The Moderation Effect of Religiosity on The Effect of Moral Equity to Auditor Ethical Behavior

on

Jurnal Ilmiah Akuntansi dan Bisnis

Vol. 16 No. 2, July 2021

AFFILIATION:

1,2Faculty of Economics and Business, Universitas Airlangga, Indonesia

*CORRESPONDENCE:

THIS ARTICLE IS AVAILABLE IN:

DOI:

10.24843/JIAB.2021.v16.i02.p10

CITATION:

Balqis, A. & Fanani, Z. (2021) The Moderating Effect of Religiosity on Moral Equity and Auditor Ethical Behavior. Jurnal Ilmiah Akuntansi dan Bisnis, 16(2), 332-342.

ARTICLE HISTORY

Received:

14 June 2020

Revised:

11 September 2020

Accepted:

10 October 2020

The Moderating Effect of Religiosity on Moral Equity and Auditor Ethical Behavior

Anastania Balqis1, Zaenal Fanani2*

Abstract

This study obtains information and empirical evidence on the moderating effect of religiosity on moral equity and auditor ethical behavior. It was conducted in public accountants in East Java using primary data to obtain vital information from respondents using the purposive sampling method. The study respondents were 102 auditors who work at the public accountant in East Java. Moderated regression analysis was applied as an analysis technique. These hypotheses were tested using WarpPLS 5.0 software. The results indicated that religiosity is proven to have a significant positive effect on the moral equity of auditor ethical behavior. This finding can be useful to help auditors understand that there are several factors that influence and strengthen ethical behavior.

Keywords: auditor, ethical behavior, moral equity, religiosity

Introduction

Ethics is the foundation of every responsible society (Adekoya et al., 2020). Globally, the continued decline in ethical values in organizations and society has increased awareness of ethical studies (Oboh, 2019; Oboh & Ajibolade, 2018; Pielke Jr, 2016). In recent years the call for ethics in business and accounting practice has been strengthened after occurred fraud in several Public Accounting Firms (PAK) (Adekoya et al., 2020).

One of the cases fraud that had occurred among auditors was the case of PT Sunprima Nusantara Financing (SNF) Finance. The Financial Services Authority (OJK) imposed administrative sanctions on two Public accountants and one Public Accounting Firm (PAK) because they were deemed not to provide an opinion that was in accordance with the actual conditions in the annual audited financial report of PT SNF Finance. Both PAs and one PAK provide “Unqualified” opinion in the audit results of SNF annual financial statements Finance's. Even though the results of the OJK examination indicate that SNF Finance presents significant financial reports that are not in accordance with the actual financial conditions. Thus causing losses to many parties, including banks.

The purpose of auditors quoted from ISA 240 is to identify and

assess the risk of material misstatement in the Financial Statements caused by fraud (Tuanakotta, 2015), so that many companies believe that Independent Auditors have a greater responsibility and sensibility to detect and report fraud and / or misinformation in financial statements (Porter, 1996). Therefore, awareness is needed from within the auditor in carrying out his responsibilities and fulfilling his goals (Adekoya et al., 2020).

Along with the emergence of awareness of the importance of auditors' moral and ethical behavior, research on ethical behavior in accounting and the factors that influence ethical behavior is needed (Kashif et al., 2017). In general, there are two categories of factors that influence ethical decision behavior, namely individual factors and situational factors (Mischel, 1977). Individual factors can be interpreted as something that is inherent in the person physiologically. While situational factors are factors that arise from outside the individual. Mentioned in Theory of Planned Behavior, there are 3 (three) main constructs that shape a behavior, namely attitude, subjective norms, and perceived behavior control (I. Ajzen, 1991). Dimension is Subjective norms represented by 5 variables (Reidenbach & Robin, 1990). Of the five variables, one of them is moral equity.

