External Debt Sustainability in Selected ASEAN Countries: Do Macroeconomic Data and Institutions Matter?

on

pISSN : 2301 – 8968

JEKT ♦ 14 [1] : 37-58

eISSN : 2303 – 0186

External Debt Sustainability in Selected ASEAN Countries: Do Macroeconomic Data and Institutions Matter?

Malik Cahyadin

Universitas Sebelas Maret

ABSTRACT

This study attempts to assess indicators of external debt sustainability in seven selected ASEAN countries during 1996-2017 using an indicator-based model. Panel cointegration test was also employed to examine the impact of macroeconomic indicators and institutions on external debt sustainability. There are two indicators of external debt sustainability, namely: (a) EDS1 —in which the growth of the external debt should be lower than the growth of GDP, and (b) EDS2—in which the growth of GDP should be greater than the real interest rate. The findings show that macroeconomic indicators and some institutional indicators impact significantly on EDS1 while the macroeconomic indicators—such as, GDP growth, inflation and FDI inflows—and a single indicator of institutions, i.e., government effectiveness, give a significant impact on EDS2 in the short-run. The speed of adjustment indicates a significant impact on external debt sustainability in the short-run. Furthermore, panel cointegration explains that in the long-run macroeconomic indicators (exclude exchange rate) and institutions have a significant effect on the external debt sustainability. The results of the study aim to contribute to governments policies in the form of an external debt management policy, progrowth, pro-investment, price stability and institutional quality improvement at both country and ASEAN levels.

JEL Classification: E02, E31, E43, E62

Keywords: external debt sustainability, macroeconomic indicator, institutions, panel cointegration

Hutang Luar Negeri yang Berkelanjutan di Negara-negara ASEAN terpilih: Apakah Data Makroekonomi dan Kelembagaan Penting?

ABSTRAK

Studi ini akan mengukur indikator hutang luar negeri yang berkelanjutan di tujuh negara ASEAN selama 1996-2017 menggunakan indicator-based model. Uji kointegrasi panel diterapkan untuk mengestimasi dampak indikator makroekonomi dan kelembagaan terhadap hutang luar negeri yang berkelanjutan. Terdapat dua indikator hutang luar negeri yang berkelanjutan, yaitu: (a) EDS1 – yang menunjukkan tingkat pertumbuhan hutang luar negeri lebih rendah dibandingkan dengan pertumbuhan GDP, dan (b) EDS2 – yang menunjukkan pertumbuahn GDP lebih besar dibandingkan dengan tingkat bunga riil. Temuan-temuan studi menunjukkan bahwa indikator makroekonomi dan beberapa indikator kelembagaan berdampak signifikan terhadap EDS1 sedangkan makroekonomi indikator – seperti pertumbuhan GDP, inflasi dan FDI inflows – dan satu indikator kelembagaan – seperti efektivitas pemerintah – berdampak signifikan terhadap EDS2 dalam jangka pendek. Speed of adjustment berdampak signifikan terhadap hutang luar negeri yang berkelanjutan dalam jangka pendek. Lebih lanjut, kointegrasi panel menjelaskan bahwa dalam jangka panjang indikator makroekonomi (kecuali nilai tukar) dan kelembagaan berdampak signifikan terhadap hutang luar negeri yang berkelanjutan. Hasil studi berkontribusi terhadap kebijakan pemerintah seperti kebijakan pengelolaan hutang luar negeri, pro-pertumbuhan, pro-investasi, stabilitas harga dan peningkatan kualitas kelembagaan baik pada tingkat sebuah negara dan tingkat ASEAN.

Klasifikasi JEL: E02, E31, E43, E62

Kata-kata kunci: hutang luar negeri yang berkelanjutan, indikator makroekonomi, kelembagaan, kointegrasi panel

INTRODUCTION

In the last two decades several countries have faced high level of external debt accumulation. It becomes a debate scholarly about the sustainability of external debt. Some key factors that drive the accumulation are among others: excess liquidity of international finance and optimistic expectation of repayment capacity (Mustapha & Prizzon, 2015) and financial crisis (Curtaşu, 2011; UNCTAD, 2018). Specifically, external debt is a significant source of financing in driving economic development in developing countries through capital accumulation and infrastructure. In contrast, Lukkezen & Rojas-Romagosa (2013) identifies detrimental effects of high debt accumulation on the economy, such as a constraint for economic growth, crowd-out private investment, and increased interest payment. Furthermore, the hefty external debt will create fiscal risks in the short- and long-run to realize government obligations (IMF, 2013). Fiscal risk arises from a growth in external debt that is higher than government revenue and economic growth. Scholarly discussion shows that the concept of government’s budget constraint requires conditions where current spending plus the cost of servicing current debt equals current tax revenues plus the issuance of new debt (Neck & Sturm, 2008).

In general, external debt sustainability can be defined as "the ability of a country to meet the current and future external obligations of both private and public sectors without running into arrears, recourse to debt-rescheduling and eventually a drastic balance-of-payments adjustment" (Akyüz, 2007). The accumulation of current and new debt is expected to decrease over time (Greiner & Fincke, 2015). However, Debrun, Ostry, Willems & Wyplosz (2019) emphasize that external debt sustainability is more relevant based on a forward-looking concept. It means that the measurement of external debt sustainability stresses the future value of the budget balance or solvency to pay the external debt in the long-run. Nevertheless, the operational definition of external debt sustainability is difficult to address (Draksaite, Snieska, Valodkiene & Daunoriene, 2015).

Loser (2004) describes the accumulation of debt burden over time in developing countries can harm economic growth. It means that external debt accumulation will negatively affect economic growth. Moreover, the volatility in international financial markets is not expected to

have direct and significant implications for the accumulation of external debt. Thus, developing countries can realize macroeconomic indicators in a discipline and an appropriate manner to avoid the risk of crisis. The countries can also employ fiscal policy to reduce the level of deficit and encourage foreign direct investment as well as to preserve interest rate and exchange rate stability.

A number of literature report some indicators of external debt sustainability, such as indicator-based model approach (Mahmood, Arby & Sherazi, 2014; and Kaur, Mukherjee & Ekka, 2017), stochastic indicator under Bohn’s approach (Lukkezen & Rojas-Romagosa, 2013), the stability of public indebtedness under Domar’s approach and Hamilton-Flavin’s approach (Bilan, 2010), and IMF-World Bank debt sustainability framework (Bilan, 2010; and Mustapha & Prizzon, 2015). Hence, the indicatorbased model approach can be utilized to assess the level of external debt sustainability. It is a simple and suitable indicator for examining the external debt sustainability in selected ASEAN countries during the study periods.

Some ASEAN countries have faced high level of external debt accumulation, such as Indonesia, Thailand, Vietnam, the Philippines, Cambodia, Lao PDR and Myanmar. Indonesia alone has the highest level of external debt accumulation since 1990s. During 1996-2017, the countries report the growth of external debt under 10%, such as Thailand (3.02%), the Philippines (3.26%), Myanmar (4.04%), Indonesia (5.02%) and Vietnam (7.87%). At the same time, however, Lao PDR and Cambodia exhibit the high growth of external debt about 9.46% and 10.89%, respectively.

ASEAN countries have also shown various levels of macroeconomic indicators, e.g., economic growth. In general, Vietnam, Myanmar and Lao PDR were able to stabilize economic growh during the study periods. In contrast, during economic crisis in 1997/1998 and 2008/2009 some countries suffer relatively heavy economic growth such as Indonesia, Thailand, the Philippines and Cambodia. Berg (1999) identifies some countries—such as, Indonesia, Thailand and the Philipppines—which have a detrimental effect of economic crisis. Likewise, Lau & Kon (2014) argue external debt hits economic growth directly in Asian countries during 1988-2006. During 1996-2017, the average of economic growth from lowest to highest levels occured in Thailand (3.31%),

Indonesia (4.33%), the Philippines (4.95%), Vietnam (6.52%), Lao PDR (7.05%) and Myanmar (9.61%).

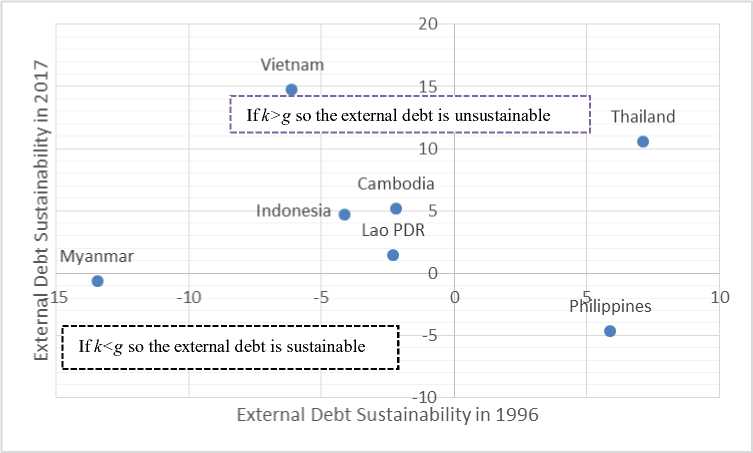

This study is aimed to assess indicators of external debt sustainability in seven selected ASEAN countries during 1996-2017. The indicator-based approach expresses diverse levels of external debt sustainability in 1996 and 2017 (Figure 1). This approach emphasizes that external debt will sustain when the growth of external debt (k) is lower than the growth of GDP (g). For example, in 1996 the growth of external debt and the growth of GDP in Indonesia were 3.70% and 7.82%, respectively. It means that Indonesia reports the level of external debt sustainability is about -4.12% (k<g). Furthermore, in 2017 Indonesia faces risk in

Source: The World Bank and the Author’s calculation

Note: The value of external debt sustainability was estimated using a criterion k-g<0 (growth of the external debt should be lower than the growth of GDP). The criterion was practised by Mahmood, Arby & Sherazi (2014) and Kaur, Mukherjee & Ekka (2017).

