The Role of Accountants in Achieving Sustainable Development Goals: Academics Perspective

on

Firmansyah, The Role of ... 242

The Role of Accountants in Achieving Sustainable Development Goals: Academics Perspective

Irman Firmansyah

Faculty of Economics, Siliwangi University, Indonesia email: irmanfirmansyah@unsil.ac.id

DOI: https://doi.org/10.24843/JIAB.2019.v14.i02.p09

ABSTRACT

Jurnal Ilmiah Akuntansi dan Bisnis

(JIAB)

https://ojs.unud.ac.id/index.php/jiab/ user/profile

Volume 14

Nomor 2

Juli 2019

Halaman 242-250

p-ISSN 2302-514X e-ISSN 2303-1018

INFORMASI ARTIKEL

Tanggal masuk: 13 Maret 2019 Tanggal revisi: 27 Juni 2019 Tanggal terima: 1 Juli 2019

This study aims to provide a general description of the role of accountants on sustainable development goals achievement. A qualitative- quantitative research method was used in the analytic network process. The results showed that the role of accountants in achieving the sustainable development goals is divided into three dimensions. The first is the role of the accounting professional organization in providing input to the government about SDGs. The second role of professional accountants is that an accountant must provide SDGs elemental messages in providing recommendations on financial statements. The third role is as an educator; an accountant compiles an education curriculum that adapts to the goals of the SDGs.

Keywords: Accountants, sustainable development goals, academics

Peran Akuntan Terhadap Pencapaian Sustainable Development Goals

ABSTRAK

Penelitian ini bertujuan untuk memberikan gambaran secara umum mengenai peran akuntan terhadap pencapaian sustainable development goals. Metode penelitian menggunakan metode analytic network process. Hasil penelitian menunjukkan bahwa peran akuntan dalam mencapai sustainable development goals yang terbagi ke dalam tiga aspek, yaitu peran organisasi profesi akuntansi yaitu harus memberikan masukan kepada pemerintah tentang SDGs. Sedangkan peran kedua yaitu akuntan profesional adalah bahwa seorang akuntan harus memberikan pesan-pesan unsur SDGs dalam memberikan rekomendasi atas laporan keuangan. Adapun peran ketiga yaitu akuntan pendidik adalah menyusun kurikulum Pendidikan yang menyesuaikan dengan tujuan SDGs. Kata kunci: Akuntan, sustainable development goals, akademisi

INTRODUCTION

The Sustainable Development Goals (SDGs) launched by the United Nations in 2015 have installed 17 environmental sustainability targets to be achieved in 2030. To achieve these targets, the private sector also needs to include SDGs in its corporate strategy. In fact, 8 of the 17 goals to be achieved in the SDGs are directly supported by the work of accountants. Among the several key SDGs that are done by accountants with a variety of diverse roles is the quality of education, gender equality, economic

growth, reducing inequality, security, climate change, justice, and strong institutions.

Accountants in carrying out their professional work are not just compiling financial reports on companies, but more than that accountants have many other jobs, so the goal of sustainable development goals can be realized through the role of accountants. Both accountants and entrepreneurs must focus on SDGs that are most relevant to their industry, sector, and type of business. This includes tools and methods to help businesses manage

reputation risk, respond to globalization, digitization and the impact of policy changes and meet investor demand for greater reporting transparency. This guide suggests that the expertise of management accountants (expertise in governance, management and risk control, business analysis and decision support), organizational roles and ethical commitment places the profession at the forefront of planning and implementing SDGs (Mead, 2018).

Accounting also plays a role in sustainable development through the activities of economic entities, analysis of costs and benefits that have an impact on the environment, the development of innovative practices and environmental pollution policies. This is the role of environmental management accounting (Agustia, 2015). According to Vasile & Man (2012), Environmental management accounting is defined as the process of identification, collection, calculation, analysis, internal reporting and use of information about raw materials and energy, environmental costs and other data regarding costs in the decision-making process to adopt decisions that can contribute to environmental protection.