Moral equity refers to actions taken based on Aristotle's principles of justice in treating something as equals (Reidenbach & Robin, 1988). Moral equity is a broad-based dimension that can be considered part of the Theory of Justice (John, 1971), and refers to an individual's perception of justice and what is right and wrong in a broad sense (Nguyen & Biderman, 2008). Moral equity has been found to be related to ethical behavior intentions in certain situations (Nguyen & Biderman, 2008).

Research conducted by (Arli & Tjiptono, 2014; Forsyth & Scott, 1984) has shown that higher levels of moral judgment lead to higher ethical behavior. When explaining auditor behavior, Rest (1986) suggests a theoretical model that specifies that an individual must recognize moral issues, make moral judgments, commit to placing moral concerns and then act on moral issues. Each individual will initially assess whether the case is fraud considered a moral problem or vice versa (Arli & Tjiptono, 2014). This in turn affects their moral judgment and consequently their behavior.

Individual moral equity is not an absolute thing that can lead people to behave well, it requires other factors as factors that strengthen moral equity. Kashif et al. (2017) stated that the latest study discusses the need to expand the scope of construction in consideration of ethical decision-making research by adding social influences. One of the most attractive socio-cultural value systems that has ever been proposed as relevant to ethical behavior in the workplace is religiosity (Hunt & Vitell, 1986; Singhapakdi et al., 2013).

The increasing religiosity of people around the world has prompted researchers to learn how this religiosity can influence ethical behavior (Tariq et al., 2019). Religiosity is a term used to denote many aspects of the influence of religion on the behavior and mindset of the observer (Singhapakdi et al., 2013). Therefore, religiosity is the most complex human trait because it acts as intrinsic and extrinsic to a behavior (Kashif et al., 2017). Intrinsic religiosity is an inner spirit that is reflected in a person's dominant motivation. This shows a commitment to the principles inherent in religion and involvement in serving religion (Singhapakdi et al., 2013; Tariq et al., 2019). Extrinsic religiosity shows the use of religion as a motivation for personal gain (Singhapakdi et al., 2013; Tariq et al., 2019). It is said that religious practice strengthens faith, that faith helps people maintain moral standards and high individual levels of morality create an

overall ethical social setting (Winchester, 2008) Religiosity has been found to be a factor for ethical behavior for a person (Singhapakdi et al., 2013).

The first motivation for this study is to add religiosity as a factor to test whether religiosity can be a reinforcing factor for moral equity or not, because religiosity is a religious understanding of individuals based on experience and awareness (Kashif et al., 2017). Religiosity comes from within oneself, the inner experience that is felt and is not formed from external factors (Singhapakdi et al., 2013). So that the religiosity must be combined with other factors to find out how religiosity will make individuals better at accepting everything they get (Johnson & Morris, 2008). Therefore, with religiosity, it will further increase awareness that what an individual receives is actually based on a correct assessment so that what they get is in accordance with what they do (Li & Chen, 2016).

A research with religiosity as a moderating variable has been conducted by Kashif et al. (2017), Lau et al. (2013), and Johnson & Morris (2008). Kashif et al. (2017) in their research showed that the elements in Theory of Planned Behavior (TPB) were felt in behavioral intentions and were moderated by religiosity. Likewise, with the research of Lau et al. (2013) and Johnson & Morris (2008) which give results that religiosity intrinsically and extrinsically moderates the influence between money ethics and tax evasion and provides support for general strain theory which has a direct positive effect on delinquency.

The next research motivation is to make a difference with the research of Kashif et al. (2017), Lau et al. (2013), and Johnson & Morris (2008) using moral equity as the independent variable and ethical behavior as the dependent variable. This study aims to add to the literature on religiosity as a moderating variable that focuses on Indonesia as an Asian Muslim country. Religion is one of the most influential value systems because it provides billions of individuals around the world, not only with the code by which they live their lives, but also with social identities (Ysseldyk et al., 2010).