Figure 1. External Debt Sustainability in Seven Selected ASEAN Countries

Some previous empirical studies have contributed significantly to economic indicators and institutions with regards to debt sustainability. However, the studies largely ignore to estimate the impact of macroeconomic indicators and institutions on external debt sustainability in ASEAN countries. The empirical study conducted by Fournier & Fall (2017) estimates the sustainability of debt accumulation under a non-linear primary balance, fiscal reaction function and debt limit. The findings show that about 31 OECD countries have a high debt limit. The low level of interest rate has a

external debt unsustainability at the level of 4.69% (k>g). The findings imply that during the study periods Indonesia takes on unsustainable external debt. In contrast, in 1996, the growth of external debt and the growth of GDP in Thailand are 12.77% and 5.65%, respectively. It means that Thailand notes the level of external debt unsustainability is about 7.12% (k>g). Similarly, in 2017 the level of external debt unsustainability in Thailand is about 10.52%. Consequently, during study periods Thailand deals with unsustainable external debt. Indeed, Indonesia and Thailand are ASEAN member countries under high level of external debt accumulation and unsustainable.

significant contribution to promoting debt sustainability.

In addition, OECD countries have a dependency on capital inflows and international markets stability. Another study conducted by Kaur, Mukherjee & Ekka (2017) exhibits fiscal reaction function that applies in India. It has implied on debt sustainability in the long-run. Kersan-Skabic (2017) explains GDP growth, unemployment and interest rates have a significant impact on debt accumulation in the European Union. Moreover, Edo, Osadolor & Dading (2019) argue that external debt and exports have a significant and negative impact on economic growth in Sub-Saharan Africa. In contrast, Paret (2017) describes interest rates, real

exchange rates, and economic growth that did not have any significant impact on debt sustainability in emerging countries.

The previous findings express that ASEAN countries deal with low quality of institutions. Javaid, Iftikhar & Ahmed (2017) report the quality improvement of institutions in the Philippines and Thailand can be promoted by increasing income per capita, tax collection and decreasing military spending while that of in Indonesia can be stimulated by increasing adult literacy, international openness, tax collection and decreasing in indebtedness. The ASEAN countries should also double their efforts to improve quality of institutions to attract foreign direct investment (Masron, 2017). Indeed, the quality of institutions in ASEAN countries need to be improved in order to reduce detrimental effects of external debt accumulation.

This study provides two objectives. First, it aims to assess indicators of external debt sustainability in seven ASEAN countries during 1996-2017 using an indicator-based model. Second, it aims to estimate the impact of macroeconomic indicators and institutions on external debt sustainability. Furthermore, seven countries were utilized as the study samplings, namely: Indonesia, Thailand, the Philippines, Cambodia, Lao PDR, Vietnam and Myanmar. These countries have suitable data on external debt and have high level of external debt accumulation during the study period. The data were collected from the World Bank both the World Bank database and worldwide governance indicator.

The contribution of this study is categorized into three areas: the existing literature, policy and method. It contributes to assess indicators of external debt sustainability in seven ASEAN countries using indicator-based model. In addition, it also examines the impact of macroeconomic indicators and institutions on external debt sustainability. Hence, some macroeconomic indicators will be employed, such as GDP growth, inflation, exchange rate, Foreign Direct Investment (FDI) inflows and real interest rate. The institutions utilize governance indicators published by the World Bank such as political stability and absence of violence, government effectiveness, and control of corruption. The study highlights some policies for governments in ASEAN region, namely: (1) fiscal policy to emphasize the external debt management protocol; (2) macroeconomic policy to stabilize interest rate, inflation and exchange

rate; and, (3) institutional policy under bureaucratic reform and anti-corruption enforcement. In terms of method, some previous studies employ econometrics modeling, such as panel data, GMM, ARDL, Instrumental Variable (IV), VAR. In addition , this study employs panel cointegration test, such as mean group (MG) (Pesaran & Smith, 1995), pooled mean group (PMG) and dynamic fixed effects (DFE) (Pesaran, Shin & Smith, 1999), fully modified ordinary least square (FMOLS) (Pedroni, 1996) and dynamic ordinary least square (DOLS) (Saikkonen, 1992; and Stock & Watson, 1993). These methods will be explored as part of Empirical Techniques section.

The study will be organized into six parts—introduction, literature review, empirical model and econometric model, empirical findings and robustness checkings, conclusion, and reference.

LITERATURE REVIEW

Debt sustainability has been largely discussed in various ways with regards to its definition and measurement. To put it simply, debt sustainability occurs when debt meets solvency conditions. Solvency happens if the future primary surplus is sufficient to pay the principal and interest payment of the debt (IMF, 2002). It also can be estimated under the condition when the current debt plus the present discounted value of total expenditure does not exceed the present discounted value of total revenue. Some operational definitions of debt sustainability are among others: (1) current debt/GDP ratio is lower than or equal to debt threshold, which is known as debt sustainability assessment (Wyplosz, 2007); (2) solvency plus does not need for major correction (IMF, 2002); (3) present value of primary balance is lower than debt/GDP ratio (Arrow, et al, 2004); and, (4) debt/GDP ratio does not grow without bound or debt/GDP ratio is weakly declining (debt stationary condition). According to Wyplosz (2007), external debt is connected to the concept of primary current account balance similar to the public debt that is linked to the concept of primary budget balance.

A comprehensive explanation on external debt sustainability was expressed by Akyüz (2007). External debt sustainability is defined as "the ability of a country to meet the current and future external obligations of both private and

public sectors without running into arrears, recourse to debt-rescheduling and eventually a drastic balance-of-payments adjustment". Akyüz (2007) illustrates that external debt sustainability can be analogous to the concept of fiscal sustainability. Simply stated, external debt sustainability is a condition of a country that is able to meet long-run obligations of both public and private debt that does not have any implication on adjusting balance-of-payment. When private saving and investment (for example foreign direct investment) are higher than external debt, the condition of external debt sustainability will be fulfilled. In addition, external debt should be supported by trade surplus, exchange rate stability, and GDP growth. However, the precise assessment of the level of external debt sustainability in each country is still being debated (Neck & Sturm, 2008). This condition is not only related to the short-run but also the medium- and long-run of a country's ability to repay all obligations to foreign creditors without harming the balance-of-payment stability. Moreover, Greiner & Fincke (2015) explains that the contribution of Hamilton and Flavin (1986) in estimating debt sustainability is significant to indicate the level of debt sustainability of the USA. When the level of current debt is lower than the critical value or target debt, debt sustainability will occur. Conceptually, the debt sustainability can be formulated under the endogenous growth model.

This study utilizes definition of external debt sustainability by Akyüz (2007). Moreover, it will employ some macroeconomic indicators to determine external debt sustainability in selected ASEAN countries, such as GDP growth, inflation, exchange rate, Foreign Direct Investment (FDI), inflows and real interest rate. The explanatory variables also cover institutions under governance indicators published by the World Bank. Panel cointegration test will be employed to examine the impact of macroeconomic indicator and institutions on external debt sustainability.

Debt sustainability can be assessed using several approaches. Wyplosz (2007) identifies several debt sustainability measurements—such as, Debt Sustainability Assessment (DSA), the debt-stabilizing primary balance, value at risk stress test, and policy reaction function. First, DSA was developed by the IMF to assess public and external debt sustainability. The four steps used in the DSA method are: (1) five-year estimates and forecasts of external debt levels

that are influenced by the primary account, GDP growth, interest rates, exchange rates, and inflation (Ferrarini & Ramayandi, 2015; Ncube & Brixiová, 2015; and Mustapha & Prizzon, 2015); (2) debt accumulation identity is bt - bt-1 = (r -g)bt-1 - primary balancet (where b = the debt-to-GDP ratio, r = the real interest rate, and g = the GDP growth) (Corsetti, 2018); (3) stress test on forecast at Point 1; and, (4) stress test at Point 3 shows the level of debt as a sustainability consideration—a stress test that is too high has implications for unsustainable debt.

The second approach is the debtstabilizing primary balance which describes that debt sustainability will be achieved if the primary balance or current account and exchange rate are stable. The third approach is value at risk stress test which expresesses that financial institutions apply the value of the risks to anticipate the risk of the financial portfolio. The stress test is applied to identify the level of risk of default or possible bankruptcy of the financial portfolio. The last approach is the policy reaction function which indicates the reaction of the policymaker to the current debt level and the ability to pay all obligations in the long-run.