According to Sudana (2017) that it is important for company accountants to be able to maintain the ecosystem of their business. To be able to portray this function, emancipatory accounting must have three very basic characteristics, namely (1) accounting is intended and has a role to provide information about the ability of business entities to carry out business activities that provide emancipation to ecosystems, intragenerational and intergenerational; (2) accounting must take a role as a catalyst for the creation of emancipatory business practices by continually encouraging spiritual transformation through education for business and accounting practitioners; and (3) accounting must act as a business information system that is able to facilitate the implementation (in full) of economic, social, environmental and spiritual accountability by business entities to preserve the harmony of life guided by the concept of integrated-in-harmony view of sustainable development.

Another role that accountants can take is the possibility of seeing adjustments to the accounting training curriculum to reflect specific goals and initiatives along with the Federation of International Accountants, which in November 2016 nominated eight objectives relevant to the profession. Related to quality education; gender equality; decent work and economic growth; industry, innovation, and

infrastructure; responsible consumption and production; Climate action; peace and justice; strong institution; and partnerships for goals (Economia, 2017).

According to Bakker (2012) that accountants are going to save the world. Accountants will minimize asymmetric information so that reports made by accountants will show the actual conditions because there is an audit process that will check the fairness of the information produced. This will facilitate the management of the company in directing the pace of the company in accordance with the objectives of the SDGs in the actual conditions that occur.

Actually, the role of accountants in the SDGs is still in the literature debate stage (Makarenko & Plastun, 2018). But this does not become a strong basis in terms of practice in the field because accountants actually have many roles that we can know immediately. As stated by Lovell & MacKenzie (2011) that professional accountant organizations play a role in regulating the new carbon economy and climate change. This shows the extent of the role of accounting in business. O’Dwyer & Unerman (2016) show that the public can take advantage of accounting research because it will provide information that accountants are not just informing numbers but can provide other information. The results of the research will be more convincing that accounting is an important part of doing business. Schaltegger, et al (2017) explain the role of innovation in accounting during the promotion of the sustainability of the company. And there are many other roles that show that accountants are not as fresh as providing financial information that is in accordance with the standards, but other information that can be presented in the accountant’s report. The number of accountants’ role in implementing sustainable development goals, according to some literature, states that accountants have a strategic role in the company’s operations.

Regarding the role of accountants in Indonesia, research is needed to identify the role of accountants and assess the most priority roles between existing roles from different perspectives. Moreover, the results of this study will explain the best strategies that can be done so that accountants can maximize their role. In Indonesia to maximize the role of accountants, it is not only to place accountants only from aspects of practitioners in business, but there are other roles, namely accountants in professional organizations and educator accountants.

RESEARCH METHODS

Respondents in this study were carried out by considering the respondents’ understanding of the issues being discussed in particular regarding the role of accountants in implementing the SDGs. The number of respondents in this study consisted of seven people, with the consideration that they were quite competent in representing the entire population. The analysis used in this study is the Analytic Network Process (ANP). In ANP analysis the number of samples/respondents is not used as a benchmark for validity. Valid respondent requirements in ANP are that they are the people who know the problem most closely. In this study respondents were accountants who doubled as academics representing large universities in the province of West Java and had an understanding of the points that were the target of the SDGs.

Analytic Network Process (ANP) is a mathematical theory that is able to analyze the influence of the assumptions approach to solving the form of the problem. This method is used in the form of completion with consideration of adjusting the

complexity of the problem by decomposing the synthesis along with the priority scale which results in the biggest priority influence. ANP is also able to explain the model of dependence factors and their feedback systematically. Decision making in ANP applications is by considering and validating the empirical experience (Saaty & Vargas, 2006).

The question in the questionnaire is in the form of pairwise comparison (comparison of pairs) between elements in the cluster to find out which of the two has greater influence (more dominant) and how much the difference is seen from one side. The numerical scale 1-9 used is a translation of the verbal judgment.