This research refers to the Theory of Planned Behavior which is based on an approach to beliefs that can encourage individuals to perform certain behaviors (I. Ajzen, 2005). According to I. Ajzen (1991), the main factor in the realization of behavior comes from the individual's intention (behavior intention). The intention to realize a behavior is influenced by three components of attitude, subjective norms and perceived behavioral control. A person can have various kinds of beliefs about a behavior, but only a few beliefs can influence behavior when faced with a certain event (I. Ajzen, 1991).

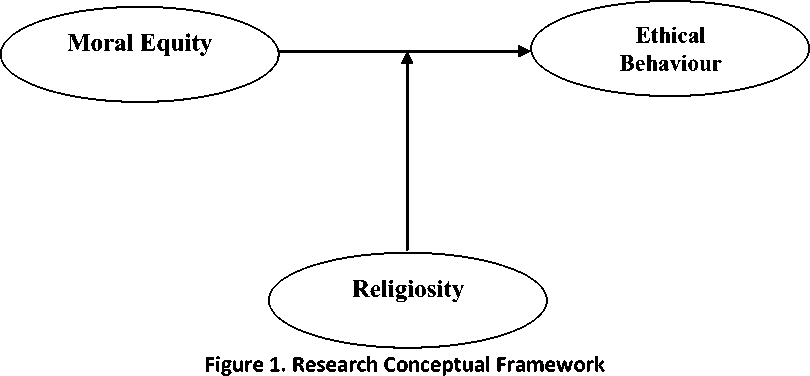

This research proposes the incorporation of religiosity as an element moderating construction effects Theory of Planned Behavior that exist on the intentions of ethical behavior. This section can be explained through a conceptual framework as shown in Figure 1.

In Theory of Planned Behavior, it is said that human behavior is under control and there is no barrier that can trigger the intention to behave in a certain way (I. Ajzen, 1985). (H. Ajzen & Fishbein, 1980) said that there are 2 things that trigger behavioral intentions, namely attitudes and norms. Norms can be seen through the moral values of an individual which will have different characteristics, this is called moral equality or moral equity. Moral equality reflects justice. The more an individual understands moral values, the easier it will be to behave fairly (Arli & Tjiptono, 2014).

Moral equity has been found to be associated with ethical behavior intentions in certain situations (Nguyen & Biderman, 2008). Nguyen & Biderman (2008) examined the behavior of retail sales and car repair in an experiment. The result found that moral equity is related to ethical behavior intention. Leonard et al. (2017) assessing individual and group situations in an academic environment, these conditions are used to assess how a student's sense of fairness affects behavioral intentions in the situation and the results are moral equity related to ethical behavior. Based on the existing explanation, the hypotheses built in the study are:

-

H1: The higher the moral equity, the better the ethical behavior.

-

H. Ajzen and Fishbein (1980) said that there are 2 things that trigger behavioral intentions, namely attitudes and norms. The Theory of Planned Behavior states also that human behavior is under control and there is no barrier that can trigger the intention to behave in a certain way. Norms can be seen through the moral value of an individual which will have different characteristics, this is called moral equality or moral equity. Moral equity reflects fairness. The more an individual understands moral values, the easier it will be to behave fairly (Arli & Tjiptono, 2014).

In a study conducted by Baumeister et al. (2007), it has been found that behavior is influenced by people's orientation towards religious beliefs which in turn affects their ethical intentions. Religiosity is also related to the degree of perceived behavioral control shown by people in both social and organizational settings (Cherry, 2006; Cohen et al., 2012; Vitell et al., 2009). Another study conducted by Walker et al. (2012), employees who score high on religiosity tend to show better behavior control. The converse has also been shown to be true: people who show higher levels of behavioral control are more likely to be influenced by religious teachings and practices (Welch et al., 2006). Based on existing explanations, the hypotheses built in this study are:

H2: Religiosity can strengthen the relationship between moral equity and ethical behavior.