As stated by Mahmood, Arby & Sherazi (2014), external debt sustainability is determined by the balance of payment and the cost of borrowing foreign funds. Mathematically, it can be formulated as it*Dt-1 - Ct = Dt - Dt-1, where i* is the nominal interest rate, D is an external debt stock and C is a non-interest current account balance. Besides, external debt dynam*ics can be measured by the equation δd —t___t√ , - c

t dt 1 ct

1+ gt

where r* is the real interest rate of foreign debt while g is GDP growth. It is also called the indicator-based model approach. Explicitly, Mahmood, Arby & Sherazi (2014) and Kaur, Mukherjee & Ekka (2017) express that indicatorbased models have several conditions that reflect external debt sustainability, namely: (1) r <g (the real interest rate should be lower than the GDP growth); (2) k <g (the growth of public or external debt should be lower than the GDP

growth); (3) s (primary balance to GDP ratio) should be greater than 0 (positive) (Debrun, Ostry, Willems & Wyplosz, 2019); and, (4) PCAB (primary current account balance to GDP ratio) should be greater than 0 (positive). Furthermore, Semmler & Tahri (2017) measure the dynamics of external debt sustainability using the model of a finite time horizon. The economic

growth model, such as the endogenous growth model can be used to demonstrate debt sustainability (Greiner & Fincke, 2015). In addition, there are several perspectives in debt sustainability analysis, such as liquidity, solvency, statutory ceiling, and externalities (Khalid, 2016).

This study employs indicator-based model approach to assess external debt sustainability particularly in seven selected ASEAN countries. The approach, which was utilized by Mahmood, Arby & Sherazi (2014) and Kaur, Mukherjee & Ekka (2017), was a simple and suitable method to measure external debt sustainability in ASEAN countries. Moreover, this study estimates the impact of macroeconomic indicators and institutions on external debt sustainability in seven selected ASEAN countries during 1996-2017. Some macroeconomic indicators and institutions are largely utilized by previous studies. However, this study employs five macroeconomic indicators—such as, GDP growth, inflation, FDI inflow, exchange rate, real interest rate—and three indicators of governance—political stability, government effectiveness, and control of corruption—as a proxy of institutions. Besides, the study contributes to the existing literature in the two ways, i.e., to determine macroeconomic indicators and institutions, and to utilize panel cointegration test.

The previous studies examine the level of debt sustainability and the factors that determine it, such as debt dynamic in Pakistan (Chandia, & Javid, 2013), fiscal limit and external debt risk (Bi, Shen & Yang, 2014), debt dynamic in China (Cuestas & Regis, 2017), debt sustainability and non-linear primary balance (Fournier & Fall, 2017), debt sustainability and fiscal reaction functions in India (Kaur, Mukherjee & Ekka, 2017), macroeconomic dynamic and external debt (Semmler & Tahri, 2017), long-run debt and structural primary balance (Beqiraj, Fedeli & Forte, 2018), monetary policy and debt equilibrium (Cavalcanti, et al, 2018), external debt and economic growth (Edo, Osadolor & Dading, 2019). Conceptually, Semmler & Tahri (2017) suggest that debt dynamic analysis to assess external debt sustainability should be done using a non-linear approach and dynamic macroeconomic models. This is intended to obtain credible external debt sustainability estimation results as a source of fiscal policy and debt management.

Chandia & Javid (2013) show that fiscal policy in Pakistan expresses a sustainable condition because there is a positive relationship between the primary surplus/GDP ratio and the debt/GDP ratio. The interest rate can increase and the exchange rate tends to appreciate as an implication of fiscal spending expansion. Similarly, in India the primary balance stability was significantly related to debt sustainability (Kaur, Mukherjee & Ekka, 2017). Another condition will occur when the increased risk of external debt is triggered by exchange rate volatility and the fiscal limit decreases over time (Bi, Shen & Yang, 2014). Macroeconomic instability and an unreliable fiscal policy can also encourage debt accumulation to become unsustainable (Cuestas & Regis, 2017). The higher debt accumulation and the indication of a decrease in the interest rate will be responded significantly by the primary balance to GDP ratio under the debt limit approach (Fournier & Fall, 2017).

Furthermore, expansionary fiscal policy can create better economic condition but the policy will not be responsive to controlling debt accumulation (Cavalcanti, et al, 2018). Specifically, Beqiraj, Fedeli & Forte (2018) found that there was a significant relationship between debt accumulation and primary balance in OECD countries that indicated debt sustainability. In a different case, Edo, Osadolor & Dading (2019) explain that the relationship between external debt and exports to economic growth is insignificant in the short-run but significant and negative in the long-run.

Interestingly, this study estimates the effect of institutions on external debt sustainability. Conceptually, North (1990) defines ―the institutions are the rules of the game in a society or, more formally, are the humanly devised constraints that shape human interaction‖. In addition, Kasper & Streit (1998) state that institutions are ―defined as man-made rules which constrain possibility arbitrary and opportunistic behaviour in human interaction‖. Furthermore, the measurement of institutions can state to the worldwide governance indicator (WGI). It was published by the World Bank. Nonetheless, this study utilizes three indices of institutions, i.e., political stability, government effectiveness, and control of corruption.

The endogenous growth model elaborates the long-run growth rate of economy as an endogenous variable based on the publication of Romer (1990) (Romer, 2012; and Greiner &

Fincke, 2015). Greiner & Fincke (2015) argue that many countries face public debt that affects the economic growth. Indeed, the linkage between public debt and economic growth can be expressed by endogenous growth model. They assume the endogenous growth model can be determined by capital accumulation and public debt. In addition, public debt implies domestic economy directly. Hence, debt accumulation of a country will lead to the growth rate. It considers both public and private debt accumulation. Thus, the study employs the endogenous growth model with external debt. The goal of study contribution is to examine the determinant factor of external debt sustainability.

This study assesses indicators of external debt sustainability using an indicator-based model (Mahmood, Arby & Sherazi, 2014; and Kaur, Mukherjee & Ekka, 2017). The model is aimed to measure the level of external debt sustainability in seven selected ASEAN countries. In such case, the external debt sustainability can be categorized into:

-

1. k<g is the growth of the external debt that should be lower than the growth of GDP. It will be called as External Debt Sustainability Indicator 1 (EDS1).

-

2. g>i is the growth of GDP that should be greater than the real interest rate. It will be called as External Debt Sustainability Indicator 2 (EDS2).

Previous studies have confirmed the signicant impacts of some macroeconomic indicators and institutions on debt sustainability. The impact can vary under different indicators of external debt sustainability. Hence, this study attempts to formulate a number of hypotheses as follows:

-

1. GDP growth has a significant impact on external debt sustainability. The higher GDP growth will lead to a decrease of EDS1 and an increase of EDS2.

-

2 . Inflation has a significant impact on

external debt sustainability. The higher inflation can cause EDS1 to decrease and EDS2 to increase.

-

3. FDI inflow has a significant impact on external debt sustainability. The higher FDI inflows can result in a decrease of EDS1 and an increase of EDS2.

-

4. The exchange rate has a significant impact on external debt sustainability. An exchange rate appreciation will lead to a decrease of EDS1 and an increase of EDS2.

-

5. olitical stability has a significant

impact on external debt sustainability. The higher quality of political stability can cause EDS1 to decrease and EDS2 to increase.

-

6. Government effectiveness has a significant impact on external debt sustainability. The higher quality of government effectiveness will impact on a decrease of EDS1 and an increase of EDS2.

-

7. Control of corruption has a significant impact on external debt sustainability. The higher quality

of control of corruption will lead to a decrease of EDS1 and an increaseof EDS2.

EMPIRICAL MODEL

Dataset

The study utilizes some data such as external debt, macroeconomic data and indicators of institutions (Appendix A). Besides, external debt sustainability will be assessed using data such as external debt growth, GDP growth and real interest rate. The Indicator-Based Model (IBM) is employed to measure external debt sustainability (Mahmood, Arby & Sherazi, 2014; and Kaur, Mukherjee & Ekka, 2017). IBM is a simple and suitable method to determine the level of external debt sustainability in seven ASEAN countries during the study periods.

Macroeconomic data consist of GDP growth, inflation, FDI inflows, exchange rate and real interest rate. The data were used by previous studies, such as GDP growth (Fournier & Fall, 2017; Kersan-Skabic, 2017; and Beqiraj, Fedeli & Forte, 2018; and Edo, Osadolor & Dading, 2019), interest rate (Fournier & Fall, 2017; Kersan-Skabic, 2017; and Beqiraj, Fedeli & Forte, 2018), domestic investment, foreign investment, and inflation (Onafowora & Owoye, 2019), and exchange rate (Paret, 2017).

Moreover, indicators of institutions have been published by the World Bank in the worldwide governance indicators publication. This study applies three indicators of institutions, i.e., political stability, government effectiveness, and control of corruption. Most empirical studies practice some indicators, such as political stability (Onafowora & Owoye, 2019) and government effectiveness (Paret, 2017). Hence, this study considers the control of corruption indicator as a determinant of externaldebt

sustainability in ASEAN. Indeed, corruption is a significant issue in the economies in Asian region (Huang, 2015).

This study focuses on external debt sustainability in seven ASEAN countries— Indonesia, Thailand, the Philippines, Cambodia, Lao PDR, Vietnam and Myanmar. These countries have faced external debt accumulation and reported relevant data regarding study objectives. Furthermore, the study period was conducted during the 1996-2017. The year 1996 was the initial period of the Worldwide Governance Index (WDI) publishing an institutional indicators. Besides, the period also provides complete information regarding external debt and macroeconomic data in selected ASEAN countries. Thus, the selected ASEAN countries was determined by the external debt accumulation and significant issue in the region. Meanwhile, the study selects macroeconomic data dan indicators of institutions that were employed by some previous studies.