The fundamental scale of values to represent the intensity of the assessment can be seen in table 1. This scale has been derived through stimulusresponse theory and validated for effectiveness, not only in the form of applications by a number but also through the theoretical justification of the scale using a comparison of homogeneous elements (Saaty & Vargas, 2006.).

Table 1. Fundamental Scale

|

Intensity of Definition Explanation Importance Equal Importance Two activities contribute equally to the objective Weak Moderate importance Experience and judgment slightly favor one activity over another Moderate plus Strong importance Experience and judgment strongly favor one activity over another Strong plus Very strong or Demonstrated An activity is favored very strongly over another; its dominance demonstrated in practice Very, very strong Extreme importance The evidence favoring one activity over another is of the highest possible order of affirmation | |

|

Reciprocals of above |

if activity i has one of the above nonzero numbers A reasonable assumption assigned to it when compared with activity j, then j has the reciprocal value when compared with i |

|

Rationals |

Ratios arising from the scale If consistency were to be forced by obtaining n numerical values to span the matrix |

Sou rce: Saaty & Vargas, 2006

At the stage of filling out the questionnaire by the respondent, assistance must be given to maintain consistency of the answers given by the respondent. In general, the questions in the ANP questionnaire

have a very large amount so that inconsistencies may occur in every answer given (Firmansyah & Devi, 2017).

Linear Hierarchy

Goal

Criteria

Subcriteria

element

Component, Cluster (level)

Aloop indicator that each element depends only on itself

Feedback Network

Figure 1. Differences AHP and ANP

Source: Data processed, 2018

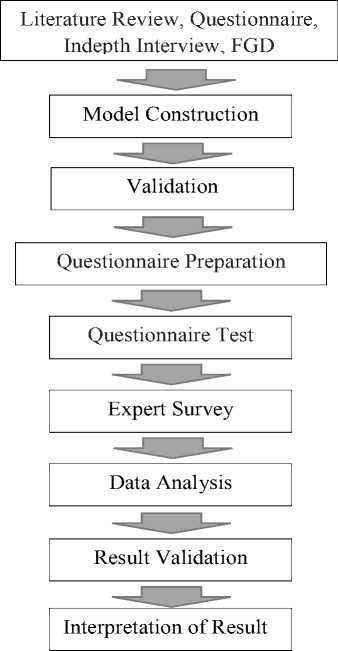

The Analytic Network Process is a refinement of the Analytic Hierarchy Process (AHP). In AHP networks there are levels of objectives, criteria, subcriteria, and alternatives, where each level has an element. Meanwhile, in the ANP network, the level in the AHP is called a cluster that can have criteria and alternatives in it, which is now called a node. Figure 1 shows the difference between AHP and ANP where there is feedback in the ANP network. With feedback, alternatives can depend on criteria such as hierarchies but can also depend on other alternatives. Furthermore, the criteria themselves can depend on alternatives and on fellow criteria. Meanwhile, feedback increases priorities derived from judgment and makes predictions more accurate. Therefore, the results of ANP are expected to be more stable. The following are the stages of research using the ANP method.

From the data obtained, to find out the results of individual assessments of respondents and determine the results of opinions in one group, an assessment was carried out by calculating the geometric mean (Saaty & Vargas, 2006). While rater agreement is a measure that shows the level of conformity (agreement) of respondents (R1-Rn) to a problem in a cluster. The tool used to measure the rater agreement is Kendall’s Coefficient of Concordance (W; 0 <Wd” 1). W = 1 shows perfect compatibility (Ascarya, 2011). To calculate Kendall’s (W), the first is to give a ranking on each answer then add it

Figure 2. Research Stage

Source: Ascarya & Yumanita, 2008

The sum of squares of deviation (S), calculated by the formula:

together.

R1 = Σ" = lrω .................................(1)

The average value of the total ranking is

R = ∣m(n + 1)...........................................(2)

5 = ∑^=l(Λi-Λ)2……………...………(3) So it gets Kendall’s W, namely:

W maGιs-n> ……………….....………(4)

If the W test value is 1 (W = 1), it can be concluded that the assessment or opinion of the respondents has perfect suitability. Whereas when the W value is 0 or getting closer to 0, it indicates a discrepancy between the respondent’s answers or varied answers (Ascarya, 2011).

