the community. On the theme of palemahan accountability carried out by the three informants it is interpreted as protecting the environment. The results of this study can contribute theoretically and practically. Theoretical contributions are related to providing benefits and contributions of new ideas regarding the concept of accountability which are not only seen from the concept of accounting and economics, but can also be seen from the perspective of Balinese culture, namely the Tri Hita Karana culture. In practical contribution, this research can be a reference and contribution for management and stakeholders in carrying out their governance role.

The researcher also realizes that this research still has some limitations and is still not perfect. The limitation in this study is that the development of the Foundation in the

third year, namely for 2021, cannot be disclosed because the annual report is carried out in January 2022 while data collection is carried out in October 2021. Researchers also only use key informants and two supporting informants. Further researchers can add as many external informants as possible who know the organization, especially to support research on the success of the organization, for example starting from the work team, village communities, and village officials. Further research can also use the perspective of the work team in a crematorium business unit or similar organization in its accountability practices using ethnographic methods.

References

Adiputra, I. M. P., Atmadja, A. T., & Saputra, K. A. K. (2014). Culture of Tri Hita Karana as Moderating Effect of Locus of Control on the Performance of Internal Auditor (Studies in the Office of the Provincial Inspectorate in Bali). Research Journal of Finance and Accounting, 5(22), 27–36.

Adiwirya, M., & Sudana, I. (2015). Akuntabilitas, Transparansi, dan Anggaran Berbasis Kinerja Pada Satuan Kerja Perangkat Daerah Kota Denpasar. E-Jurnal Akuntansi, 11(2), 611–628.

Alang, J. A., Sauw, H. M., & Bire, R. (2019). Implementasi Akuntabilitas Penyelenggaraan Organisasi dan Manajemen bagi Koperasi Serba Usaha Tunas Mandiri di Kupang. Jurnal Penelitian Manajemen, 4(1), 19–23.

https://journal.stieken.ac.id/index.php/penataran/article/view/391

Aryasa, P. I., & Musmini, L. S. (2020). Mengungkap Transparansi Dan Akuntabilitas Pengelolaan Keuangan Pada Organisasi Sekaa Suka Duka Bharata Dalam Ranah Kearifan Lokal Menyama Braya. JIMAT (Jurnal Ilmiah Mahasiswa Akuntansi), 11(3), 550–560.

Beckett, R., & Jonker, J. (2002). AccountAbility 1000: a new social standard for building sustainability. Managerial Auditing Journal, 17(1), 36–42.

https://doi.org/10.1108/02686900210412225

Chariri, A. (2009). Landasan filsafat dan metode penelitian kualitatif. Workshop Metodologi Penelitian Kuantitatif Dan Kualitatif, Laboratorium Pengembangan Akuntansi (LPA), Fakultas Ekonomi Universitas Diponegoro Semarang, 31 Juli – 1 Agustus 2009, 1–27.

Creswell, J. W., & Poth, C. N. (2018). Qualitative Inquiry and Research Design: Choosing Among Five Approaches (Fourth Edition). In Angewandte Chemie International Edition, 6(11), 951–952.

Deni, A., Riswanto, A., Tinggi, S., Ekonomi, I., & Sukabumi, P. (2019). Akuntabilitas Dalam Pengelolaan Keuangan Koperasi Perguruan Tinggi (KPT) Mahasiswa. Ejournal Stiedewantara, 115–122.

https://ejournal.stiedewantara.ac.id/index.php/SNEB/issue/view/46

Goddard, A. (2021). Accountability and accounting in the NGO field comprising the UK and Africa – A Bordieusian analysis. Critical Perspectives on Accounting, 1–20.

https://doi.org/10.1016/j.cpa.2020.102200

Gray, R., Bebbington, J., & Collison, D. (2006). NGOs, civil society and accountability: Making the people accountable to capital. Accounting, Auditing and Accountability Journal, 19(3), 319–348. https://doi.org/10.1108/09513570610670325

Gross, M. J., McCarthy, J. H., & Shelmon, N. E. (2012). Financial and Accounting Guide for Not-for-Profit Organizations.

https://books.google.com/books?id=zvVqW1R53YMC&pgis=1

Hanggara, N. ., Atmadja, A. T., & Sinarwati, N. K. (2017). Efisiensi Biaya pada Masing-Masing Paket Upacara Ngaben Di Yayasan Pengayom Umat Hindu (YPUH) Kabupaten Buleleng, Singaraja. E-Journal S1 Ak Universitas Pendidikan Ganesha, 7(1), 5.

Helaluddin. (2018). Mengenal Lebih Dekat dengan Pendekatan Fenomenologi: Sebuah Penelitian Kualitatif. Uin Maulana Malik Ibrahim Malang, 1–15.