Empirical Techniques

Indicator-Based Model (IBM)

External debt sustainability can be assessed by several methods. This study utilizes an IndicatorBased Model (IBM) to determine the level of external debt sustainability in selected ASEAN countries during 1996-2017. IBM has been employed by Mahmood, Arby & Sherazi (2014) and Kaur, Mukherjee & Ekka (2017). Mahmood, Arby & Sherazi (2014) assess external debt sustainability in SAARC countries (Pakistan, India, Sri Lanka and Bangladesh) while Kaur, Mukherjee & Ekka (2017) examine external debt sustainability in India.

Moreover, IBM has several indicators regarding the level of debt sustainability. There are two indicators of external debt sustainability as follows:

-

1. k<g = the growth of the external debt should be lower than the growth of GDP. The negative value (-) indicates external debt sustainability.

The positive value (+) indicates external debt unsustainability.

-

2. g>i = the growth of GDP should be greater than the real interest rate.

The positive value (+) indicates external debt sustainability

The negative value (-) indicates external debt unsustainability

Panel Cointegration Test

Panel cointegration consists of several econometric techniques, such as Mean Group (MG), Pooled Mean Group (PMG), Dynamic Fixed Effect (DFE), Fully Modified Ordinary Least Square (FMOLS) and dynamic ordinary least square (DOLS). The techniques will be applied to examine the impact of macroeconomic indicators and institutions on external debt sustainability in selected ASEAN countries during the study periods. Furthermore, MG, PMG and DFE will produce both short- and long-run estimation. In contrast, FMOLS and DOLS only produce long-run estimation.

Macroeconomic data include GDP growth, inflation, FDI inflows, and exchange rate. Meanwhile, the indicator of institutions consists of political stability, government effectiveness, and control of corruption. Previous studies set some explanatory variables to determine debt sustainability such as the output gap, GDP growth, and real interest rate (Chandia & Javid, 2013; and Beqiraj, Fedeli & Forte, 2018), government spending, consumption, and exchange rates (Chandia & Javid, 2013), government expenditure and revenue (Kaur, Mukherjee & Ekka, 2017). Moreover, some indicators of institutions which can affect debt sustainability include among others political rights and civil liberties index (Onafowora & Owoye, 2019) and government effectiveness (Paret, 2017).

Modeling external debt sustainability in selected ASEAN countries utilizes the equation as follows:

EDS = f(GDP growth, inflation, FDI, ER, QI)

-

(1)

EDS is external debt sustainability indicators consisting of EDS1 and EDS2 while QI is quality of institutions including political stability (PS), government effectiveness (GE), and control of corruption (CC). In addition, FDI and ER will be transformed in the form of logarithms (L). Thus, the function of Equation-1 becomes as follows:

EDS = f(GDP growth, inflation, LFDI, LER, PS, GE, CC)

-

(2)

Equation-2 will be estimated using panel cointegration test. It can be categorized as the macro panel which indicates that the amount of time (t) is greater than the individual (n). Thus, the appropriate estimation method is panel cointegration test.

The MG approach was developed by Pesaran & Smith (1995). This approach emphasizes the heterogeneity of data and the consistency of long-run estimation. Other approaches cover PMG and DFE developed by Pesaran, Shin & Smith (1999). In addition, MG, PMG and DFE are also able to express the estimation results both in the short- and long-run. Technically, the estimation of MG, PMG and FDE is based on the autoregressive distributed

lag (ARDL) model. The study has estimated the Equation-2 using ARDL model. The result shows that the ARDL model is ARDL (1,1,1,1,1,1,1) (Appendix D). Moreover, the lag length of 1 is determined by Schwarz Bayesian Criterion (SBC) and Akaike Information Criterion (AIC) indicators.

Mathematically, Equation-2 can be formulated by ARDL (1,1,1,1,1,1,1) as follows:

EDS, = C+αιEDS,,-ι + MGDP, + β2 GGDP,-, + β3INF, + β4 INF,-, + β5LFDI1 + β6LFDI,-1 + β7 LER, + β,LER,-1

+ β9 PS,+M>‰ + β,,OE,+β12 GE,-, + βlj CC,+βμ CC,-1 + ε, (3)

EDS is external debt sustainability indicators, the “i” equals seven ASEAN countries, the “i” equals 1996-2017, C equals a constant, α equals a parameter of lagged EDS, β1-14 equal parameters of independent variables, while ε is an error term.

Re-parameterized of Equation-3 is as follows:

ΔEDS = C - (1-α ∣^

it 1) EDSt-1

L

θ1 GGDP - θ2 INF - θ3 LFDI -JlLER -JlPS - θ6 GE - θ7 CC 1-α1 it-1 1-α1 it-1 1-α1 it-1 1-α1 it-1 1-α1 it-1 1-α1 it-1 1-α1 it-1 J

+ β1Δ GGDPit + β2ΔINFit + β3ΔLFDIit + β4ΔLERit + β5ΔPSit + β6Δ GEit + β7Δ CCit + εu(6)

Where: ECT

t-1

Γ _ θ1

Y-1 1

^ _ θ2

t-1 1-α1

1

w

t-1

γ = (1-α )

1

The long-run coefficients can be formulated as follows:

EDSit = α0 +α1GGDPu +α2 INFit +α3 LFDIit +α 4 LERit +α5 PSit +α6 GEit +α7 CCit + vit(8)

Where:

α1 =------; α2 =------; α3 =------; α4 =------; α5 =------; α6 =------; α7 =------; α0 =-----

1-α1 1-α1 1-α1 1-α1 1-α1 1-α1 1-α1

Furthermore, the robustness checking utilizes FMOLS and DOLS. FMOLS and DOLS estimate the impact of macroeconomic indicators and institutions on external debt sustainability in the long-run. Conceptually, FMOLS was developed by Pedroni (1996) while DOLS was formulated by Saikkonen (1992) and Stock & Watson (1993). Besides, DOLS is also explained by Kao & Chiang (2000). Simply stated, Equation-2 can be formulated by FMOLS and DOLS as follows:

EDSit = θi + TiGGDPit + ^INFu + T3LFDIu + T4LERit + r5PSu + τ6GEu + T7CCu + utt (9)

θi is individual effects, ɤ equals parameters of independent variables in the long-run, while ս is an error term.

EMPIRICAL FINDINGS AND ROBUSTNESS CHECKINGS

External Debt Sustainability

The Indicator-Based Model (IBM) was utilized to assess external debt sustainability in selected ASEAN countries. It applies two indicators— Indicator 1 of External Debt Sustainability (EDS1) and Indicator 2 of External Debt Sustainability (EDS2). EDS1 was calculated using k<g or the growth of the external debt should be lower than the growth of GDP (Appendix B). The findings explain that all countries face external debt sustainability and unsustainability in a particular time during study period. In the 1998 economic crisis, Cambodia, Vietnam and Myanmar have a level of external debt sustainability. Likewise, Indonesia, Thailand, Philippines and Lao PDR were significantly hitted by the economic crisis and faced external debt unsustainability. The unsustainable indications are caused not only by the accumulation of external debt but also the relatively deep contraction in economic growth.

Since the 2008 financial crisis, several countries—such as, Indonesia, Thailand, Cambodia, Lao PDR and Vietnam—have indicated facing the risk of unsustainable external debt. The high level of external debt accumulation seems unable to be offset by a significant increase in economic growth. In addition, numerical changes in the level of external debt from sustainable to unsustainable and vice versa have occurred at the beginning and at the end of the study period. For example, in 1996 five ASEAN countries—Indonesia, Cambodia, Lao PDR, Vietnam and Myanmar— had a level of external debt sustainability. Other countries which had a level of external debt unsustainability were Thailand and the Philippines. In contrast, in 2017 two ASEAN countries—i.e, the Philippines and Myanmar— have a level of external debt sustainability. In the same period (2017), five ASEAN countries— i.e., Indonesia, Thailand, Cambodia, Lao PDR and Vietnam—had a level of external debt unsustainability.

The second assessment is called Indicator 2 of external debt sustainability (EDS2). It is calculated by g>i or the growth of GDP should be greater than the real interest rate (Appendix C). The greater economic growth that is balanced

with the decline in interest rates over time will lead the sustainability of external debt. Furthermore, this assessment only emphasizes six countries in ASEAN because Cambodia did not provide sufficient and appropriate data of real interest rate during the study period.

In the 1998 economic crisis, EDS2 records that there were four ASEAN countries having a level of external debt unsustainability, namely: Indonesia, the Philippines, Lao PDR, and Myanmar. At the same time, Thailand and Vietnam have a level of external debt sustainability. However, in the 2008 financial crisis, only Lao PDR has suffered significantly the level of unsustainable external debt. Moreover, the five ASEAN countries were indicated having a level of external debt sustainability. At the beginning of study, Myanmar has a level of external debt sustainability while some countries face a level of external debt unsustainability such as Indonesia, Thailand, Philippines, Lao PDR and Vietnam. In contrast, at the end of the study Indonesia faces a risk of external debt unsustainability. On the other hand, some countries have a level of external debt sustainability, such as Thailand, the Philippines, Lao PDR, Vietnam and Myanmar.