RESULTS AND DISCUSSIONS

From the results of the research that has been carried out in accordance with the first stage, namely the construction of the model, the data collection is carried out in several ways, namely (1) through the review literature on the results of research and literature review, (2) conducting interviews with academics, and (3) using a questionnaire. The indepth interview and questionnaire were given to seven academics in West Java who represented each region as well as knowing the problems being studied, namely the role of accounting towards sustainable development goals.

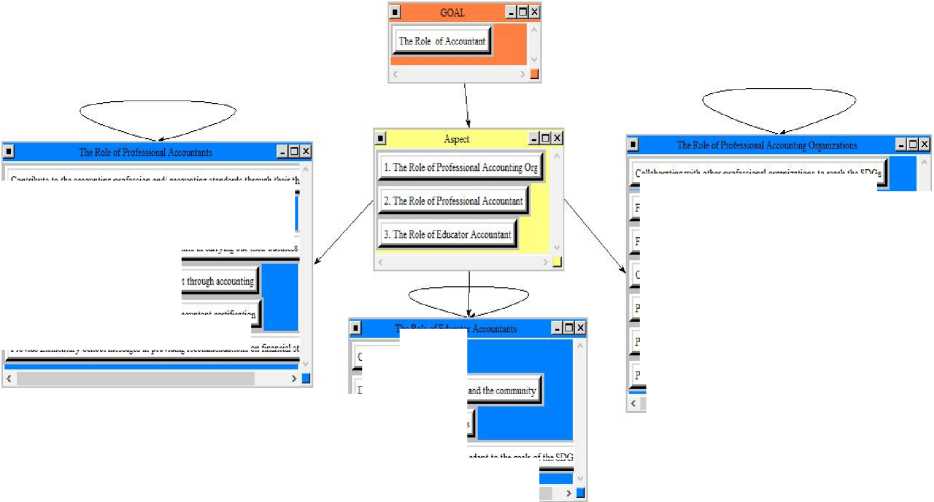

The results of the research in the first stage then obtained the priority role of accountants in three aspects, namely the role of the accounting profession organization, the role of professional accountants and the role of educating accountants. Some of these aspects are the role of professional accounting organizations. These aspect includes organize seminars on the role of accountants in achieving SDGs. Professional accountant organizations must be at the forefront and commitment to the

achievement of the SDGs, provide innovations in the preparation of digital-based financial reports and audits that are in line with global conditions, formulate accounting standards in accordance with the SDGs, fostering members in introducing and implementing SDGs, provide input to the government regarding SDGs. Collaborating with other professional organizations to reach the SDGs.

Second aspect is the role of professional accountants. These aspect includes encouraging companies to fulfill SDGs requirements in carrying out their business, helping SMEs in growth and development through accounting, deliver accounting information objectively or fairly, provide Elementary School messages in providing recommendations on financial statements, increase professionalism through professional accountant certification, contribute to the accounting profession and accounting standards through their thoughts.

Third aspect is the role of educator accountants. These aspect includes the education curriculum must adapt to the goals of the SDGs, improve the quality of lecturers, conduct research on SDGs, and disseminate SDGs to students and the community.

From the aspects and priorities that have been obtained, then an analytic network process (ANP) model is established which is validated by one of the respondents who is considered the most competent. The network model is formed as follows.

Helping SMEs SXEs in growth and devel

j. Ihe Kole of Educator Accountant

Ihe Role OfEducator Accountants

Collabofatiflgwithothefptofessioflal organizations to reach the SDGs

Formulate accounting standards in accordance with the SDGs ∣

Organize seminars on the role of accountants in.

Professional accountant organizations must be at the forefront and commitment t

Provide innovations in the preparation of digital-based financial reports and audil

Conduct research on SDGs

Pmidejqrmc^hegcv^

Dissemiflate SDGs to

Improve the quality Oflecturers

Fostet⅛gιnanbet>ii^^

Figure 3. Network Model

Source: Data processed, 2018.