Hidayat, A. A. (2007). Metode Penelitian Keperawatan dan teknik Analisa Data. Selemba Medika.

Jayasinghe, K., & Soobaroyen, T. (2009). Religious “spirit” and peoples’ perceptions of accountability in Hindu and Buddhist religious organizations. Accounting, Auditing & Accountability Journal, 22(7), 997–1028.

https://doi.org/10.1108/09513570910987358

Kaban, & Luther. (2010). Transparansi dan Akuntabilitas Keuangan GBKP. Https://Gbkp.or.Id.

Kamaruddin, M. I. H., & Ramli, N. M. (2018). the Impacts of Internal Control Practices on Financial Accountability in Islamic Non-Profit Organizations in Malaysia. International Journal of Economics, Management and Accounting, 26(2), 365–391.

Kepramareni, P., Sudarma, M., Irianto, G., & Rahman, A. F. (2014). Sekala and Niskala accountability practices in the clan-based organization MGPSSR in Bali, Indonesia. Scientific Research Journal (SCIRJ), 2(2), 1–5. www.scirj.org

Komalasari, Y., Wirajaya, I. G. A., & Ratna Sari, M. M. (2019). Akuntabilitas Akuntan Perempuan-Karir Bali: Sebuah Studi Fenomenologi. Jurnal Ilmiah Akuntansi Dan Bisnis, 14(1), 70–85. https://doi.org/10.24843/jiab.2019.v14.i01.p07

Kumalawati, D. D., & Atmadja, A. T. (2020). Analisis Akuntabilitas Pengelolaan Iuran Dana Patis (Studi Kasus Pada Desa Adat Cau). JIMAT (Jurnal Ilmiah …, 11(2), 77–88. https://ejournal.undiksha.ac.id/index.php/S1ak/article/view/24959

Manguma, V., Randa, F., & Palalangan, C. A. (2020). Mengungkap Praktik Akuntabilitas Dalam Organisasi Gereja Toraja Jemaat Tallunglipu. Jurnal Ilmiah Akuntansi Dan Bisnis, 4(2), 165–173. https://doi.org/10.38043/jiab.v4i2.2328

Massud, M. E. I., & Aktar, A. (2020). Beneficiary Accountability of NGOs : A Case Study on a Women Empowerment Based Advocacy NGO. The Cost and Management, 48(02), 41–53.

Muttakin, M. B., Khan, A., & Azim, M. I. (2015). Corporate social responsibility disclosures and earnings quality: Are they a reflection of managers’ opportunistic behavior? Managerial Auditing Journal, 30(3), 277–298. https://doi.org/10.1108/MAJ-02-2014-0997

Pandeni, K. R. (2017). Pengaruh Budaya Organisasi, Akuntabilitas Publik, Dan Pengendalian Intern Terhadap Kinerja Organisasi Dengan Total Quality Management Sebagai Variabel Moderating Pada Pdam Kabupaten Buleleng. JIMAT (Jurnal Ilmiah Mahasiswa Akuntansi S1), 7(1).

Paranoan, S. (2015). Akuntabilitas dalam Upacara Adat Pemakaman. Jurnal Akuntansi Multiparadigma, 6(2), 214–223. https://doi.org/10.18202/jamal.2015.08.6017

Randa, F., & Daromes, F. E. (2015). Akuntabilitas Organisasi Sektor Publik. JKAP (Jurnal Kebijakan Dan Administrasi Publik), 19(1), 477–484.

https://doi.org/10.22146/jkap.7523

Randa, F., Triyuwono, I., Ludigdo, U., & Sukoharsono, E. G. (2011). Studi Etnografi Akuntabilitas Spiritual Pada Organisasi Gereja Katolik Yang Terinkulturasi Budaya

LokaLas Spiritual.pdf. Jurnal Akuntansi Multiparadigma, 2(1), 35–51.

Riskiyadi, M., Tarjo, & Anggono, A. (2022). Uncovering Tax Avoidance at Government Agencies : A Phenomenological Research. Jurnal Ilmiah Akuntansi Dan Bisnis, 17(1), 22–32. https://doi.org/10.24843/JIAB.2022.v17.i01.p02

Riyanti. (2020). Dekonstruksi Akuntabilitas Konvensional : Sebuah Kritik Yang Dibangun Dari Akuntabilitas Masjid. Doctoral dissertation, Universitas Hasanuddin.