Research Method

This research is a quantitative study using primary data. The primary data is in the form of a questionnaire distributed to auditors in 64 PAKs located in East Java. This

questionnaire contains questions related to moral equity, religiosity, and ethical behavior. To determine the sample, researchers used a purposive sampling technique. Based on the calculation results, the minimum sample size in this study is 100 respondents. Furthermore, the questionnaire was distributed to 150 auditors in 64 PAK, but with consideration of feasibility and consistency of answers, this study used 102 questionnaires as a sample.

This questionnaire method is implemented by providing a list of written statements to the respondents (research sample). Then the respondent answers the statement by choosing the alternative answers that have been provided. A list of statements addressed to auditors in Public accounting firms (PAK) located in East Java.

The data analysis technique used in this study is the test moderated regression analysis. The test is moderated regression analysis used to measure the strength of the influence between two or more independent variables on one dependent variable and is used to predict the relationship between the dependent variable and the independent variable.

This research consists of three variables, namely moral equity as the independent variable, religiosity as a moderating variable, and ethical behavior as the dependent variable. Moral equity is all generally accepted moral philosophy that represents an effort to develop a fair approach in moral relations with others (Robin, 2020). This variable is measured using a Likert scale 1-7 with 4 (four) indicators adopted from the study (Leonard et al., 2017).

The next variable is religiosity which is defined as a belief in God with a commitment to follow the principles set by God (McDaniel & Burnett, 1990). This variable is measured using a 1-7 Likert scale with 5 statement instruments developed by Kashif et al. (2017).

The last variable, namely ethical behavior, is behavior that is in accordance with the beliefs of each individual and social norms about what is right and good (Kashif et al., 2017). Ethical behavior consists of 5 (five) statements adopted from research by Kelley et al. (1990).

Result and Discussion

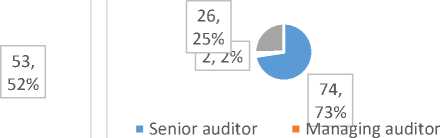

Research respondents were the auditors of the Public Accounting Firm in East Java with a total of 102 auditors. The following will explain the distribution based on age, gender and position of the respondents.

20, 20%

Age

Gender

Position

82, 80%

49, 48%

■ Male ■ Female

■ Junior auditor

Figure 2. Respondent Characteristics

Source: Processed Data, 2020

|

Table 1. Religiosity Indicators | |||

|

Variable |

Indicator |

Outer Loading Value |

Conclusion |

|

EM1 |

0.693 |

Significant | |

|

Moral Equity |

EM2 EM3 |

0.843 0.729 |

Significant Significant |

|

EM4 |

0.697 |

Significant | |

|

PE 1 |

0.020 |

Not Significant | |

|

PE 2 |

0.748 |

Significant | |

|

Ethical Behavior |

PE 3 |

0.706 |

Significant |

|

PE 4 |

0.599 |

Significant | |

|

PE 5 |

0.628 |

Significant | |

|

RG1 |

0.651 |

Significant | |

|

RG2 |

0.728 |

Significant | |

|

Religiosity |

RG3 |

0.563 |

Significant |

|

RG4 |

0.620 |

Significant | |

|

RG5 |

0.734 |

Significant | |

Source: Processed Data, 2020

Based on Figure 2., most auditors have an age range of less than 30 years with a total of 82 people or 80.39% of the total respondents, while the lowest respondents have an age above 30 years with a total of 20 people or 19.61% of the total respondents. The majority of respondents have an age range of 30-40 years, so it can be said that auditors at KAP East Java are in the productive age range.

Based on Figure 2., most of the auditors were male with a total of 53 people or 51.96% of the total respondents. And based on Figure 2., most of the respondents had positions as auditors as many as 74 people or 72.55% of the total respondents, while the lowest was the implementing auditor with 2 people or 1.96% of the total respondents.

Measurement of the outer model in this study was carried out by measuring the reflection of the indicator which was assessed based on the correlation between item score/component score the estimated and the outer loading factor value. The minimum limit of the outer loading factor value of an indicator that is suitable for reflecting a variable is 0.5 (Chin, 1998).