Panel Unit Roots Test

Panel unit roots test utilizes several approaches, such as Im, Pesaran and Shin (IPS), Augmented Dickey-Fuller (ADF)-Fisher, and Phillip-Perron (PP)-Fisher. IPS was introduced by Im, Pesaran and Shin (2003). It was the first generation of panel unit roots test that concerns on heterogenity data. Moreover, Pesaran (2007) formulates ADF-Fisher to analyze cross-sectional dependencies of panel data. Besides, PP-Fisher was the second generation of cross-sectional dependencies in panel data (Phillips & Sul, 2003; Moon & Perron, 2004; and Moon, Perron & Phillips, 2005). The result of the panel unit roots test is exhibited in Table 1.

EDS1 has stationary at the level I(0) both trend and no trend at 1% significance level. I(0) is calculated under several tests, namely: IPS, ADF-Fisher and PP-Fisher. In addition, EDS2 also has stationary at the level I(0) at 5% significance level under IPS and ADF-Fisher and about 1% significance level under PP-Fisher. EDS1 and EDS2 are dependent variables in panel

cointegration test. Therefore, both variables indicate cointegration at the level I(0).

GGDP is GDP growth as a macroeconomic indicator. Higher economic growth and lower growth of external debt and real interest rate will lead to external debt sustainability. A stable and rising GDP growth will provide creditor confidence and trust regarding debtor countries’ ability to pay obligations on schedule. The unit root test result indicates GGDP has been stationary at the level I(0) of 1% significance level.

Moreover, inflation (INF) will raise the level of external debt sustainability. It means that the higher the price level, the accumulation of external debt will increase. INF has been stationary at the level I(0) of 1% significance level. The price level of cross-country analysis can be expressed by exchange rate (LER). The appreciation of exchange rate will push the nominal external debt to be low while the depreciation of exchange rate will lead to an increase in nominal external debt. LER was stationary at the level I(0) of 1% significance level.

Developing countries do not only seek to increase external debt accumulation but also to attract foreign investment (LFDI). The higher foreign investment, the lower external debt is expected to accumulate gradually. LFDI has stationary at the first difference I(1) of 1% significance.

Malik Cahyadin

Moreover, the study uses three institutional quality indicators, namely: political stability (PS), government effectiveness (GE), and control of corruption (CC). Some empirical studies argue that institutional quality can lead to debt sustainability and economic growth. The better the quality of institutions, the level of debt will tend to be sustainable. The unit root test result explains that the three indicators were stationary at the first difference I(0) of 1% significance level. It means that the quality of institutions is cointegrated at I(0).

The cointegration test of panel data can be estimated using Pedroni cointegration test. The results describe that the EDS1 has cointegrated with explanatory variables. It can be concluded from the result of Modified Phillips-Perron test, Phillips-Perron, and Augmented Dickey-Fuller about 5% of significance level. It means that macroeconomic indicators and institutions have a cointegration with Indicator 1 of external debt sustainability (EDS1).

Pedroni cointegration test of EDS2 also indicates cointegrated result. The Modified Phillips-Perron test, Phillips-Perron, and Augmented Dickey-Fuller indicate that there is a cointegration between explanatory variables and Indicator 2 of external debt sustainability about 5% of significance level. Indeed, macroeconomic indicators and institutions have a cointegration with EDS2 about 5% of significant level.

Table 1. Panel Unit Roots Results

|

EDS1 |

EDS2 |

GGDP |

INF | |||||

|

No Trend |

Trend |

No Trend |

Trend |

No Trend |

Trend |

No Trend |

Trend | |

|

Level IPS |

-2.77(0.003)*** |

-1.98(0.024)** |

-2.097(0.018)** |

-1.71(0.043)** |

-3.66(0.000)*** |

-4.08(0.000)*** |

-3.22(0.000)*** |

-4.82(0.000)*** |

|

ADF-Fisher |

29.61(0.008)*** |

23.40(0.054)** |

21.37(0.045)** |

21.21(0.047)** |

39.41(0.000)*** |

42.16(0.000)*** |

34.15(0.002)*** |

50.04(0.000)*** |

|

PP-Fisher First Difference |

51.87(0.000)*** |

44.75(0.000)*** |

41.14(0.000)*** |

53.14(0.000)*** |

46.72(0.000)*** |

45.55(0.000)*** |

46.48(0.000)*** |

56.14(0.000)*** |

|

IPS |

- |

- |

- |

- |

- |

- |

- |

- |

|

ADF-Fisher |

- |

- |

- |

- |

- |

- |

- |

- |

|

PP-Fisher |

- |

- |

- |

- |

- |

- |

- |

- |

Source: The World Bank (processed)

Note: The number in ―()‖ is probability values. ***, ** and * denote rejection of the null of non-stationary at the 1%, 5% and 10% levels of significance, respectively. IPS is Im, Pesaran and Shin. The variable-specified lag is 1.

Continued…

|

LER |

LFDI |

PS |

GE |

CC | ||||||

|

No Trend |

Trend |

No Trend |

Trend |

No Trend |

Trend |

No Trend |

Trend |

No Trend |

Trend | |

|

Level IPS |

-11.11 |

-13.50 |

1.80 |

-0.28 |

-0.52 |

0.37 |

0.34 |

2.77 |

0.19 |

2.53 |

|

(0.000)*** |

(0.000)*** |

(0.96) |

(0.387) |

(0.301) |

(0.645) |

(0.635) |

(0.99) |

(0.578) |

(0.994) | |

|

ADF-Fisher |

155.97 |

135.95 |

9.03 |

13.91 |

16.27 |

11.72 |

9.36 |

2.86 |

9.14 |

3.91 |

|

(0.000)*** |

(0.000)*** |

(0.829) |

(0.456) |

(0.297) |

(0.628) |

(0.807) |

(0.999) |

(0.822) |

(0.996) | |

|

PP-Fisher |

312.09 |

315.72 |

21.40 |

28.48 |

89.27 |

99.53 |

72.45 |

65.95 |

65.19 |

74.32 |

|

(0.000)*** |

(0.000)*** |

(0.092)* |

(0.012)** |

(0.000)*** |

(0.000)*** |

(0.000)*** |

(0.000)*** |

(0.000)*** |

(0.000)*** | |

|

First Difference IPS |

- |

- |

-4.82 |

- |

-7.16 |

- |

-4.74 |

- |

-4.82 |

- |

|

ADF-Fisher |

- |

- |

(0.000)*** 49.69 |

- |

(0.000)*** 73.56 |

- |

(0.000)*** 48.08 |

- |

(0.000)*** 49.09 |

- |

|

PP-Fisher |

- |

- |

(0.000)*** 168.76 |

- |

(0.000)*** 955.64 |

- |

(0.000)*** 694.88 |

- |

(0.000)*** 886.27 |

- |

|

(0.000)*** |

(0.000)*** |

(0.000)*** |

(0.000)*** | |||||||

Source: The World Bank (processed)

Note: LER is the logarithm of exchange rate while LFDI is the logarithm of FDI inflows.

Panel Cointegration Estimation and Robustness Check

The study has two main objectives. First, it estimates the impact of macroeconomic indicators and institutions on external debt sustainability in selected ASEAN countries. The Equation-5 and 6 will be examined using panel cointegration test. The number of lag length is Lag 1 under test of Schwarz Bayesian Criterion (SBC) and Akaike Information Criterion (AIC) indicators. The result of ARDL estimation was illustrated in Appendix D.

Second, it estimates the effect of macroeconomic indicators (GGDP, INF, LFDI and LER) and institutions (PS, GE, and CC) on the external debt sustainability in seven ASEAN countries during 1996-2017. Some econometric techniques were addressed, such as MG, PMG, DFE, FMOLS and DOLS (Table 2). The dependent variable is Indicator 1 of external debt sustainability.

Model 1 reveals that GDP growth and Foreign Direct Investment (FDI) inflows have significant impact on external debt sustainability under PMG and DFE in the long-run. The higher level of GDP growth will lead to lower level of

external debt sustainability while the higher level of FDI inflows promotes higher level of external debt sustainability. Similarly, the findings were also carried out by FMOLS, DOLS and Model 2 of PMG and DFE. In contrast, the significant effect of GDP growth of MG estimation was only shown by Model 2. Moreover, the indicators of institutions—such as, such as political stability (Model 2 of PMG), government effectiveness (Model 1 and 2 of MG), and control of corruption (Model 2 of PMG and DFE, and FMOLS)—have also determined external debt sustainability.

Speed of adjustment (ECT(-1)) confirms the significant effect on external debt sustainability in the short- run in all estimation models. It means that macroeconomic indicators and institutions are significant determinants on the level of external debt sustainability in selected ASEAN countries. Besides, some explanatory variables—such as, GDP growth (Model 1 of PMG and DFE), inflation (Model 1 of MG), political stability (Model 1 and 2 of PMG), government effectiveness (Model 2 of MG), and control of corruption (Model 2 of PMG)—were also determining external debt sustainability.