Contribute to the accounting profession and accounting standards through their th

Deliver accounting information Objectkely fairly |

Encouraging companies to fulfill SDGs requirements in carrying out their business

Increase professionalism through professional accountant certification

Provide Elementaryr School messages in providing recommendations on financial st

The education curriculum must adapt to the goals of the SDG

After the model is obtained, then the second phase is compiling a paired questionnaire and then distributing it to all respondents who have previously been conducted in-depth interviews. So that it enters the third phase, namely the analysis of research results.

Based on the assessment of all respondents regarding the role of accountants towards the achievement of the SDGs, the following results were obtained.

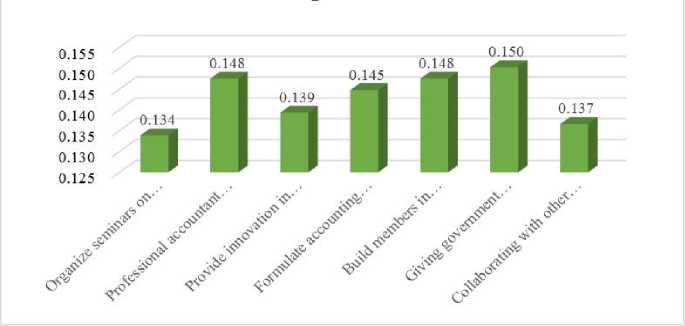

Figure 4. Priority Aspects of the Role of Professional Accounting Organizations

Source: Data Processed, 2018

From the seven priorities that have been collected, there are three most important priorities according to academics in West Java related to the role of accountants in achieving the SDGs. The Kendal coefficient of 0.998 shows that the answers among respondents have a very high agreement with the priority arrangement.

The role of professional organizations which is the most important in achieving SDGs implementation is to provide input to the government regarding SDGs. Professional organizations must be able to maximize their strength in providing input while reducing the importance of cooperation with the government towards global goals. The government has a large influence on the community so that all policies will be carried out by the community.

Therefore, accounting academics view that the government is the best object in achieving the SDGs.

The second priority is that the accounting profession must be at the forefront of bringing all its members to commit to the SDGs. Accountants are certainly waiting for policies and regulations made by the organization so that their actions do not violate the accountant’s code of ethics. So that the professional organization is not the party that rules the government and members but must be the main actor

The third priority is that professional organizations must continue to develop by holding workshops or seminars on the role of accountants in implementing the SDGs. This activity is carried out continuously as a form of the profession’s seriousness in committing towards a global agreement.

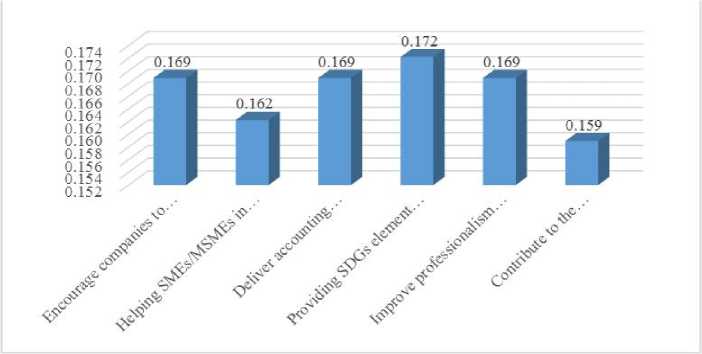

Figure 5. Priority Aspects of the Role of Professional Accountants

Source: Data Processed, 2018

Based on the results of the study, academics have an assessment of the role of professional accountants in companies or accounting services offices with Kendal coefficient of 0.976 which indicates that all respondents have a high agreement.