Based on the results of statistical data processing using the help of software WarpPLS version 5.0 to calculate the value of the outer loading factor, the first iteration results are obtained. The following table describes the reflective value of the indicator Table 2. Estimated Final Iteration Outer Loading Factor

Variable Indicator Outer Loading Value Conclusion

|

EM1 |

0.693 |

Significant | |

|

Moral Equity |

EM2 EM3 |

0.843 0.729 |

Significant Significant |

|

EM4 |

0.697 |

Significant | |

|

PE2 |

0.824 |

Significant | |

|

Ethical Behaviour |

PE3 |

0.820 |

Significant |

|

PE5 |

0.521 |

Significant | |

|

RG1 |

0.759 |

Significant | |

|

Religiosity |

RG2 |

0.791 |

Significant |

|

RG5 |

0.779 |

Significant | |

Source: Processed Data, 2020

Table 3. Discriminant Validity Test

|

Variable |

Average Variance Extracted (AVE) |

|

Moral Equity |

0,552 |

|

Ethical Behavior |

0,541 |

|

Religiosity |

0,603 |

Source: Processed Data, 2020

for each variable. Table 3. illustrates the reflective value of the indicator for each variable.

Indicators that have an outer loading factor value below 0.5 are assumed to be not suitable to be used as indicators that can reflect each of the corresponding variables (Hult et al., 2018; Solihin & Ratmono, 2014). To get optimal results, the indicators that cannot reflect the predetermined variables will be eliminated and will be recalculated on the value of the outer loading factor.

After a single recalculation process is carried out, indicators are obtained that can reflect all variables. Table 2. illustrates the reflective value of the indicator for each variable. Based on the results in Table 2., all indicators have an value outer loading factor greater than 0.5. Therefore, it can be concluded that all indicators are appropriate to reflect each of the related variables.

Each variable was tested for validity by using discriminant validity. This test is measured by comparing the square root Average Variance Extracted (AVE) value of each construct with the correlation between other constructs in the model. AVE value must be greater than 0.50 or have a p-value smaller than the significance level (0.05). The results of measuring discriminant validity in this study can be seen in Table 5.

Based on the results in Table 3., all variables have values discriminant validity above 0.50. These results indicate that all variables are declared valid and can be used in the analysis process. After the variables have been declared valid, then the reliability test is carried out on all variables used in this study. Variable reliability was tested using techniques composite reliability.

To determine whether a measuring instrument is reliable or not, the reliability coefficient is used. The reliability coefficient must be greater than 0.70 (Fraenkel et al., 1993). The results of measuring composite reliability can be seen in Table 4.

Based on the results presented in Table 4., all variables have a value composite reliability above 0.70. These results indicate that all variables are declared reliable and reliable for use in the further analysis process.

Before testing the hypothesis to see the effect between variables, the fit model test is first carried out. The fit model test aims to determine whether the model built in the study is fit with the original data, so that it can determine the quality of the model (Vinzi et al., 2010). This study uses five fit model measures, including Average Path coefficient (APV), Average R-Square (ARS), Average adjusted R-Square (AARS), Average block VIF (AVIF), Average full collinearity VIF (AFVIF). The results of the fit model test are

Table 4. Composite Reliability Test

|

Variable |

Composite Reliability |

|

Moral Equity |

0.830 |

|

Ethical Behavior |

0.773 |

|

Religiosity |

0.820 |

Source: Processed Data, 2020

Table 5. Model Fit Test

Fit Model Measures Value

AVIF 1,646 ; Acceptable if < 0,05

AFVIF 1,045 ; Acceptable if < 0,05

Source: Processed Data, 2020

presented in Table 5.

Based on the results of data processing in Table 5., it shows that the model in this study is declared fit. APC, ARS, and AARS have p-values less than 0.05. AVIF value <3.3 indicates that there is no problem multicollinearity between the indicators and variables used.