Table 2. Panel Cointegration Estimation Using Dependent Variable of EDS1

|

Variables |

MG |

PMG |

DFE |

FMOLS |

DOLS | |||

|

Model 1 |

Model 2 |

Model 1a |

Model 2 |

Model 1 |

Model 2 | |||

|

Long-run GGDP |

-3.55 |

-4.79 |

-2.18 |

-1.81 |

-2.12 |

-2.09 |

-1.71 |

-2.83 |

|

(0.160) |

(0.096)* |

(0.000)*** |

(0.000)*** |

(0.001)*** |

(0.001)*** |

(0.000)*** |

(0.000)*** | |

|

INF |

-0.923 |

-0.57 |

0.06 |

0.04 |

0.05 |

0.05 |

0.05 |

0.09 |

|

(0.317) |

(0.607) |

(0.592) |

(0.513) |

(0.606) |

(0.575) |

(0.488) |

(0.641) | |

|

LFDI |

-2.23 |

2.34 |

3.29 |

1.96 |

3.37 |

2.68 |

3.46 |

3.71 |

|

(0.597) |

(0.554) |

(0.004)*** |

(0.011)** |

(0.030)** |

(0.032)** |

(0.004)*** |

(0.026)** | |

|

LER |

23.36 |

0.64 |

-0.75 |

-0.52 |

-0.13 |

-0.59 | ||

|

(0.503) |

(0.956) |

(0.537) |

(0.762) |

(0.926) |

(0.751) | |||

|

PS |

-1.53 |

3.00 |

6.74 |

-2.12 |

-0.48 |

-3.26 | ||

|

(0.919) |

(0.348) |

(0.002)*** |

(0.548) |

(0.857) |

(0.437) | |||

|

GE |

-28.07 |

-28.09 |

-1.88 |

7.05 |

10.81 |

7.49 |

1.89 | |

|

(0.011)** |

(0.074)* |

(0.785) |

(0.437) |

(0.158) |

(0.271) |

(0.853) | ||

|

CC |

-23.59 |

-29.18 |

-6.39 |

-9.07 |

-11.75 |

-16.53 |

-11.26 |

-12.93 |

|

(0.389) |

(0.350) |

(0.398) |

(0.003)*** |

(0.187) |

(0.011)** |

(0.077)* |

(0.217) | |

|

Short-run C |

-84.52 |

37.50 |

-42.09 |

-24.40 |

-50.30 |

-41.77 | ||

|

(0.838) |

(0.816) |

(0.000)*** |

(0.000)*** |

(0.046)** |

(0.076)* | |||

|

D(GGDP) |

-1.24 |

3.92 |

0.97 |

0.35 |

0.75 |

0.69 | ||

|

(0.285) |

(0.363) |

(0.039)** |

(0.498) |

(0.096)* |

(0.111) | |||

|

D(INF) |

0.87 |

0.44 |

-0.08 |

-0.09 |

0.02 |

0.01 | ||

|

(0.057)* |

(0.136) |

(0.768) |

(0.694) |

(0.844) |

(0.928) | |||

|

D(LFDI) |

6.06 |

0.56 |

2.74 |

1.14 |

-1.49 |

-1.48 | ||

|

(0.195) |

(0.863) |

(0.395) |

(0.630) |

(0.404) |

(0.387) | |||

|

D(LER) |

55.87 |

40.29 |

13.32 |

-1.46 | ||||

|

(0.262) |

(0.406) |

(0.601) |

(0.556) | |||||

|

D(PS) |

3.44 |

10.89 |

6.03 |

4.02 | ||||

|

Variables |

MG |

PMG |

DFE |

FMOLS |

DOLS | |||

|

Model 1 |

Model 2 |

Model 1a |

Model 2 |

Model 1 |

Model 2 | |||

|

(0.877) |

(0.006)*** |

(0.032)** |

(0.173) | |||||

|

D(GE) |

-3.56 |

19.58 |

-5.75 |

-7.26 |

-5.67 | |||

|

(0.889) |

(0.036)** |

(0.605) |

(0.363) |

(0.434) | ||||

|

D(CC) |

6.28 |

-24.03 |

2.33 |

-6.90 |

4.50 |

6.43 | ||

|

(0.585) |

(0.535) |

(0.798) |

(0.077)* |

(0.530) |

(0.308) | |||

|

ECT(-1) |

-1.85 |

-1.28 |

-0.77 |

-0.75 |

-0.83 |

-0.83 | ||

|

(0.008)*** (0.000)*** |

(0.000)*** |

(0.000)*** |

(0.000)*** |

(0.000)*** | ||||

|

R2 |

0.231 |

0.558 | ||||||

|

Adj. R2 |

0.152 |

0.221 | ||||||

|

Observation |

140 |

140 |

140 |

140 |

140 |

140 |

140 |

126 |

|

Group |

7 |

7 |

7 |

7 |

7 |

7 |

7 |

6 |

Source: Authors’ estimation

Note: The number in ―()‖ is probability values. ***, ** and * denote rejection of the null of non-stationary at the 1%, 5% and 10% levels of significance, respectively. The ARDL models of MG, PMG and DFE are ARDL(1,1,1,1,1,1,1). a INF, LER, PS, GE and CC are jointly significant (integrated) determinants of EDS1 at 10% (Chi2 is 9.78) under PMG Model. The GGDP, INF, LER, PS and GE are jointly significant (integrated) determinants of EDS1 at 5% (F-statistics is 3.13) under FMOLS Model. The lead and lag of DOLS use the max. lag of SIC Criterion.

The findings show that indicators of institutions will determine external debt sustainability in selected ASEAN countries in several ways. First, the higher the quality of government effectiveness, the higher the external debt sustainability in the short-run will be. In contrast, government effectiveness will harm external debt sustainability in the long-run. Second, the higher quality of political stability will promote external debt sustainability both in the short- and long-run. It means that governments in ASEAN region should guarantee the domestic political stability to manage and use external debt accumulation effectively in order to boost domestic economy. Third, control of corruption hits the level of external debt sustainability. The negative effect of control of corruption indicates that governments in ASEAN regions still face risks of corruptive practices. Hence, the governments should strengthen anti-corruption body and expand campaign of anti-corruption practices.

As shown in the findings of some previous studies, macroeconomic data can determine debt accumulation to be both significant and insignificant. For example, insignificant contributions of investment to reduce government debt accumulation occurs in some developing countries, such as Ghana and Pakistan (Ansah & Qureshi, 2013). Government debt in developing countries can sustain when investment grows over time. It means that the growth of investment can stimulate GDP growth properly so that developing countries have the

ability to pay all obligations in the long-run (Icaza, 2018). Nonetheless, Cavalcanti, et al. (2018) describe that inappropriate investment policies in encouraging debt sustainability can promote inflation, production costs in the private sector and a decline in domestic economic performance. More specifically, Bi & Leeper (2013) and Bi (2017) state that countries facing fiscal limits and declining economic growth cannot guarantee whether debt sustainability (stability) will occur. It was also discovered by Paret (2017) that interest rate, exchange rate and GDP growth do not always guarantee the level of debt is sustainable in emerging countries. This study was supported by Edo, Osadolor & Dading (2019) that economic growth and external debt have a significant long-run relationship in SubSaharan African countries. Nevertheless, countries like Caribbeans can be careful of high debt accumulation because it tends to harm economic growth (Onafowora & Owoye, 2019).

Chandia & Javid (2013) found that the expansion of government spending can be followed by an increase in interest rate and exchange rate appreciation. It is relevant to the empirical findings made by Ganelli (2005) that debt accumulation can encourage exchange rate appreciation. Thus, this condition illustrates that debt accumulation needs to be executed carefully to stabilize interest rate and exchange rate. Current account deficits also have significant implications for unsustainable debt in some

developing countries (Mahmood, Arby & Sherazi, 2014).

Moreover, the previous findings note that political changes have significant impacts on fiscal policy, especially primary balance (Icaza, 2018). It indicates that political stability can also determine the level of debt accumulation in a country. Mustapha & Prizzon (2015) report that there are several sources of debt crisis as a result of unsustainable debt. Those are imprudent lending and borrowing policies, political stability and institutional weakness.

Meanwhile, Onafowora & Owoye (2019) found that the quality of institutions (such as, political right and civil liberties) can be a driver of economic growth which indirectly contributes to debt sustainability. Thus, the quality of institutions can be a determinant of debt sustainability in various countries, including

ASEAN countries. Hence, debt management policies can be designed to guarantee debt sustainability in developing countries.

This study also assessed external debt sustainability using Indicator 2 that can be called EDS2. Table 3 explains the estimation result of panel cointegration with dependent variable of EDS2. The findings record that some macroeconomic indicators—such as, GDP growth, inflation and FDI inflows—determine external debt sustainability in the long-run. The significant impacts of GDP growth and inflation were carried out by PMG, DFE, FMOLS and DOLS while the significant effect of FDI inflows was expressed by MG (Model 2), DFE, FMOLS and DOLS. The results indicate that the level of external debt sustainability will be driven by macroeconomic data.