Rodliyah, S., Djamhuri, A., & Prihatiningtias, Y. W. (2021). Revealing The Accountability of Nurul Haromain Islamic Boarding Schools: A Phenomenological Study. Jurnal Ilmiah Akuntansi Dan Bisnis, 16(2), 359–372.

https://doi.org/10.24843/jiab.2021.v16.i02.p12

Saputra, P. B. A., Sutapa, I. N., & Kurniawan, K. A. (2018). Akuntabilitas Pengelolaan Keuangan Desa Dalam Perspektif Budaya Tri Hita Karana. Jurnal Riset Akuntansi Dan Bisnis Airlangga, 3(1). https://doi.org/10.31093/jraba.v3i1.90

Sari, D. M. M. Y., & Sudana, I. P. (2020). Managerial Accountability of Badan Usaha Milik Desa Wija Sari in Samsam Village: A Case Study Research. Jurnal Ilmiah Akuntansi Dan Bisnis, 15(2), 152. https://doi.org/10.24843/jiab.2020.v15.i02.p02

Sayuti, S., Majid, J., & Juardi, M. S. S. (2018). Perwujudan Nilai Transparansi, Akuntabilitas dan Konsep Value For Money dalam Pengelolaan Akuntansi Keuangan Sektor Publik (Studi Pada Kantor BAPPEDA Sulawesi Selatan). ATESTASI : Jurnal Ilmiah Akuntansi, 1(1), 16–28. https://doi.org/10.33096/atestasi.v1i1.39

Scobie, M., Lee, B., & Smyth, S. (2020). Grounded accountability and Indigenous selfdetermination. Critical Perspectives on Accounting.

https://doi.org/10.1016/j.cpa.2020.102198

Silvia, J., Mahasiswa, N. I. M. C., & Ansar, M. (2011). (Studi Fenomenologis Pada Gereja Protestan Indonesia Donggala Jemaat Manunggal Palu) Fakultas Ekonomi Universitas Syiah Kuala Banda Aceh , 21-22 Juli 2011 Fakultas Ekonomi Universitas Syiah Kuala Banda Aceh , 21-22 Juli 2011. Simposium Nasional Akuntansi XIV, 1–25.

Smith, J. A., Flowers, P., & Larkin, M. (2009). Interpretative Phenomenological Analysis: Theory, Method and Research. January, 232.

http://books.google.com/books?id=WZ2Dqb42exQC&pgis=1

Sugiyono. (2011). Metode Penelitian Kuantitatif, Kualitatif dan R&D. Alfabeta.

Sujana, I. K., Dwirandra, A. A. N. B., Putri, I. G. A. M. A. D., & Suardikha, I. M. S. (2015). Akuntabilitas dalam Perspektif Budaya Lokal pada Lembaga Perkreditan Desa ( LPD ). Laporan Penelitian Unggulan Program Magister Akuntansi Fakultas Ekonomi Dan Bisnis Universitas Udayana, 1–69.

Triyuwono, I. (2011). ANGELS: Sistem Penilaian Tingkat Kesehatan (TKS) Bank Syari’ah.

Jurnal Akuntansi Multiparadigma, 2(1), 1–21.

https://doi.org/10.18202/jamal.2011.04.7107

Vidyantari, P. K., Sudana, I. P., Wirajaya, I. G. A., & Suprasto, H. B. (2022). Work Cultural-Life Balance : A Phenomenological Study of Balinese Female Accountant in the Banking Sector. Jurnal Ilmiah Akuntansi Dan Bisnis, 17(1), 50–65.

https://doi.org/10.24843/JIAB.2022.v17.i01.p04

Wardana, I. W., & Putra, K. D. (2012). Tri Hita Karana Tourism Awards & Accreditation. Yayasan Tri Hita Karana Bali.

Wati, N. L. Y., Atmadja, A. T., & Herawati, N. T. (2017). Transparansi dan Akuntabilitas Pengelolaan Dana Air Desa Sebagai Pendapatan Tambahan pada Pura Desa Banyuning. Jurnal Ilmiah Mahasiswa Akuntansi, 7(1).

Wijaya, G. D., Ayu, G., Rencana, K., Dewi, S., Prayudi, M. A., & Ganesha, U. P. (2020). Analisis Akuntabilitas dan Transparansi Program Buda Wage Kelawu Dusun Kawanan Desa Sawan. JIMAT (Jurnal Ilmiah Mahasiswa Akuntansi), 11(1), 101–113.

Wirajaya, G. A., Sudarma, M., Ludigdo, U., & Djamhuri, A. (2014). The Accountability in the Dimension of TRI HITA Karana (THK) An Ethnographic Study on the Organization of Kuta Traditional Vilage. Scientific Research Journal Issue VIII, 2(8), 10–17. www.scirj.org

Yasmin, S., Ghafran, C., & Haslam, J. (2021). Centre-staging beneficiaries in charity accountability: Insights from an Islamic post-secular perspective. Critical

Perspectives on Accounting, 75(January 2021), 1–29.

https://doi.org/10.1016/j.cpa.2020.102167

Jurnal Ilmiah Akuntansi dan Bisnis, 2022 | 312

Discussion and feedback