The direct effect test aims to determine the moderating effect of religiosity on the effect of moral equity on ethical behavior. The direct effect test was carried out using the test t-statistic in the analysis model partial least squared (PLS)using the help of the software WarpPLS 5.0.

The moderating effect of religiosity on the effect of moral equity on ethical behavior shows a path coefficient value of 0.149 and p-value <0.001. These results indicate that moral equity has a significant effect on ethical behavior because the p-value is <0.05.

Based on the results of hypothesis testing, it can be concluded that moral equity has a positive and significant effect on ethical behavior. This can be seen in Table 8. that p-values of <0.05. It can be concluded that hypothesis 1 (one) has a positive effect and is proven to be significant. These results are in line with research conducted by Leonard et al. (2017) that moral equity was found to influence behavioral intention.

The results of this test support the model of Reidenbach & Robin (1990), it is said that there are many factors that can shape a person's ethical behavior. One of them is moral equity. When explaining ethical behavior, Rest (1986) suggests a theoretical model that stipulates that an individual must recognize moral problems, make moral judgments, resolve to place moral concerns and act on moral issues. This in turn affects their moral judgment and consequently their behavior.

Based on the results of hypothesis testing in Table 6., it can be concluded that religiosity is able to strengthen the relationship between moral equity and ethical behavior. So that hypothesis 2 (two) has a positive effect and is proven significant. This is in line with research from Kashif et al. (2017).

Vitell et al. (2009) argue that belief in Almighty God and devotion to religious principles not only help build a moral identity and provide a way of life, but also act as a basis for socialization and a source of strength and courage to defend what is believed regardless of consequences. Therefore, this study can show that religiosity can strengthen the relationship between moral norms and acceptable ethical behavior in a

Table 6. Hypothesis Testing

|

Variable |

Path-Coefficient (Model 1) β Sig |

|

Moral Equity Adjusted R-Square |

0,192 ; p < 0,05 0,149 ; p < 0,001 |

Source: Processed Data, 2020

country like Indonesia where religion is openly practiced in social and even occupational rules.

Conclusion

Based on the results of the tests that have been done, it can be concluded that: 1) moral equity has a positive effect on the ethical behavior of an auditor, 2) religiosity is able to moderate the relationship between moral equity and ethical behavior. This study produces findings that can be useful for an auditor to be able to understand that there are individual and situational factors, in this study, namely moral equity and religiosity, which can influence and strengthen a person's ethical behavior.

This study uses data in the form of statements submitted in the research questionnaire. The research questionnaire is hypothetical because the nature of ethical research is sensitive and the respondents are in an unreal condition when making decisions. It is likely that when respondents are faced with an actual situation they will act in different ways.

This study examines one individual factor that can influence ethical behavior. Thus there may be other individual factors that can influence ethical behavior. So it is hoped that further research can use a wider range of factors so that the results obtained can add to the study of literature in this field.

References

Adekoya, A. C., Oboh, C. S., & Oyewumi, O. R. (2020). Accountants perception of the factors influencing auditors' ethical behaviour in Nigeria. Heliyon, 6(6), 1-8. https://doi.org/10.1016/j.heliyon.2020.e04271

Ajzen, H., & Fishbein, M. (1980). Understanding attitudes and predicting social behavior. Prentice-Hall.

Ajzen, I. (1985). From intentions to actions: A theory of planned behavior Action control (pp. 11-39): Springer. https://doi.org/10.1007/978-3-642-69746-3_2

Ajzen, I. (1991). The theory of planned behavior. Organizational behavior and human decision processes, 50(2), 179-211. https://doi.org/10.1016/0749-5978(91)90020-T

Ajzen, I. (2005). Attitudes, personality, and behavior: McGraw-Hill Education (UK).