Table 3. Panel Cointegration Estimation Using Dependent Variable of EDS2

|

Variables |

MG |

PMG |

DFE |

FMOLS |

DOLS | |||

|

Model 1 |

Model 2 |

Model 1a |

Model 2 |

Model 1 |

Model 2 | |||

|

Long-run | ||||||||

|

GGDP |

9.01 |

4.61 |

0.48 |

0.98 |

1.53 |

1.53 |

0.92 |

1.11 |

|

(0.235) |

(0.134) |

(0.006)*** |

(0.000)*** |

(0.001)*** |

(0.001)*** |

(0.000)*** |

(0.037)** | |

|

INF |

1.38 |

0.06 |

0.23 |

0.35 |

0.34 |

0.34 |

0.41 |

0.34 |

|

(0.206) |

(0.802) |

(0.004)*** |

(0.000)*** |

(0.000)*** |

(0.000)*** |

(0.000)*** |

(0.004)*** | |

|

LFDI |

-1.34 |

-2.98 |

0.19 |

1.68 |

1.49 |

1.51 |

1.92 | |

|

(0.528) |

(0.024)** |

(0.579) |

(0.101)* |

(0.096)* |

(0.008)*** |

(0.049)** | ||

|

LER |

-2.04 |

-0.10 |

-1.38 |

-1.11 |

-0.99 |

-0.81 | ||

|

(0.797) |

(0.833) |

(0.229) |

(0.221) |

(0.130) |

(0.449) | |||

|

PS |

-18.73 |

3.87 |

2.98 |

-0.06 |

0.32 |

3.36 | ||

|

(0.580) |

(0.000)*** |

(0.000)*** |

(0.981) |

(0.802) |

(0.184) | |||

|

GE |

58.85 |

27.69 |

12.35 |

8.12 |

5.04 |

6.27 |

9.19 |

8.43 |

|

(0.337) |

(0.094)* |

(0.000)*** |

(0.000)*** |

(0.410) |

(0.093)* |

(0.005)*** |

(0.161) | |

|

CC |

-19.78 |

-20.45 |

-12.30 |

-7.10 |

1.91 |

-3.42 |

-6.143 | |

|

(0.269) |

(0.051)* |

(0.000)*** |

(0.000)*** |

(0.765) |

(0.257) |

(0.358) | ||

|

Short-run | ||||||||

|

C |

45.49 |

136.38 |

-2.55 |

-3.74 |

-14.87 |

-14.11 | ||

|

(0.379) |

(0.205) |

(0.035)** |

(0.000)*** |

(0.106)* |

(0.116) | |||

|

D(GGDP) |

1.28 |

-7.16 |

1.72 |

0.51 |

0.39 |

0.40 | ||

|

(0.376) |

(0.304) |

(0.013)** |

(0.003)*** |

(0.033)** |

(0.031)** | |||

|

D(INF) |

0.16 |

0.56 |

0.55 |

0.39 |

0.31 |

0.31 | ||

|

(0.579) |

(0.025)** |

(0.000)*** |

(0.000)*** |

(0.000)*** |

(0.000)*** | |||

|

D(LFDI) |

2.57 |

0.61 |

0.92 |

0.61 |

0.49 | |||

|

(0.010)*** |

(0.518) |

(0.057)* |

(0.312) |

(0.407) | ||||

|

D(LER) |

-0.80 |

7.76 |

0.52 |

0.24 | ||||

|

(0.793) |

(0.119) |

(0.525) |

(0.765) | |||||

|

D(PS) |

2.32 |

1.04 |

0.32 |

0.62 | ||||

|

(0.472) |

(0.604) |

(0.787) |

(0.541) | |||||

|

D(GE) |

-5.54 |

-59.25 |

2.34 |

-0.36 |

4.80 |

1.95 | ||

|

(0.553) |

(0.296) |

(0.626) |

(0.858) |

(0.085)* |

(0.132) | |||

|

D(CC) |

-1.75 |

42.83 |

1.97 |

1.24 |

-3.43 | |||

|

(0.834) |

(0.267) |

(0.118) |

(0.228) |

(0.164) | ||||

|

ECT(-1) |

-0.94 |

-1.94 |

-0.45 |

-0.69 |

-0.44 |

-0.44 | ||

|

(0.000)*** |

(0.057)* |

(0.007)*** |

(0.000)*** |

(0.000)*** |

(0.000)*** | |||

|

Variables |

MG |

PMG |

DFE |

FMOLS |

DOLS |

|

Model 1 Model 2 |

Model 1a Model 2 |

Model 1 Model 2 | |||

|

R2 |

0.777 |

0.875 | |||

|

Adj. R2 |

0.754 |

0.776 | |||

|

Observation |

119 119 |

119 126 |

119 119 |

126 |

120 |

|

Group |

6 6 |

6 6 |

6 6 |

6 |

6 |

Source: Research output

Note: The number in ―()‖ is probability values. ***, ** and * denote rejection of the null of non-stationary at the 1%, 5% and 10% levels of significance, respectively. The ARDL models of MG, PMG and DFE are ARDL(1,1,1,1,1,1,1). a GGDP, LFDI and LER are jointly significant determinants of EDS2 at 5% (chi2 = 10.75). The GGDP, LER, PS and CC are jointly significant (integrated) determinants of EDS2 at 1% (F-statistics is 9.16) under FMOLS Model. The lead and lag of DOLS use the max lag of SIC Criterion.

In addition, indicators of institutions also should be lower than the growth of GDP), which impact significantly on external debt can be called EDS1. Meanwhile, the second sustainability. For example, political stability has indicator is g>i (the growth of GDP should be determined external debt sustainability under greater than the real interest rate), which is known PMG (Model 1 and 2), government effectiveness as EDS2. Furthermore, seven ASEAN countries— has a significant impact under MG (Model 1), Indonesia, Thailand, Vietnam, the Philippines, PMG (Model 1 and 2), DFE (Model 2) and Cambodia, Lao PDR and Myanmar—were FMOLS, while control of corruption influences selected as samplings because during 1996-2017 external debt sustainability significantly under MG those countries had faced high level of external (Model 2), and PMG (Model 1 and 2). Thus, the debt accumulation. This study proposes two quality of institutions will give both a positive and objectives, namely: (a) to assess external debt a negative impacts to the level of external debt sustainability using an indicator-based model, and sustainability. Moreover, all findings can be set as (b) to examine the effect of macroeconomic robustness checking of panel cointegration test. indicators and institutions on the external debt

In the short-run, speed of adjustment sustainability using panel cointegration test.

(ECT(-1)) records significant impacts on external The findings show that the selected

debt sustainability. It indicates that the panel ASEAN countries—Indonesia, Thailand, Vietnam, cointegration test can report the significant effects the Philippines, Cambodia, Lao PDR and of macroeconomic indicators and institutions on Myanmar—have managed to deal with the external debt sustainability in selected ASEAN external debt sustainability and unsustainability in countries. Furthermore, some macroeconomic a particular time during 1996-2017. It confirmed indicators which have significant contribution the proposed hypothesis that GDP growth has a include among others, GDP growth, inflation and significant impact on external debt sustainability. FDI inflows. It means the variables will determine The higher GDP growth will lead to a decrease of the level of external debt sustainability in the EDS1 and an increase of EDS2. The sustainability shortrun. Yet, there is only one indicator of will occur when the GDP growth is higher than the institution which significantly affects external debt growth of external debt and the GDP growth is sustainability, namely: government effectiveness also higher than the real interest rate. For example, (see Model 1 of DFE). The high quality of in 1996 the EDS1 records that five ASEAN government effectiveness will lead to the high countries—Indonesia, Cambodia, Lao PDR, level of external debt sustainability. Hence, the Vietnam and Myanmar—faced external debt governments in ASEAN region should concern on sustainability. Nevertheless, at the same time the improving bureaucratic reform and applying good EDS2 notes that Myanmar is one of ASEAN governance through improved government countries which has external debt sustainability.

services. Panel cointegration test results in two

findings. First, in the long-run two macroeconomic

CONCLUSION indicators—such as, GDP growth and inflation—

significantly determine Indicator 1 of external debt External debt sustainability can be assessed under sustainability (EDS1) while all indicators of different types of indicators. This study employs institutions—i.e., political stability, government two indicators to assess external debt sustainability effectiveness and control of corruption—were also using an indicator-based model (IBM). The first significant. Meanwhile, EDS2 was impacted by indicator is k<g (the growth of the external debtthree macroeconomic indicators—i.e., GDP

growth, inflation and FDI inflows—and all Bi, H. & Leeper, E. M. (2013), Analyzing Fiscal

indicators of institutions. Second, in the short-run Sustainability, Bank of Canada Working

the speed of adjustment has significant Paper No. 2013-27, pp. 1-38.

contribution to external debt sustainability, as Bi, H., Shen, W. & Yang, S. S. (2014), Fiscal

indicated by panel cointegration test which expresses robustness result. In addition, two macroeconomic indicators—GDP growth and inflation—and three indicators of institutions—

Limits, External Debt, and Fiscal Policy in Developing Countries, IMF Working Papers No. 14/49, pp. 1-18. International Monetary Fund.

high quality of government effectiveness, political Bi, H. (2017), Fical Sustainability: A Cross-

stability and control of corruption—have significantly contributed to Indicator 1 of external debt sustainability (EDS1) while Indicator 2 of

Country Analysis, Kansas City Fed Economic Review, pp. 5-35. DOI: 10.18651/ER/4q17Bi.

external debt sustainability (EDS2) has been Bilan, I. (2010), Model of Public Debt

Sustainability Assessment and Their Utility, Anale: Seria Stiinte Economice, 16, pp. 685-693.

Cavalcanti, M.A.F.H., et al (2018), The

significantly affected by three macroeconomic indicators—GDP growth, inflation and FDI inflows—and by a single indicator of institutions, i.e., government effectiveness.

This study implies on policy recommendations with regards to macroeconomic policies and institutions. In this case, macroeconomic policies can be directed to manage external debt accumulation under external debt protocol, pro-growth policy, pro-investment, and

macroeconomic effects of monetary policy shocks under fiscal rules constrained by public debt sustainability, Economic Modelling, pp. 1-18.

price stability. Meanwhile, the quality institutions should be improved and focused on the quality of bureaucratic reform and government services, domestic political stability, and strengthened anti-corruption body.