The most important role of a professional accountant is to strive to convey SDGs element messages on financial statements prepared or financial reports examined. This is because accounting contributes to the achievement of SDGs through financial statements prepared so that on that occasion accountants must work well and be full of professionalism in order to give their role to the world agreement regarding the achievement of the SDGs

The next sequence of roles is that the accountant must provide recommendations on the course of the

company through a report prepared and must be able to encourage management so that in carrying out their business they always pay attention to global interests, especially the achievement needs of the SDGs.

The third order is accountants must objectively convey information. Any information generated from accountants will be used as a tool for corporate decision making, therefore the preparation of financial statements should be done as well as possible without any specific interests.

The fourth sequence is that accountants must have accounting certifications that will show that an accountant is a professional, in addition, accountants must always update the information so that their knowledge continues to increase according to current needs.

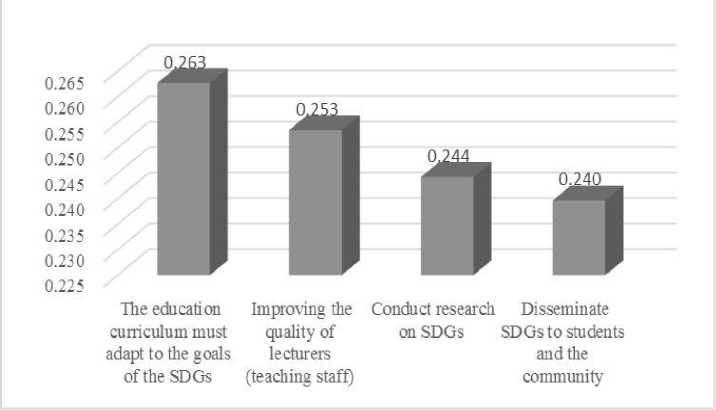

Figure 6. Priority Aspect of the Role of Educator Accountants

Source: Data Processed, 2018

Data that has been collected from research on academic respondents shows that there are 4 important roles of an educating accountant in achieving the SDGs. The Kendal coefficient has a value of 0.799 so that it shows a high agreement among the answers of the respondents.

Education curriculum must adapt to the goals of the SDGs. The first sequence of the role of the educator accountant is, as the main driver in compiling the curriculum for higher education and/or secondary education so that in preparing the curriculum will be adjusted to the demands of the times. The achievement of SDGs as a common need now must be applied to the education process so that students/ students understand the importance of implementing the SDGs and systematically form student thought patterns towards the SDGs.

Higher education institution must be improve the quality of lecturers. The second order is increasing the quality of lecturers (teaching staff). Lecturers as parties who transfer information to students must certainly have good quality. The quality of lecturers, in this case is an understanding of accounting that is not only limited to theory but understands practice in the field. So that students feel there is satisfaction in receiving information from lecturers.

The third sequence is accountant must conduct research on SDGs. Because these SDGs are still the goals that people aspire to in the world, applicative research is still needed to create these goals. Therefore, educator accountants do not only carry out the process of transferring knowledge but must also contribute to efforts to find solutions towards achieving the SDGs through good research.

The fourth sequence is accountant educators must routinely disseminate information about SDGs to both students and the community. Even though educator accountants are more focused on teaching accounting, but because students and society need information about the SDGs related to not getting good information about the SDGs, all educators including educator accountants must be involved in socializing it so that the hope is that students and communities will be involved in implementation efforts SDGs.

CONCLUSIONS

Based on the results of the research and discussion, this study concluded that there is a role for accountants in the achievement of the Sustainable Development Goals which are divided into three aspects, namely the role of the accounting profession organization, the role of professional accountants and the role of educating accountants. The most important role of the aspect of professional organizations is that professional organizations must provide input to the government regarding SDGs, besides that professional organizations of accountants must be at the forefront and commitments towards the achievement of the SDGs. This result is in accordance with Mead (2018) which explains that organizations must be in the front especially in making a plan so that SDGs can be implemented properly. Whereas the role of a professional accountant is that an accountant must provide SDGs elemental messages in providing recommendations on financial statements, in addition, the accountant must encourage the company to fulfill the SDGs requirements in carrying out its business. In accordance with Agustia (2015) that accountants also play a role in the perspective of environmental management, so the company will not disrupt the environment so that the environment will be maintained. The role of the educating accountant is the accountant educator must compile an Education curriculum that adapts to the SDGs goals. Besides that, another important factor is that lecturers must be of good quality who are ready to update accounting information.