Arli, D., & Tjiptono, F. (2014). The end of religion? Examining the role of religiousness, materialism, and long-term orientation on consumer ethics in Indonesia. Journal of Business Ethics, 123(3), 385-400. https://doi.org/10.1007/s10551-013-1846-4

Baumeister, R. F., Vohs, K. D., & Tice, D. M. (2007). The strength model of self-control. Current directions in psychological science, 16(6), 351-355.

https://doi.org/10.1111/j.1467-8721.2007.00534.x

Cherry, J. (2006). The impact of normative influence and locus of control on ethical judgments and intentions: A cross-cultural comparison. Journal of Business Ethics, 68(2), 113-132. https://doi.org/10.1007/s10551-006-9043-3

Chin, W. W. J. M. m. f. b. r. (1998). The partial least squares approach to structural equation modeling. 295(2), 295-336.

Cohen, J., Ding, Y., Lesage, C., & Stolowy, H. (2012). Corporate fraud and managers’ behavior: Evidence from the press Entrepreneurship, governance and ethics (pp. 271-315): Springer. https://doi.org/10.1007/978-94-007-2926-1_8

Forsyth, D. R., & Scott, W. L. (1984). Attributions and moral judgments: Kohlberg’s stage theory as a taxonomy of moral attributions. Bulletin of the Psychonomic Society, 22(4), 321-323. https://doi.org/10.3758/BF03333831

Fraenkel, J. R., Wallen, N. E., & Hyun, H. H. (1993). How to design and evaluate research in education (Vol. 7): McGraw-Hill New York.

Hult, G. T. M., Hair Jr, J. F., Proksch, D., Sarstedt, M., Pinkwart, A., & Ringle, C. M. (2018). Addressing endogeneity in international marketing applications of partial least squares structural equation modeling. Journal of International Marketing, 26(3), 1-21. https://doi.org/10.1509/jim.17.0151

Hunt, S. D., & Vitell, S. (1986). A general theory of marketing ethics. Journal of macromarketing, 6(1), 5-16. https://doi.org/10.1177/027614678600600103

John, R. (1971). A theory of justice. Cambridge, MA: p, University.

Johnson, M. C., & Morris, R. G. (2008). The moderating effects of religiosity on the relationship between stressful life events and delinquent behavior. Journal of Criminal Justice, 36(6), 486-493. https://doi.org/10.1016/j.jcrimjus.2008.09.001

Kashif, M., Zarkada, A., & Thurasamy, R. (2017). The moderating effect of religiosity on ethical behavioural intentions: An application of the extended theory of planned behaviour to Pakistani bank employees. Personnel Review, 46(2), 429448. https://doi.org/10.1108/PR-10-2015-0256

Kelley, S. W., Ferrell, O., & Skinner, S. J. (1990). Ethical behavior among marketing researchers: An assessment of selected demographic characteristics. Journal of Business Ethics, 9(8), 681-688. https://doi.org/10.1007/BF00383395

Lau, T.-C., Choe, K.-L., & Tan, L.-P. (2013). The moderating effect of religiosity in the relationship between money ethics and tax evasion. Asian Social Science, 9(11), 213. https://doi.org/10.5539/ass.v9n11p213

Leonard, L. N., Riemenschneider, C. K., & Manly, T. S. (2017). Ethical behavioral intention in an academic setting: Models and predictors. Journal of Academic Ethics, 15(2), 141-166. https://doi.org/10.1007/s10805-017-9273-2

Li, F., & Chen, H. (2016). Perceived ethicality of moral choice: The impact of ethics codes, moral development, and relativism. Nankai Business Review International, 7(2), 258-279. https://doi.org/10.1108/NBRI-12-2015-0032

McDaniel, S. W., & Burnett, J. J. (1990). Consumer religiosity and retail store evaluative criteria. Journal of the Academy of marketing Science, 18(2), 101-112. https://doi.org/10.1007/BF02726426

Mischel, W. (1977). On the future of personality measurement. American psychologist, 32(4), 246. https://doi.org/10.1037/0003-066X.32.4.246