REFERENCES

Akyüz, Y. (2007), Debt Sustainability in Emerging Markets: A Critical Appraisal, DESA Working Paper, No. 61, pp. 1-24.

Ansah, J. P. & Qureshi, M. A. (2013), System dynamics model of debt accumulation in developing countries, African Journal of Economic and Management Studies, Vol. 4, Issue 3, pp. 317-337.

http://dx.doi.org/10.1108/AJEMS-08-2011-0060

Arrow, K., et al (2004), Are We Consuming Too Much?, Journal of Economic Perspectives, 18(3): 147-172.

Beqiraj, E., Fedeli, S. & Forte, F. (2018), Public Debt Sustainability: An Empirical Study on OECD Countries, Journal of Macroeconomics, pp. 1-20.

Doi:https://doi.org/10.1016/j.jmacro.2018. 10.002

Berg, A. (1999), The Asia Crisis: Causes, Policy Responses, and Outcomes, IMF Working Paper, WP/99/138, pp. 1-62.

of Chandia, K. E. & Javid, A. Y. (2013), An Analysis of Debt Sustainability in the Economy of Pakistan, Procedia Economics and Finance, 5, pp. 133-142.

Doi:10.1016/S2212-5671(13)00019-1

Corsetti, G. (2018), Debt Sustainability Assessments: the state of the art, European Union.

Cuestas, J. C. & Regis, P. J. (2017), On the dynamics of sovereign debt in China: Sustainability and structural change, Economic Modelling, pp. 1-4. http://dx.doi.org/10.1016/j.econmod.2017. 08.003

Curtaşu, A. R. (2011), How to assess public debt sustainability: Empirical evidence for the advanced European countries, Romanian Journal of Fiscal Policy, 2 (2), pp. 20-43.

Debrun, X., Ostry, J. D., Willems, T. & Wyplosz, C. (2019), Public Debt Sustainability, Discussion Paper DP14010, Centre for Economic Policy Research.

Draksaite, A., Snieska, V., Valodkiene, G. & Daunoriene, A. (2015), Selection of government debt evaluation methods based on the concept of sustainability of the debt, Procedia - Social and Behavioral Sciences, 213, pp. 474-480. Doi: 10.1016/j.sbspro.2015.11.436

Edo, S., Osadolor, N. E. & Dading, I. F., (2019), Growing External Debt and Declining Export: The Concurrent Impediments in

Economic Growth of Sub-Saharan African Kao, C., & Chiang, M.H. (2000), On the

Countries, International Economics, https://doi.org/10.1016/j.inteco.2019.11.01 3

Ferrarini, B. & Ramayandi, A. (2015), Public Debt Kasper, W. & Streit, M. E. (1998), Institutional

Sustainability in Developing Asia: An Update, ADB Economics Working Paper Series, No. 468, pp. 1-50.

http://hdl.handle.net/11540/5302

Fournier, J.-M. & Fall, F. (2017), Limits to government debt sustainability in OECD countries, Economic Modelling, pp. 1-12.

http://dx.doi.org/10.1016/j.econmod.2017. Kersan-Skabic, I. (2017), Is There a Debt-

05.013

Ganelli, G. (2005), The new open economy macroeconomics of government debt, Journal of International Economics, 65, 167-184.

Doi:10.1016/j.jinteco.2004.03.001

Greiner, A. & Fincke, B. (2015), Public Debt, Sustainability and Economic Growth: Theory and Empirics, Switzerland: Springer International Publishing.

Huang, C.-J. (2015), Is corruption bad for economic growth? Evidence from Asia-Pacific countries. North American Journal of Economics and Finance, 1-10.

http://dx.doi.org/10.1016/j.najef.2015.10.0 13

Icaza, V. E. (2018), Fiscal fatigue and debt sustainability: Empirical evidence from the Eurozone 1980-2013, Cuadernos de Economía, 41, 69-78.

http://dx.doi.org/10.1016/j.cesjef.2017.03. 002

Im, K. S., Pesaran, M. H. & Shin. Y. (2003), Testingfor unit roots in heterogeneous panels, Journal of Econometrics, 115, pp. 53-74.

IMF (2002), Assessing Sustainability, Policy Development and Review Department, SM/02/166.

http://www.imf.org/external/np/pdr/sus/20 02/eng/052802.htm.

(2013), Staff Guidance Note for Public Debt Sustainability Analysis in Market-Access Countries, IMF Policy Paper.

https://www.imf.org/external/np/pp/eng/20 Moon, H.R., Perron, B. & Phillips, P.C.B. (2005),

13/050913.pdf.

Javaid, M.N., Iftikhar, N.M. & Ahmed, G. (2017), What Drives the Quality of Institutions in ASIAN Economies? Directions for

Economic Reforms, Journal of South Asia Mustapha, S. & Prizzon, A. (2015), Debt

Studies, 05(03), pp. 127-139.

estimation and inference of a cointegrated regression in panel data. Advances in Econometrics 15, pp. 179–222.

Economics: Social Order and Public Policy, UK: Edward Elgar.

Kaur, B., Mukherjee, A. & Ekka, A. P. (2017), Debt Sustainability of States in India: An Assessment, MPRA Paper, No. 81929, pp. 1-29. https://mpra.ub.uni-muenchen.de/81929

Overhang Problem in the European Union? Economic Imbalances and Institutional Changes to the Euro and the European Union, pp. 277-303. https://doi.org/10.1108/S1569-376720170000018014

Khalid, A. (2016), Perspectives on Public Debt Sustainability, SBP Staff Notes, 04/16, pp. 1-11.

Lau, E. & Kon, T.-L. (2014), External Debt, Export and Growth in Asian Countries: 1988-2006, Journal of Applied Sciences, Volume 14, pp. 2170-2176.

DOI: 10.3923/jas.2014.2170.2176

Loser, C. M. (2004), External Debt Sustainability: Guidelines for Low- and Middle-income Countries, G-24 Discussion Paper Series, pp. 1-17. UNCTAD

Lukkezen, J. & Rojas-Romagosa, H. (2013), Stochastic debt sustainability indicators, Revue de l’OFCE, 127(1), 97-121. doi:10.3917/reof.127.0097

Mahmood, T., Arby, M. F. & Sherazi, H. (2014), Debt Sustainability: A Comparative Analysis of SAARC Countries, Pakistan Economic and Social Review, Volume 52, No. 1, pp. 15-34.

Masron, T.A. (2017), Relative Institutional Quality and FDI Inflows in ASEAN, Journal of Economic Studies, 44(1), pp. 115-137. DOI: 10.1108/JES-04-2015-0067

Moon, H.R. & Perron, B. (2004), Asymptotic Local Power of Pooled t-Ratio Tests for Unit Roots in Panels with Fixed Effects, mimeo.

Incidental Trends and the Power of Panel Unit Root Tests, IEPR Working Papers, Institute of Economic Policy Research (IEPR).

Sustainability and Debt Management in Developing Countries, EPS-PEAKS Topic

Guide, pp. 1-33. Overseas Development Institute

Ncube, M. & Brixiová, Z. (2015), Public Debt Sustainability in Africa: Building Resilience and Challenges Ahead, Working Paper No. 227, pp. 1-27. African Development Bank Group

Neck, R. & Sturm, J.-E. (2008), Sustainability of Public Debt: Introduction and Overview, Cambridge: Massachusetts Institute of Technology.

North, D.C. (1990), Institutions, Institutional Change and Economic Performance, Cambridge and New York: Cambridge University Press.

Onafowora, O. & Owoye, O. (2019), Public debt, foreign direct investment and economic growth dynamics: Empirical evidence from the Caribbean, International Journal of Emerging Markets, pp. 1-23.

https://doi.org/10.1108/IJOEM-01-2018-0050

Paret, A.-C. (2017), Debt sustainability in emerging market countries: Some policy guidelines from a fan-chart approach, Economic Modelling, 63, pp. 26-45. http://dx.doi.org/10.1016/j.econmod.2017. 01.010

Pedroni, P. (1996), Fully Modified OLS for Heterogeneous Cointegrated Panels and the Case of Purchasing Power Parity, Indiana University Working Papers in Economics, No. 96-020, June.

Pesaran, M.H. (2007), A Simple Panel Unit Root Test in the Presence of Cross Section Dependence, Journal of Applied Econometrics, 22, pp. 265-312.

Pesaran, M.H. & Smith, R. (1995), Estimating long-run relationships from dynamic heterogeneous panels, Journal of Econometrics, 68 (1), pp. 79-113.

Pesaran, M.H., Shin, Y., & Smith, R.P. (1999), Pooled mean group estimation of dynamic heterogeneous panels, J. Am. Stat. Assoc., 94 (446), pp. 621-634.

Phillips, P.C.B. & Sul, D. (2003), Dynamic Panel Estimation and Homogeneity Testing Under Cross Section Dependence, Econometrics Journal, 6, pp. 217-259.

Romer, D. (2012), Advanced Macroeconomics, Fourth Edition, New York: McGraw-Hill.

Saikkonen, P. (1992), Estimation and Testing of Cointegrated System by an Autoregressive Approximation, Econometric Theory, 8(1), pp. 1-27.

Semmler, W. & Tahri, I. (2017), Current account imbalances: A new approach to assess external debt sustainability, Economic Modelling, pp. 1-10.