This research implies that the accounting profession has an important role in achieving the SDGs. The results of the study explain that the accounting profession must be the spearhead in determining the direction of accounting to reach the SDGs because the rules and codes of ethics are

determined by professional organizations. In addition, this study provides a strong signal that professional accountants must maximize their role in the company so as to provide input to management to run the company’s operations with a focus on achieving the SDGs. Another implication is that educator accountants must be prepared to increase professionalism in transferring knowledge to students regarding the role of accountants in achieving SDGs. Therefore the curriculum must be adjusted to the current needs related to achieving Sustainable Development Goals

This research has limitations so it needs to be developed by increasing the number of respondents who are not only 7 people in academia but can be done to practitioners and regulations so that the results obtained are better.

REFERENCES

Agustia, D. (2015). Peran Profesi Akuntan Manajemen Terhadap Perubahan Lingkungan Global/ : Perspektif Implementasi, (April).

Ascarya; Yumanita, D. (2008). Analisis Efisiensi Perbankan Konvensional dan Perbankan Syariah di Indonesia dengan Data Envelopment Analysis (DEA). Jakarta: Kencana Prenada Media Group.

Ascarya. (2011). The Persistence of Low Profit and Loss Sharing Financing in Islamic Banking: The Case of Indonesia. Review of Indonesian Economic and Business Studies, 1.

Bakker, P. (2012). Accountants Will Save the World. Speech at The Prince’s Accounting for Sustainability Forum on December 13, 2012. Retrieved from http://www.wbcsd.org/Pages/ eNews/e News Details .aspx? ID =15305 & No Search Context Key = true/.

Economia. (2017). How the accountancy profession is shaping global development goals. Retrieved from https://economia.icaew.com/features/ february-2017/how-accountancy-profession-is-shaping-global-development-goals

Firmansyah, I., & Devi, A. (2017). The Implementation Strategies of Good Corporate Governance for Zakat Institutions in Indonesia. International Journal of Zakat, 2(2), 85–97.

Lovell, H & MacKenzie, D. (2011). Accounting for Carbon: The Role of Accounting Professional Organisations in Governing Climate Change. Antipode, 43, 704–730.

Makarenko, I., & Plastun, A. (2018). The role of accounting in sustainable development. Accounting and Financial Control, 1(2), 4– 12. https://doi.org/10.21511/afc.01(2).2017.01

Mead, L. (2018). Guide Highlights Role of Management Accountants in Implementing SDGs. IISD. Retrieved from http://sdg.iisd.org/ news/guide-highlights-role-of-management-accountants-in-implementing-sdgs/

O’Dwyer, B., & Unerman, J. (2016). Fostering rigour in accounting for social sustainability. Accounting, Organizations and Society, 49(June 2015), 32–40. https://doi.org/10.1016/ j.aos.2015.11.003

Saaty, T. L., Vargas, L. G., & Vargas, L. G. (n.d.). Decision Making With The by Spri ineer.

Schaltegger, S.; Etxeberria, I. A.; Ortas, E. (2017). Innovating Corporate Accounting and Reporting for Sustainability – Attributes and Challenges. Sustainable Development, 25, 113–122. Retrieved from https://onlinelibrary.wiley.com/ doi/full/10.1002/sd.1666

Sudana, I. P. (2017). Sustainable Development, Kebijakan Lokal Bali, dan Emancipatory Accounting. Jurnal Akuntansi Multiparadigma, 207–222. https://doi.org/10.18202/jamal.2016. 08.7017

Vasile, E., & Man, M. (2012). Current Dimension of Environmental Management Accounting. Procedia - Social and Behavioral Sciences, 62, 566–570. https://doi.org/10.1016/ j.sbspro.2012.09.094

Discussion and feedback