Nguyen, N. T., & Biderman, M. D. (2008). Studying ethical judgments and behavioral intentions using structural equations: Evidence from the multidimensional ethics scale. Journal of Business Ethics, 83(4), 627. https://doi.org/10.1007/s10551-007-9644-5

Oboh, C. S. (2019). Personal and moral intensity determinants of ethical decisionmaking. Journal of Accounting in Emerging Economies, 9(1), 148180. https://doi.org/10.1108/JAEE-04-2018-0035

Oboh, C. S., & Ajibolade, S. O. (2018). Personal characteristics and ethical decisionmaking process of accounting professionals in Nigeria. Crawford J. Busines. Soc. Sci, 8(1), 1-23.

Pielke Jr, R. (2016). Obstacles to accountability in international sports governance.

Global Corruption Report: Sport, Transparency International, Routledge, London and New York, 29-38.

Porter, B. A. (1996). A research study on financial reporting and auditing--bridging the expectation gap. Accounting Horizons, 10(1), 130.

Reidenbach, R. E., & Robin, D. P. (1988). Some initial steps toward improving the measurement of ethical evaluations of marketing activities. Journal of Business Ethics, 7(11), 871-879. https://doi.org/10.1007/BF00383050

Reidenbach, R. E., & Robin, D. P. (1990). Toward the development of a multidimensional scale for improving evaluations of business ethics. Journal of Business Ethics, 9(8), 639-653. https://doi.org/10.1007/BF00383391

Rest, J. R. (1986). Moral development: Advances in research and theory. New York: Praeger

Singhapakdi, A., Vitell, S. J., Lee, D.-J., Nisius, A. M., & Grace, B. Y. (2013). The influence of love of money and religiosity on ethical decision-making in marketing. Journal of Business Ethics, 114(1), 183-191. https://doi.org/10.1007/s10551-012-1334-2

Solihin, M., & Ratmono, D. (2014). Analisis SEM-PLS dengan WarpPLS 3.0 untuk hubungan non-linear untuk penelitian sosial dan bisnis. Yogyakarta: Andi Publisher.

Tariq, S., Ansari, N. G., & Alvi, T. H. (2019). The impact of intrinsic and extrinsic religiosity on ethical decision-making in management in a non-Western and highly religious country. Asian Journal of Business Ethics, 8(2), 195-224. https://doi.org/10.1007/s13520-019-00094-3

Tuanakotta, T. M. (2015). Audit kontemporer. Jakarta: Salemba Empat.

Vinzi, V. E., Chin, W. W., Henseler, J., & Wang, H. (2010). Perspectives on partial least squares Handbook of partial least squares (pp. 1-20): Springer. https://doi.org/10.1007/978-3-540-32827-8_1

Vitell, S. J., Bing, M. N., Davison, H. K., Ammeter, A. P., Garner, B. L., & Novicevic, M. M. (2009). Religiosity and moral identity: The mediating role of self-control. Journal of Business Ethics, 88(4), 601-613. 1 https://doi.org/0.1007/s10551-008-9980-0

Walker, A. G., Smither, J. W., & DeBode, J. (2012). The effects of religiosity on ethical judgments. Journal of Business Ethics, 106(4), 437-452. https://doi.org/10.1007/s10551-011-1009-4

Welch, M. R., Tittle, C. R., & Grasmick, H. G. (2006). Christian religiosity, self-control and social conformity. Social Forces, 84(3), 1605-1623.

https://doi.org/10.1353/sof.2006.0075

Winchester, D. (2008). Embodying the faith: Religious practice and the making of a Muslim moral habitus. Social Forces, 86(4), 1753-1780.

https://doi.org/10.1353/sof.0.0038

Ysseldyk, R., Matheson, K., & Anisman, H. (2010). Religiosity as identity: Toward an understanding of religion from a social identity perspective. Personality and Social Psychology Review, 14(1), 60-71. https://doi.org/10.1177/1088868309349693

Jurnal Ilmiah Akuntansi dan Bisnis, 2021 | 342

Discussion and feedback